West Virginia Patent of the Year – 2024/2025

EmeryAllen LLC has been awarded the 2024/2025 Patent of the Year for their innovative lighting solution. Their invention, detailed in U.S. Patent No. 11927311, titled ‘Miniature integrated omnidirectional LED bulb’, introduces a compact, energy-efficient lighting option designed to replace traditional incandescent and halogen bulbs.

The patented LED bulb features a semi-cylindrical light pipe populated with LEDs on its external surface, encased within a transparent diffuser. This design ensures uniform light distribution, making it ideal for applications requiring consistent illumination. The integration of a cylindrical heatsink within the bulb’s body facilitates effective thermal management, enhancing the longevity and performance of the LEDs.

EmeryAllen’s innovation stands out with its impressive luminous efficiency of at least 45 lumens per watt and a color rendering index of 90 or higher, ensuring vibrant and accurate color representation. The bulb’s dimmable capability down to 10% of full light output offers flexibility in various lighting environments. Additionally, with a rated lifetime of over 15,000 hours, this LED bulb promises durability and cost-effectiveness over time.

Designed for retrofit applications, this miniature LED bulb aligns with industry standards, offering a sustainable alternative to conventional lighting solutions. EmeryAllen’s commitment to innovation continues to drive advancements in energy-efficient lighting technologies.

Study Case

Fresh Water Inc. is an established water industry supplier focusing on water and energy conservation. In 2009, Fresh Water began developing their main control product, the WaterWally, which was envisioned to be a smart solution to effective, remote water management.

The project has been ongoing for several years. For fiscal year 2015, their main objective for the project is to design and develop improvements to the intuitive, multi-functional, water management system. Specific technical objectives of this project include:

- To design and develop a disinfection management system that destroys pathogens in the water flow;

- To design and develop a system that can manage multiple water sources for non-potable applications;

- To design and develop a larger version of WaterWally incorporating more pumps and catering to different OHS requirements;

- To improve efficiency of embedded software code (i.e. memory use).

Fresh Water needed to determine the eligibility of its proposed R&D activities in order to know if they qualified for the Research and Experimentation Tax Credit. To be eligible, Fresh Water had to be certain that its “qualified research” met four main criteria, known and developed by Congress as the Four-Part Test. Fresh Water conducted the following R&D activities.

Background research to evaluate current knowledge gaps and determine feasibility (background research of the WaterWally).

The background research of WaterWally included literature search and review to find out how WaterWally would function in third-world and developing countries. The study identified a number of functions that would provide significant additional benefit to those users in the area of water quality and safety. Fresh Water’s research into global water issues and climate change confirmed an urgent need for improved rainwater harvesting and re-use around the world. To address this need, WaterWally had to be capable of managing a broader spectrum of water sources and be able to take autonomous action based on a variety of conditions. Parameters to be developed included:

- pH, turbidity and conductivity;

- analysis of previous design solutions and assessment of key interferences to determine potential solutions;

- consultation with industry professionals and potential customers to determine the feasibility of the solution;

- consultation with key component suppliers to determine the factors they consider important in the design, and to gain an understanding of how the design needed to be structured accordingly.

Design and development of a series of prototypes to achieve the technical objectives (design, development and testing of WaterWally).

Fresh Water’s hypothesis for this R&D activity was that theorized designs and redesigns of WaterWally can be implemented physically into a specific physical space and tested for functionality. The R&D activities to test this hypothesis included:

- Physical implementation of new functions to ensure physical fit with existing computer firmware and other components;

- Re-coded embedded software to improve efficiency within space limitations;

- Continued long-term maintenance and reliability testing in existing test sites.

Trials and analysis of data to achieve results that can be reproduced to a satisfactory standard and to test the hypothesis (design of a lager-scale WaterWally).

The hypothesis for this stage stated that Fresh Water could design the components and layout of a larger-scale WaterWally for larger projects, incorporating design changes due to different requirements. The R&D activities in this phase included:

- Sketches with the goal of reducing manufacturing cost (important due for end users) and shortening the overall length of WaterWally;

- 2D technical drawings for:

- Process assessment

- Cross section analysis

- 3D CAD modeling. Key factors examined were:

- The physical relationships between the various components and the control electronics.

- The size and positioning of optional modules control electronics

Ongoing analysis of customer or user feedback to improve the prototype design (feedback of the WaterWally).

Feedback of the WaterWally was necessary to evaluate the performance capabilities of the new design in the field and improve any flaws in the design. Feedback included analysis of feedback from testing results which may serve as starting points for the development of new hypotheses, and application of minor changes such as tweaks or minor modifications to further enable the testing of the new solution.

Qualified research consists of research for the intent of developing new or improved business components. A business component is defined as any product, process, technique, invention, formula, or computer software that the taxpayer intends to hold for sale, lease, license, or actual use in the taxpayer’s trade or business.

The Four-Part Test

Activities that are eligible for the R&D Credit are described in the “Four-Part Test” which must be met for the activity to qualify as R&D.

- Permitted Purpose: The purpose of the activity or project must be to create new (or improve existing) functionality, performance, reliability, or quality of a business component.

- Elimination of Uncertainty: The taxpayer must intend to discover information that would eliminate uncertainty concerning the development or improvement of the business component. Uncertainty exists if the information available to the taxpayer does not establish the capability of development or improvement, method of development or improvement, or the appropriateness of the business component’s design.

- Process of Experimentation: The taxpayer must undergo a systematic process designed to evaluate one or more alternatives to achieve a result where the capability or the method of achieving that result, or the appropriate design of that result, is uncertain at the beginning of the taxpayer’s research activities.

- Technological in Nature: The process of experimentation used to discover information must fundamentally rely on principles of hard science such as physical or biological sciences, chemistry, engineering or computer science.

What records and specific documentation did Fresh Water keep?

Similar to any tax credit or deduction, Fresh Water had to save business records that outlined what it did in its R&D activities, including experimental activities and documents to prove that the work took place in a systematic manner. Fresh Water saved the following documentation:

- Literature review

- Meeting notes

- Sketches/drawings

- Photos

- Screen shots

- Test protocols

- Test results and analysis

- Customer feedback

- Field-test results

- Patent application number

By having these records on file, Fresh Water confirmed that it was “compliance ready” — meaning if it was audited by the IRS, it could present documentation to show the progression of its R&D work.

Choose your state

Never miss a deadline again

Stay up to date on IRS processes

Discover R&D in your industry

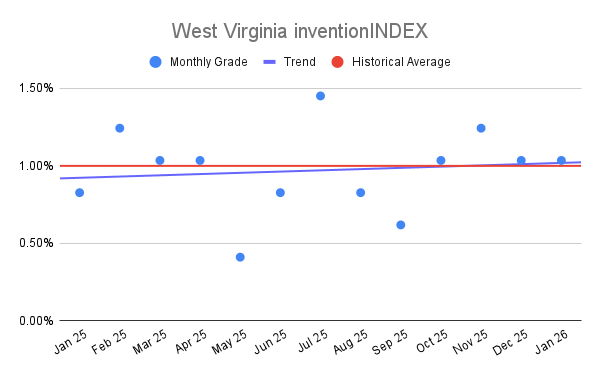

West Virginia inventionINDEX Janua

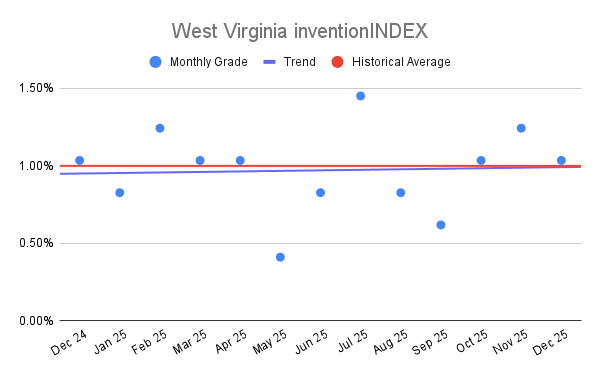

West Virginia inventionINDEX Janua  West Virginia inventionINDEX Decemb

West Virginia inventionINDEX Decemb