Wyoming Patent of the Year – 2024/2025

Row64 INC. has been awarded the 2024/2025 Patent of the Year for revolutionizing compiler parsing. Their invention, detailed in U.S. Patent No. 12050892, titled ‘Card solver compiler parsing’, introduces a novel method to process programming code more efficiently and with greater speed.

ROW64’s patented technique departs from traditional recursive parsing methods by employing a non-recursive, card game-inspired approach. This innovation allows for the sequential evaluation of code tokens, assigning precedence values to determine their processing order. The result is a streamlined parsing process that reduces computational complexity and enhances performance.

Furthermore, the system intelligently allocates processing tasks across different hardware architectures. By directing specific nodes of the parsing process to either CPU or GPU resources based on their parallelism requirements, the method optimizes resource utilization and accelerates overall computation.

This advancement holds significant implications for software development, particularly in areas requiring rapid code compilation and execution. By improving the efficiency of parsing operations, ROW64’s technology can lead to faster development cycles, reduced latency in software applications, and a more responsive computing experience for end-users.

Row64’s innovative approach exemplifies how reimagining fundamental computing processes can yield substantial improvements in performance and efficiency, marking a notable step forward in the evolution of compiler technology.

Study Case

SafeMark Gas Experts (SafeMark) has been involved in gas detection in the workplace for over 40 years and offers safety solutions to America’s infrastructure and resource companies. To maintain the trust of its clients and keep its industry-leading reputation, SafeMark conducts regular R&D work.

In March of 2013, SafeMark found a need for a guard that detected flammable materials which led to the start of Project Flame Guard in April of 2013. The hypothesis for its project was that SafeMark could design and develop an examined guard with innovative features to detect flammable material in an improved manner to what currently existed on the market.

To qualify for the Research and Experimentation Tax Credit, SafeMark had to make sure its “qualified research” met four main criteria, known and developed by Congress as The Four-Part Test. After self-assessing, SafeMark declared the following experiments as R&D work.

Design and development of a series of prototypes to achieve the technical objectives (design of the examined guard).

SafeMark’s hypothesis for its experiment questioned whether it was feasible to design an examined guard to detect flammable materials that was easier to use in the field and reduced operating costs for clients.

The experiments SafeMark conducted in the design phase mainly consisted of computer modeling, conceptual engineering drawings and mathematical calculations. These experiments could only be proven effective or ineffective in the prototype development and testing phase. Following the experiments in that phase, during which the product was built and tested in various applications, the design was modified and re-tested until the desired outcome was achieved.

Background research to evaluate current knowledge gaps and determine feasibility (background research for the examined guard).

SafeMark’s eligible R&D activities during this phase of experimentation included:

- Literature search and review, including maintaining up-to-date knowledge on relevant certification and standards.

- Consultation with industry professionals and potential customers to determine the level of interest and commercial feasibility of the product.

- Preliminary equipment and resources review with respect to capacity, performance and suitability for the project.

- Consultation with key component/part/assembly suppliers to determine the factors they considered important in the design and to gain an understanding of how the design needed to be structured accordingly.

The background research conducted by SafeMark was directly related to the main objective of designing a guard capable of detecting flammable materials, therefore qualifying as R&D.

Ongoing analysis of customer or user feedback to improve the prototype design (feedback of the examined guard).

The feedback of the examined guard included:

- Ongoing analysis and testing to improve the efficiency and safety of the project.

- Ongoing development and modification to interpret the experimental results and draw conclusions that served as starting points for the development of new hypotheses.

- Commercial analysis and functionality review.

This feedback was necessary to evaluate the performance capabilities of the new design in the field and to improve any flaws in the design. There was a direct correlation between the feedback and the design process of the examined guard, making it an eligible R&D activity.

Qualified research consists of research for the intent of developing new or improved business components. A business component is defined as any product, process, technique, invention, formula, or computer software that the taxpayer intends to hold for sale, lease, license, or actual use in the taxpayer’s trade or business.

The Four-Part Test

Activities that are eligible for the R&D Credit are described in the “Four-Part Test” which must be met for the activity to qualify as R&D.

- Permitted Purpose: The purpose of the activity or project must be to create new (or improve existing) functionality, performance, reliability, or quality of a business component.

- Elimination of Uncertainty: The taxpayer must intend to discover information that would eliminate uncertainty concerning the development or improvement of the business component. Uncertainty exists if the information available to the taxpayer does not establish the capability of development or improvement, method of development or improvement, or the appropriateness of the business component’s design.

- Process of Experimentation: The taxpayer must undergo a systematic process designed to evaluate one or more alternatives to achieve a result where the capability or the method of achieving that result, or the appropriate design of that result, is uncertain at the beginning of the taxpayer’s research activities.

- Technological in Nature: The process of experimentation used to discover information must fundamentally rely on principles of hard science such as physical or biological sciences, chemistry, engineering or computer science.

What records and specific documentation did SafeMark keep?

Similar to any tax credit or deduction, SafeMark had to save documents that outlined what it did in its R&D activities, including experimental activities and business records to prove that the work took place in a systematic manner.

SafeMark saved the following documentation:

- Background research

- Meeting notes or progress reports, including internal project management issues and updates

- Conceptual sketches

- Design drawings

- Emails

By having these records on file, SafeMark confirmed that it was “compliance ready” — meaning if it was audited by the IRS, it could present documentation to show the progression of its R&D activity, ultimately proving its eligibility for the R&D credit.

Choose your state

Never miss a deadline again

Stay up to date on IRS processes

Discover R&D in your industry

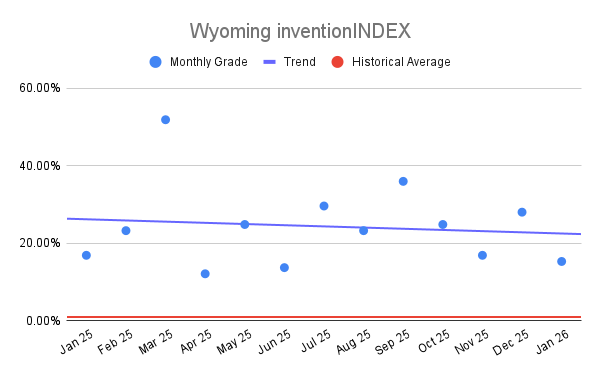

Wyoming inventionINDEX January 2026:[...]

Wyoming inventionINDEX January 2026:[...] Wyoming inventionINDEX December 2025:[...]

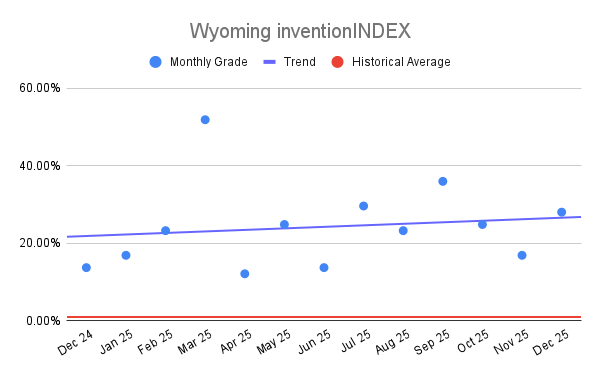

Wyoming inventionINDEX December 2025:[...]