Industry Case Studies and Regional Economic Development in Houma, Louisiana

The economic geography of Houma, Louisiana, the parish seat of Terrebonne Parish, provides a unique crucible for industrial innovation. Established in 1822 after being annexed from Lafourche Parish, Terrebonne was christened “Good Earth” by early French and Acadian settlers due to its immense agricultural fertility and abundance of estuarine resources. For its first century, the region was geographically isolated, accessible primarily via the intricate network of bayous that connect the inland marshes to the Gulf of Mexico, fostering an agrarian and maritime economy centered on sugarcane cultivation and commercial seafood harvesting. However, the economic trajectory of Houma was permanently altered in 1929 with the discovery of onshore and coastal oil and natural gas reserves. By the post-World War II era, the proliferation of offshore drilling transformed Houma into a critical logistical and manufacturing gateway for the global energy sector. This transition was cemented by the completion of the 36.7-mile Houma Navigation Canal (HNC) in 1961, which provided a direct, deep-draft conduit from the city’s industrial corridors to the open waters of the Gulf of Mexico. Today, Houma’s economy is highly specialized, anchored by an interconnected ecosystem of offshore energy services, maritime manufacturing, advanced seafood processing, coastal restoration engineering, and specialized agriculture. The following five case studies examine how these specific industries developed historically in Houma and how contemporary enterprises operating within these sectors can navigate the stringent requirements of the United States federal and Louisiana state R&D tax credit frameworks.

Offshore Oil and Gas Service and Subsea Fabrication

Historical Development in Houma

The offshore petroleum industry in Houma represents a profound narrative of post-war technological adaptation and local entrepreneurialism. Following the successful completion of the Creole platform in the Gulf of Mexico in 1938—the first successful offshore well—petroleum operators recognized the vast potential of the continental shelf. As exploration moved further from the coastline, the logistical demands required specialized marine vessels, subsea pipelines, and massive platform fabrication capabilities that traditional port cities were unequipped to handle. Local Terrebonne Parish residents and returning World War II veterans adapted surplus naval vessels and applied their innate maritime knowledge to service the burgeoning offshore platforms. Because the port of Houma historically lacked extensive overland transportation infrastructure such as robust rail and interstate highway connections, the local economy leaned heavily into marine-based fabrication and offshore logistics utilizing the waterways. As drilling operations pushed into the deeper, geologically complex salt domes and sedimentary strata of the Gulf in the late 20th century, Houma-based firms pioneered advancements in continuous geophysical surveying, underwater hyperbaric welding, and the deployment of remotely operated vehicles (ROVs). Today, Houma remains a global epicenter for companies specializing in subsea architecture and deepwater exploration logistics.

Application of the United States Federal R&D Tax Credit

Consider a hypothetical Houma-based oilfield service company employing 150 personnel that is developing a next-generation automated ROV capable of performing hyperbaric welding on subsea pipelines at extreme depths exceeding 8,000 feet. The federal R&D tax credit, governed by Internal Revenue Code (IRC) Section 41, strictly requires the taxpayer to satisfy a four-part test for qualified research.

First, the project faces intense technological uncertainty regarding pressure tolerances, material fatigue, and automated weld integrity in extreme saltwater environments, satisfying the requirement to discover information that is technological in nature and intended to eliminate uncertainty concerning the development of a new business component. Second, the engineers design multiple chassis prototypes and subject them to systematic trial and error in pressurized simulation tanks, strictly satisfying the “process of experimentation” requirement mandated by the Internal Revenue Service (IRS) Audit Techniques Guide. The wages paid to the mechanical, electrical, and software engineers performing the design work, as well as the materials and supplies consumed and destroyed during the prototyping phase, constitute Qualified Research Expenses (QREs) under IRC Section 41(b).

However, the firm must meticulously navigate the “funded research” exclusion under IRC Section 41(d)(4)(H). This specific administrative hurdle was the focal point in the recent United States Court of Appeals for the Fifth Circuit decision, Grigsby v. United States (2023). In Grigsby, the court denied federal R&D tax credits claimed by Cajun Industries LLC, an industrial contractor based in Louisiana. The court ruled that the taxpayer’s projects did not constitute qualified research because they were funded by external contracts with Chevron. Specifically, the master service agreement stipulated that all technical information, inventions, and patent rights belonged exclusively to Chevron, and Cajun Industries was guaranteed payment for services rendered regardless of the ultimate success of the research. To avoid the fate of Cajun Industries, the Houma ROV manufacturer must utilize fixed-price contracts where payment is strictly contingent upon the successful deployment and functional acceptance of the ROV, thereby forcing the economic risk of failure onto the taxpayer. Furthermore, the Houma firm must explicitly retain substantial intellectual property rights to the ROV’s welding mechanisms in its client agreements.

Application of the Louisiana State R&D Tax Credit

Under the Louisiana Research and Development Tax Credit framework codified in Louisiana Revised Statute (La. R.S.) 47:6015, the firm’s eligibility and credit amount are determined by its employee headcount and historical QRE base. Because the firm employs more than 100 individuals, it qualifies for a 5% refundable tax credit applied against the incremental increase of its current year Louisiana QREs over its base amount. For entities with 50 or more employees, the base amount is defined as 80% of the average annual qualified research expenses incurred within Louisiana during the three preceding taxable years.

To secure this credit, the firm must submit an application and a non-refundable fee (equal to 0.5% of the credit applied for, up to a maximum of $15,000) to Louisiana Economic Development (LED) for pre-claim certification. Because the firm is developing its own proprietary ROV product rather than simply fabricating parts to a customer’s exact blueprint, it operates as an original equipment manufacturer rather than a “custom fabricator,” thus avoiding the specific industry exclusions outlined in the Louisiana Administrative Code (LAC 13:I.2903). Once LED issues the formal Credit Certification, the firm may utilize the credit on its Louisiana corporate income or franchise tax return administered by the Louisiana Department of Revenue (LDR).

Shipbuilding and Marine Manufacturing

Historical Development in Houma

The shipbuilding industry in Terrebonne Parish evolved organically from the acute needs of the local commercial fishing fleet and cypress logging operations in the early 20th century. With the explosion of the offshore oil sector, traditional waterfront repair yards along the bayous transitioned into major industrial shipbuilders. Facilities such as Main Iron Works, which began operations on Main Street in downtown Houma in 1947 before relocating to the Intracoastal Waterway, became national leaders in the construction of push boats, offshore tugs, and specialty marine transport vessels. Similarly, Houma Welders (established in the 1960s and later acquired by Candies Shipbuilders) and Gulf Island Shipyards expanded their operations along the Houma Navigation Canal to construct massive towing, salvage, and university research vessels. A persistent geographic challenge driving local shipbuilding innovation is the draft limitation of the Houma Navigation Canal, which historically maintained a depth of only 15 feet. This shallow draft forces Houma naval architects to continuously innovate hull designs, propulsion systems, and weight-distribution matrixes to construct massive, high-horsepower vessels capable of navigating the shallow inland canals before entering the deep waters of the Gulf of Mexico.

Application of the United States Federal R&D Tax Credit

Consider a mid-sized Houma shipyard employing 75 personnel that is contracted to design a novel class of shallow-draft, hybrid-electric towboat. The vessel must navigate the 15-foot depth of the local canal while possessing the immense torque required to tow heavy offshore platforms, introducing severe technical uncertainty regarding hydrodynamic stability, battery bank weight distribution, and thermal management of the electric drivetrains. To resolve these uncertainties, the shipyard’s engineering team engages in a rigorous process of experimentation, utilizing advanced computational fluid dynamics (CFD) software to model various hull shapes and calculate resistance under varying payload scenarios before constructing scaled physical models. The wages paid to the naval architects and marine engineers performing the design iterations, the cost of the raw materials used to construct the physical testing models, and the cloud computing rental costs associated with running the CFD software all qualify as QREs under IRC Section 41.

Application of the Louisiana State R&D Tax Credit

While the federal tax credit application is relatively straightforward for the shipyard, the Louisiana state framework presents a severe, specific statutory obstacle. The Louisiana R&D tax credit regulations contain exclusionary rules specifically targeting businesses primarily engaged in “custom manufacturing and custom fabricating”. Because a shipyard typically builds distinct, highly customized vessels to the specific operational requirements of individual maritime clients, it falls directly into this prohibited category under LAC 13:I.2903.

However, the Louisiana legislature provided a narrow exception to this exclusion. The shipyard can circumvent the custom manufacturing prohibition if it possesses a pending or issued United States patent that is directly related to the qualified research expenditures being claimed. Therefore, to secure the state-level tax credit (which, for a 75-employee firm, equates to a 10% credit on excess QREs over 80% of its three-year average base), the shipyard’s legal counsel must strategically file a United States patent application for the novel hybrid powertrain integration or the unique hydrodynamic hull design. Upon successfully demonstrating to LED that the patent application is pending and directly covers the technology developed through the claimed QREs, the shipyard becomes eligible for the state incentive, transforming a regulatory barrier into a driver for formal intellectual property protection.

Seafood Processing and Industrial Automation

Historical Development in Houma

Long before the discovery of subterranean hydrocarbons, the commercial seafood industry was the economic lifeblood of Terrebonne Parish. The complex estuarine environment of the region naturally supports some of the most productive fisheries in the United States, allowing Houma to become a dominant force in the harvesting of brown shrimp, blue crabs, and oysters. Historically, seafood processing was a highly labor-intensive endeavor, relying on manual peeling, grading, and packing. The industry began to industrialize in the late 19th and early 20th centuries with the advent of commercial ice-making facilities and motorized trawling vessels. By the 1930s, the introduction of flash-freezing technology, blast freezers, and individual quick freezing (IQF) techniques allowed Houma processors to package shrimp in cardboard containers for nationwide distribution, effectively creating a modern, scalable export industry. Today, facing intense global competition from inexpensive foreign aquaculture imports, volatile fuel costs, and chronic domestic labor shortages, Houma processors are forced to innovate aggressively. Local firms frequently collaborate with regional academic institutions, such as the LSU AgCenter and the Louisiana Sea Grant Seafood Processing Demonstration Laboratory, to explore advanced automation technologies, artificial intelligence sorting, and the development of value-added products derived from underutilized bycatch species like garfish.

Application of the United States Federal R&D Tax Credit

Consider a family-owned Houma seafood processing facility employing 40 individuals that seeks to completely automate its shrimp grading and packaging line. Simultaneously, the company attempts to design a proprietary, automated pneumatic machine to debone garfish to create a commercially viable flash-frozen consumer product. The federal R&D tax credit rules contain strict exclusions regarding research related to style, taste, cosmetic, or seasonal design factors. Therefore, the culinary development of a new seasoning blend or the subjective taste-testing of the garfish product would be disqualified as non-technological.

However, the mechanical and software engineering required to build the automated processing equipment qualifies entirely. Integrating artificial intelligence (AI) computer-vision sensors to sort shrimp by microscopic size variations and detect translucent shell fragments involves profound technical uncertainty in the fields of optics and computer science. The engineers must evaluate different machine-learning algorithmic models and sensor calibration thresholds to eliminate the uncertainty of false-positive shell detection, constituting a systematic process of experimentation. The wages of the systems engineers, the cost of the prototype sensors, and the materials consumed during the testing phases qualify as federal QREs.

Application of the Louisiana State R&D Tax Credit

Because the seafood processing facility employs fewer than 50 individuals, it is positioned to receive the most lucrative tier of the Louisiana R&D tax credit. Under La. R.S. 47:6015(B)(2), firms with under 50 employees calculate their base amount as only 50% of the average annual Louisiana QREs over the preceding three taxable years. The firm then receives a massive 30% refundable tax credit applied against the incremental excess of current year QREs over that base amount.

Furthermore, unlike the shipyard in the previous case study, the seafood processor operates as a commercial food manufacturer producing goods for general wholesale distribution. It is not building bespoke, customized items to individual client specifications. Consequently, the firm does not fall under the restrictive “custom manufacturing” exclusion, meaning it is not statutorily required to hold a pending or issued United States patent to participate in the LED certification program. The firm simply compiles its QRE documentation, submits the application and fee to LED, receives its Credit Certification, and utilizes the 30% credit to offset its state tax liabilities or secure a refund from the LDR.

Coastal Restoration and Protection Engineering

Historical Development in Houma

The geographical existence of coastal Louisiana is currently threatened by a catastrophic land loss crisis. Over the past 80 years, the state has lost approximately 25% of the coastal landmass that was built over the previous 7,000 years of geological history. This crisis is driven by natural subsidence, global sea-level rise, the leveeing of the Mississippi River (which starves the wetlands of natural sediment replenishment), and the extensive dredging of thousands of miles of oil and gas access canals. The Houma Navigation Canal itself, while an economic engine, acts as a massive conduit for saltwater intrusion, devastating the fragile freshwater marshes surrounding Terrebonne Parish. In response to this existential threat, compounded by the devastation of Hurricanes Katrina, Rita, and Ida, Houma has evolved into a critical epicenter for a multi-billion-dollar coastal restoration engineering industry. Facilitated by funding from the Coastal Protection and Restoration Authority (CPRA), the Coastal Wetlands Planning, Protection and Restoration Act (CWPPRA), and the RESTORE Act, local civil and environmental engineering firms are pioneering advanced restoration techniques. These include massive hydrologic restoration projects, wave-dampening terracing, the beneficial use of dredged materials to construct new marsh platforms, and the design of the monumental Houma Navigation Canal Lock Complex, which integrates a massive floodgate and lock system to block storm surge and regulate salinity levels.

Application of the United States Federal R&D Tax Credit

Consider a Houma-based civil and environmental engineering firm employing 85 personnel that is contracted by a non-governmental organization (NGO) to design a novel, biodegradable geotextile matrix specifically engineered for sediment trapping and marsh creation in the high-energy wave environment of Terrebonne Bay. The firm faces severe engineering and biological uncertainties regarding how the specific polymer blends of the geotextile matrix will withstand the shear forces of Gulf storm surges while simultaneously degrading at a precise rate to allow local marsh grasses to establish deep root systems within the artificial sediment platform. The firm conducts a rigorous process of experimentation by creating scaled hydrodynamic models in specialized wave tanks to test the tensile strength and degradation rates of various prototypes under simulated hurricane conditions. The wages of the civil engineers and environmental scientists conducting the testing are valid federal QREs.

To claim the federal credit, the engineering firm must ensure its contractual arrangement is not classified as “funded research.” In the recent United States Tax Court cases Smith v. Commissioner and System Technologies, Inc. v. Commissioner (2024), the IRS aggressively challenged architectural and engineering firms, arguing their design contracts constituted funded research because they were paid for their services. The Tax Court denied the IRS summary judgment, noting that fixed-price contracts can implicitly leave the financial risk of failure on the taxpayer if payment is strictly contingent upon the successful completion of design milestones, rather than mere hourly effort. The Houma firm must structure its contract with the NGO as a fixed-price deliverable to retain the economic risk and secure the federal credit.

Application of the Louisiana State R&D Tax Credit

The Louisiana state framework poses a severe challenge for this firm. Civil engineering and architectural design are traditionally classified under administrative regulations as “professional services”. Like custom manufacturing, professional services firms are statutorily excluded from participating in the Louisiana R&D tax credit program unless they meet specific exceptions.

To secure the 10% state credit available to firms with 50 to 99 employees, the engineering firm has two potential avenues. First, it could file a United States patent application for the specific structural design and chemical composition of the biodegradable geotextile matrix, thereby satisfying the patent exception rule. Alternatively, because coastal restoration is a matter of absolute existential priority for the state of Louisiana, the firm could formally petition the Secretary of Louisiana Economic Development. The statutes grant the Secretary discretionary authority to specifically invite an otherwise ineligible business to participate in the program. If the firm receives this explicit invitation, it bypasses the professional services exclusion entirely, allowing LED to certify the research expenditures for utilization with the LDR.

Sugarcane Agriculture and Precision Farming

Historical Development in Houma

Sugarcane cultivation forms the historical bedrock of the Terrebonne Parish economy, with the region’s first recorded commercial plantation established in 1828. While the industry generated immense wealth throughout the 19th century, it faced severe existential biological threats in the late 19th and early 20th centuries from the proliferation of mosaic viruses, the destructive sugarcane borer pest, and competition from European beet sugar. Recognizing the desperate need for systematic scientific intervention, the United States Department of Agriculture (USDA) established a dedicated Sugarcane Research Laboratory in Houma in 1923. Over the ensuing century, the USDA Agricultural Research Service (ARS) Sugarcane Research Unit in Houma, operating in close collaboration with the LSU AgCenter, has led global efforts in developing high-sucrose, disease-resistant, and cold-tolerant sugarcane varieties utilizing advanced recurrent selection breeding methods. Today, the survival of sugarcane farming in Houma relies heavily on technological integration, soil science, bioinformatics, and the rapid adoption of precision agriculture techniques to maximize yields while minimizing environmental impacts.

Application of the United States Federal R&D Tax Credit

Consider a large, vertically integrated sugarcane farming and milling cooperative in Terrebonne Parish employing 200 personnel. The cooperative seeks to develop proprietary algorithmic software integrated with drone-mounted LiDAR (Light Detection and Ranging) and multispectral sensors. The objective is to autonomously measure cane stalk density, evaluate chlorophyll levels to identify nitrogen deficiencies across thousands of acres, and translate that data into real-time mechanical commands for automated, variable-rate fertilizer applicators mounted on the cooperative’s tractors.

The cooperative is not claiming a federal tax credit for the routine act of planting cane or purchasing off-the-shelf commercial drones. Rather, the technological uncertainty lies entirely in developing the proprietary algorithm capable of instantly translating raw, unstructured multispectral data into mechanical actuation commands within the harsh, unpredictable physical environment of a sugarcane field. The software engineering and data science iterations required to build, test, and refine this algorithm constitute a valid process of experimentation based in computer science.

However, the cooperative must adhere strictly to the substantiation standards emphasized in the recent Tax Court case, Moore, T.C. Memo. 2023-20. In Moore, the IRS successfully challenged a company’s substantiation of qualified time performed by high-level executives because the taxpayer failed to clearly delineate the nexus between the executives’ daily activities and the specific qualified research projects. To secure the federal credit, the Houma cooperative must maintain contemporaneous documentation—such as version control logs, software commit histories, and detailed timesheets—proving exactly how much time its chief agronomist and lead software developers spent directly performing or directly supervising the algorithm’s development, as opposed to routine farm management.

Application of the Louisiana State R&D Tax Credit

Under the Louisiana state framework, the cooperative benefits from a streamlined compliance pathway compared to the engineering and shipbuilding firms. Because the cooperative employs 200 personnel, it falls into the largest entity tier, making it eligible for a 5% refundable tax credit applied against the incremental excess of its current year QREs over 80% of its three-year historical average base amount.

Crucially, agricultural production and internal software development for agricultural use do not fall under the statutory definitions of “custom manufacturing” or “professional services”. Therefore, the cooperative is not subjected to the restrictive patent exception rule. The cooperative simply compiles its federal and state QRE documentation, submits the requisite application and fee to LED to secure its Credit Certification, and subsequently utilizes the 5% credit to offset its Louisiana corporate franchise or income tax liability via the LDR.

Detailed Analysis of the United States Federal R&D Tax Credit Framework

The United States federal R&D tax credit, originally enacted in 1981 and made permanent by the PATH Act of 2015, is codified under Section 41 of the Internal Revenue Code (IRC § 41). The legislative intent is to stimulate domestic economic growth by incentivizing taxpayers to bear the financial risk of technological innovation within the United States. The federal framework is strictly defined by statutory criteria, rigorous administrative guidance detailed in the IRS Audit Techniques Guide, and a complex, evolving body of judicial precedent.

The Statutory Four-Part Test for Qualified Research

To qualify for the federal R&D tax credit, a taxpayer’s activities must strictly satisfy the “Four-Part Test” outlined in IRC § 41(d)(1). The IRS views this test sequentially; failure to meet any single requirement completely disqualifies the activity from the credit calculation.

| Statutory Requirement | Legal Description and Application Parameters |

|---|---|

| Section 174 Requirement (Permitted Purpose) | The expenses must be of the type deductible under IRC § 174, meaning they are incurred in connection with the taxpayer’s trade or business and represent research and development costs in the experimental or laboratory sense. The research must relate to a new or improved function, performance, reliability, or quality of a business component (a product, process, computer software, technique, formula, or invention). Research related to style, taste, cosmetic, or seasonal design factors is explicitly excluded. |

| Technological in Nature | The research must be undertaken for the purpose of discovering information that is fundamentally technological. The process must rely on the principles of the hard sciences: physical sciences, biological sciences, engineering, or computer science. |

| Elimination of Technical Uncertainty | The taxpayer must intend that the information discovered will be useful in the development of a new or improved business component. Specifically, there must be technical uncertainty regarding the capability, the method, or the appropriate design of the business component at the outset of the research initiative. |

| Process of Experimentation | Substantially all of the activities (administratively defined as 80% or more) must constitute elements of a process of experimentation. The final treasury regulations dictate that this requires the taxpayer to: identify the uncertainty, identify one or more alternatives intended to eliminate the uncertainty, and identify and conduct a process of evaluating the alternatives (e.g., modeling, simulation, or systematic trial and error). |

Data Source: 26 U.S. Code § 41 and IRS Audit Techniques Guide

Categories of Qualified Research Expenses (QREs)

If the underlying activity meets the Four-Part Test, the taxpayer may aggregate the associated costs into the credit calculation. Under IRC § 41(b), Qualified Research Expenses (QREs) are generally limited to three exclusive categories:

- Wages for Qualified Services: This represents any amount paid or incurred to an employee for qualified services performed by such employee. The statute recognizes three levels of qualified services: the direct performance of qualified research (e.g., the scientist conducting the experiment), the direct supervision of the research (e.g., the lead engineer managing the testing protocols), and the direct support of the research (e.g., the machinist fabricating the physical prototype or the technician cleaning the laboratory equipment). General administrative tasks, human resources, and high-level executive management divorced from the actual science are strictly excluded.

- Supplies: Tangible personal property used and consumed in the conduct of qualified research. This category explicitly excludes land, improvements to land, and depreciable property (e.g., the purchase of a 3D printer is excluded, but the resin consumed by the printer during prototyping is a valid supply QRE).

- Contract Research Expenses: Under regulations prescribed by the Secretary of the Treasury, a taxpayer may claim 65% of any amount paid or incurred to a third-party contractor for the right to use computers in the conduct of qualified research (e.g., cloud computing rental for hydrodynamic simulations) or for the performance of qualified research on behalf of the taxpayer.

Jurisprudential Limitations: The Funded Research Exclusion

A critical area of IRS scrutiny and federal litigation involves the “funded research” exclusion defined under IRC § 41(d)(4)(H). The statute prohibits taxpayers from claiming credits for research funded by any grant, contract, or another person. The treasury regulations dictate that research is considered funded unless the taxpayer retains substantial rights to the research results and bears the economic risk of failure.

The application of this exclusion was the central issue in the Fifth Circuit Court of Appeals decision, Grigsby v. United States (2023). The taxpayer, Cajun Industries LLC, performed extensive industrial contracting and engineering services for Chevron in Louisiana. While the engineering work involved significant technical problem-solving, the Fifth Circuit upheld the denial of the tax credits. The court focused entirely on the master service agreement, noting that Cajun Industries was paid for its services regardless of the project’s ultimate success, meaning Chevron bore the financial risk. Furthermore, the contract explicitly stated that all inventions, discoveries, and patent rights conceived during the performance of the services belonged exclusively to Chevron. Because Cajun Industries lacked both the economic risk and the intellectual property rights, the research was deemed funded and legally disqualified. This case establishes a rigid precedent for Louisiana-based contractors, forcing them to adopt fixed-price, milestone-based contracts and aggressively negotiate intellectual property retention clauses if they intend to utilize the federal R&D tax credit.

Detailed Analysis of the Louisiana State R&D Tax Credit Framework

The Louisiana Research and Development Tax Credit, governed by Louisiana Revised Statute (La. R.S.) 47:6015, functions as a powerful complement to the federal credit. However, it incorporates a highly unique structural hierarchy, complex administrative hurdles, and specific industry exclusions designed to target the incentive toward particular modes of economic growth. The explicit legislative purpose of the statute is to “encourage new and continuing efforts to conduct research and development activities within this state” by providing a refundable tax credit applied against state income and corporation franchise taxes.

The Tiered Base Amount Calculation Methodology

Unlike the federal regular research credit, which relies on gross receipts to establish a historical baseline, the Louisiana state framework calculates the credit based entirely on the incremental increase of the taxpayer’s current year Louisiana QREs over a statutorily defined base amount. The state employs a tiered rate structure dependent upon the taxpayer’s total employee headcount across all affiliated companies.

| Entity Size (Employee Headcount) | Base Amount Statutory Definition | Credit Percentage Applied to Excess QREs |

|---|---|---|

| Less than 50 employees | 50% of the average annual Louisiana QREs over the 3 preceding taxable years. | 30% |

| 50 to 99 employees | 80% of the average annual Louisiana QREs over the 3 preceding taxable years. | 10% |

| 100 or more employees | 80% of the average annual Louisiana QREs over the 3 preceding taxable years. | 5% |

Data Source: La. R.S. 47:6015 and Louisiana Economic Development guidelines

Detailed Calculation Mechanics: If a firm has no previous years of R&D expenditures in Louisiana, its base amount is zero, and the credit percentage is applied to the entirety of the current year QREs. For a taxpayer with fewer than 50 employees that incurred $210,000 in current year QREs, $100,000 in the prior year, and $150,000 in the year before that, the calculation proceeds as follows: The average of the prior years is calculated ($100,000 + $150,000 / 2 = $125,000). The statutory base calculation is 50% of that average ($125,000 x 50% = $62,500). The incremental excess is determined by subtracting the base from the current year ($210,000 – $62,500 = $147,500). Finally, the 30% credit rate is applied to the excess ($147,500 x 30% = $44,250 state tax credit).

Additionally, Louisiana attempts to attract federal research dollars by offering an independent, highly lucrative 30% transferable tax credit for taxpayers who receive a federal Small Business Innovation Research (SBIR) or Small Business Technology Transfer (STTR) grant. The credit is calculated directly on the award amount received during the tax year. These specific SBIR/STTR credits are entered into the Louisiana Department of Revenue Tax Registry and may be sold or transferred to other Louisiana taxpayers, providing immediate liquidity to early-stage technology firms.

The Bifurcated Administrative Compliance Framework

A defining characteristic of the Louisiana R&D tax credit is its bifurcated administrative process. The federal system generally relies on a self-reporting mechanism where the taxpayer claims the credit on their return and retains documentation subject to future IRS audit. Louisiana, conversely, mandates a rigorous, front-end administrative approval process managed by two separate governmental entities: Louisiana Economic Development (LED) and the Louisiana Department of Revenue (LDR).

- Phase One: Certification by LED. The taxpayer cannot claim the credit on a tax return without prior authorization. The taxpayer must submit a comprehensive application to LED, accompanied by a non-refundable application fee equal to 0.5% of the tax credit applied for (with a minimum fee of $500 and a maximum of $15,000). LED evaluates the application, the federal Form 6765, and supporting documentation to verify that the activities occurred strictly within Louisiana and meet the IRC § 41 definition of qualified research. If approved, LED issues a formal Credit Certification.

- Phase Two: Utilization with LDR. Only upon receipt of the LED Credit Certification can the taxpayer utilize the credit. The certified amount is then claimed on the state income or franchise tax return administered by the LDR. If the statutory deadline to file the tax return occurs before LED completes its certification review, the Department of Revenue explicitly dictates that the taxpayer must file the return without the credit and subsequently amend the return upon receipt of the certification.

State Jurisprudence and the Board of Tax Appeals

The strict nature of Louisiana’s administrative tax laws frequently generates disputes that are adjudicated before the Louisiana Board of Tax Appeals (BTA) and the state appellate courts.

In Ampirical Solutions, L.L.C. v. State of Louisiana (2023), the Louisiana First Circuit Court of Appeal established critical procedural rights for taxpayers utilizing the program. Following a denial of its R&D credit application by LED, the taxpayer appealed. The appellate court upheld the trial court’s decision to allow a de novo trial regarding the denial, noting that because there is no specific legislative procedure outlined within La. R.S. 47:6015 for the review of an LED denial, a de novo review is required to protect the taxpayer’s constitutional right to due process.

Conversely, the BTA strictly enforces statutory waiver provisions, as demonstrated in the matter of LIPCA, Inc.. In this case, the taxpayer owed a minor tax deficiency of $3,330 for the 2012 tax year. The taxpayer participated in the Louisiana Delinquency Amnesty Act of 2013, paying the deficiency while receiving a waiver of $903 in penalties and interest. Subsequently, the taxpayer received a formal LED certification for a massive $72,452 R&D tax credit for that same 2012 tax year and attempted to amend its return to claim the refund. The Secretary of the LDR disallowed the credit. The BTA ruled in favor of the state, concluding that the statutory language of the Amnesty Act explicitly dictated that participation in the amnesty program barred the taxpayer from initiating any administrative or judicial proceeding for refunds for that specific tax period. This case highlights the profound, sometimes unintended consequences of parallel administrative tax procedures in Louisiana.

The Exclusionary “Patent Rule” for Specific Industries

Perhaps the most significant deviation between the federal and Louisiana state R&D tax credit frameworks is Louisiana’s targeted exclusion of specific industrial sectors. To focus state resources on advanced technology and product development, La. R.S. 47:6015 and the corresponding Louisiana Administrative Code (LAC 13:I.2903) strictly dictate that two types of businesses are ineligible to participate in the program: professional services firms (such as architectural and civil engineering firms), and businesses primarily engaged in custom manufacturing and custom fabricating.

However, the legislature established two narrow pathways to bypass these exclusions:

- The Patent Exception: The excluded firm may claim the credit if it has a pending or issued United States patent that is directly related to the qualified research expenditures being claimed on the application.

- The Secretarial Invitation: The Secretary of Louisiana Economic Development retains the discretionary authority to specifically invite an otherwise ineligible business to participate in the program, typically utilized for projects demonstrating massive economic impact or critical state interest, such as large-scale coastal restoration engineering.

Final Thoughts

The intersection of the United States federal R&D tax credit and the Louisiana state incentive framework creates a highly complex, lucrative compliance environment. Within the specialized industrial ecosystem of Houma, Louisiana, traditional enterprises in maritime transportation, offshore energy extraction, coastal engineering, seafood harvesting, and sugarcane agriculture are continuously forced to overcome profound engineering and environmental uncertainties through technological innovation. By meticulously adhering to the four-part test of IRC § 41, structuring client contracts to avoid the funded research exclusion, and aggressively managing the distinct administrative, exclusionary, and patent-based hurdles of La. R.S. 47:6015, enterprises within Terrebonne Parish can significantly subsidize the financial risks inherent in industrial evolution.

The information in this study is current as of the date of publication, and is provided for information purposes only. Although we do our absolute best in our attempts to avoid errors, we cannot guarantee that errors are not present in this study. Please contact a Swanson Reed member of staff, or seek independent legal advice to further understand how this information applies to your circumstances.

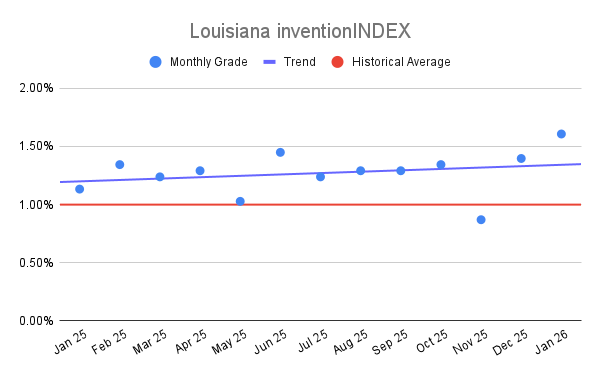

Louisiana inventionINDEX January 2026:

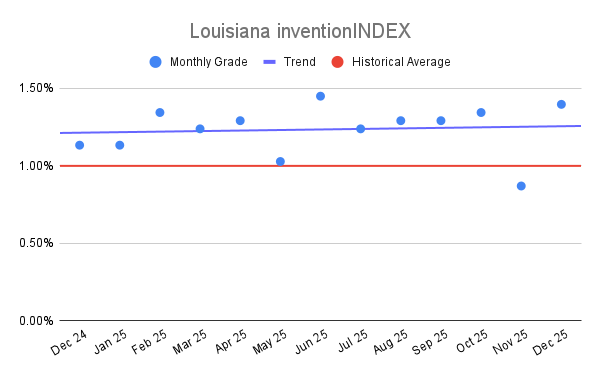

Louisiana inventionINDEX January 2026:  Louisiana inventionINDEX December 2025

Louisiana inventionINDEX December 2025