Industry Case Studies: The Evolution and Innovation of Bentonville, Arkansas

To fully comprehend the application of complex federal and state tax laws, one must first analyze the precise economic conditions that birthed Bentonville’s modern industries. Located in Northwest Arkansas, Bentonville has transformed from an isolated agricultural community into a globally recognized epicenter for retail technology, supply chain logistics, advanced food processing, specialized manufacturing, and modern healthcare. The following five case studies dissect how these specific industries developed and how hypothetical companies operating within them navigate the stringent requirements of the United States federal R&D tax credit (Internal Revenue Code § 41) and the Arkansas state R&D tax credit (Arkansas Code § 15-4-2708).

Case Study 1: Retail Technology, E-commerce, and Artificial Intelligence Software Development

The genesis of Bentonville’s dominance in retail technology traces back to a geographic anomaly. In the late nineteenth century, the first major railroad line into the region bypassed Bentonville entirely, establishing the nearby town of Rogers. To survive, local business leaders formed the Bentonville Railroad Company in 1883, constructing a six-mile link to the main line. This ethos of infrastructural self-reliance set the stage for Sam Walton, who opened the first Wal-Mart Discount City in Rogers in 1962 before establishing the corporate headquarters in Bentonville. Sparsely populated Northwest Arkansas offered a blank canvas for Walton to hone a revolutionary business model based on centralized distribution and hyper-efficient data management. As the retailer grew into the largest corporation in the world, it exerted a massive gravitational pull known as the “Supplier Effect.” While not explicitly mandated, the retail giant heavily favored suppliers who maintained a local presence, enabling rapid collaboration, synchronized merchandising, and in-person alignment with operational tempos. Today, over 1,300 major suppliers, consumer packaged goods (CPG) firms, and third-party vendors operate within a thirty-mile radius of the home office. This unprecedented concentration of global commerce generated a massive secondary market for business-to-business (B2B) retail technology, transforming Bentonville into an emergent startup geography focused on predictive analytics, omnichannel tools, and artificial intelligence. By the time the global e-commerce division was consolidated in 2010 to accelerate online channel growth and digital transformation, the local ecosystem was fully primed to support massive technological experimentation.

Consider a hypothetical Bentonville-based software startup, Ozark Retail Automation, which is developing a proprietary generative artificial intelligence (GenAI) platform. The software processes billions of distinct transactional data points to create hyper-personalized shopping experiences, dynamically adjusting digital storefronts and predicting localized inventory stockouts. From a federal tax perspective, Ozark Retail Automation must navigate the stringent four-part test established under Internal Revenue Code Section 41 (I.R.C. § 41). The company satisfies the “Permitted Purpose” requirement because it is creating a new computer software component designed to improve operational performance and reliability. The reliance on computer science algorithms and machine learning architecture satisfies the “Technological in Nature” test. However, the company faces severe technological uncertainty regarding the latency of its database queries and the accuracy of its predictive models when subjected to real-time, high-volume consumer traffic. The iterative coding, simulation testing, and algorithm refinement constitute the required “Process of Experimentation”.

Because Ozark Retail Automation is developing software, it must carefully navigate the complex federal regulations surrounding “Internal Use Software” (IUS). If the platform were being developed solely for the internal operational use of a single client, it would face a significantly higher threshold of innovation to qualify for the federal credit. However, because the firm intends to license this B2B software to multiple CPG vendors within the Bentonville ecosystem, it successfully bypasses the stricter IUS limitations. Furthermore, the firm must heed the precedent set by the United States Tax Court in Smith v. Commissioner. In this case, the IRS successfully utilized the “funded research exclusion” to deny credits to an architectural firm, arguing that the taxpayer’s clients funded the research through guaranteed contracts. To secure its federal Qualified Research Expenses (QREs)—which include the taxable wages of its software engineers and data scientists—Ozark Retail Automation must structure its vendor agreements as fixed-price contracts rather than time-and-materials agreements. The company must bear the economic risk of the software’s failure and explicitly retain substantial rights to the underlying intellectual property.

Under the laws of the State of Arkansas, this retail technology firm is exceptionally well-positioned. The Arkansas Consolidated Incentive Act 182 of 2003, amended over time, authorizes multiple tiers of R&D support. Because Information Technology is specifically identified by the Board of Directors of the Arkansas Science and Technology Authority (ASTA) as a field having long-term economic and commercial value to the state, Ozark Retail Automation can apply for the “Research and Development in Area of Strategic Value” tax credit. Upon submitting a detailed project plan and receiving approval from the Arkansas Economic Development Commission (AEDC), the startup can capture a highly lucrative 33 percent income tax credit on its qualified in-house research expenditures. While the federal credit permits the inclusion of certain cloud computing supply costs, the Arkansas Department of Finance and Administration (DFA) strictly limits strategic QREs to taxable wages and usual fringe benefits, entirely excluding supplies and equipment. Although this strategic state credit is capped at $50,000 per taxpayer annually, it provides a crucial dollar-for-dollar offset against the startup’s state income tax liability, featuring a robust nine-year carryforward provision for any unused credits.

Case Study 2: Supply Chain Operations and Transportation Logistics

The historical development of the transportation logistics industry in Northwest Arkansas is inextricably linked to both the region’s challenging topography and the meteoric rise of its retail sector. Unlike the fertile, flat expanses of the Arkansas Delta region, the hilly terrain of the Ozarks was fundamentally unsuited for large-scale row crop agriculture. This geographic limitation forced local entrepreneurs into alternative agricultural pursuits, primarily poultry farming, which subsequently demanded highly specialized, refrigerated transportation networks. In 1969, entrepreneurs Johnnie Bryan Hunt and Johnelle Hunt relocated their fledgling poultry litter operation from Stuttgart to Lowell, Arkansas—just outside Bentonville—shifting their primary focus to the trucking industry. This strategic relocation coincided perfectly with Sam Walton’s decision to build a massive centralized distribution center in Bentonville in 1970. By hauling Tyson chickens outbound and returning with retail goods for the growing discount empire, J.B. Hunt Transport Services capitalized on the region’s central location—within driving distance of massive markets in Texas, Missouri, and Tennessee—to become the nation’s largest publicly held trucking company. The federal deregulation of the trucking industry in the 1980s further removed governmental hurdles, sparking rapid growth and requiring an intense focus on operational execution, cost reduction, and fleet efficiency. Today, this legacy has spawned a dense cluster of logistics engineering firms and transportation startups dedicated to optimizing global supply chains.

Imagine a hypothetical Bentonville-based engineering firm, Ozark Freight Dynamics, which is currently engaged in the development of next-generation telematics hardware and routing software. The company seeks to optimize the final-mile delivery of heavy, bulky goods, designing sensors that monitor axle stress and autonomous routing algorithms that dynamically adjust to the extreme gradients and unpredictable weather patterns of the Ozark Mountains. From a federal taxation standpoint, the development of specialized hardware sensors qualifies as a new product business component under I.R.C. § 41. The engineers at Ozark Freight Dynamics face significant technological uncertainty regarding the durability of the sensor casings under severe vibration and the latency of the telemetry signals in rural areas lacking broadband infrastructure. Through a systematic process of prototyping, mechanical stress testing, and algorithmic refinement, the company relies heavily on the principles of mechanical engineering and computer science.

A critical component of this company’s financial strategy involves the recent federal tax code updates. Under the One Big Beautiful Bill Act (OBBBA) of 2025, Congress fully reinstated and made permanent the immediate expensing of domestic research and experimental (R&E) expenditures under I.R.C. § 174A. Prior to this legislation, the firm would have been forced to capitalize and amortize these expenses over five years, severely impacting cash flow. Now, the firm can immediately deduct the massive costs associated with domestic prototyping, while simultaneously claiming the I.R.C. § 41 R&D tax credit on the raw materials—such as circuit boards, specialized alloys, and testing apparatuses—that are physically consumed or destroyed during the experimental process.

For its Arkansas state tax strategy, Ozark Freight Dynamics benefits from the state’s aggressive recruitment of advanced logistics infrastructure. Transportation Logistics is explicitly listed as a targeted business sector under the rules governing the Arkansas Science and Technology Authority. While the company could apply for the 33 percent strategic value credit, it opts instead for the broader “In-House Research and Development” credit, which is tailored for mature, expanding firms. Administered at the discretion of the AEDC Executive Director, this program provides a 20 percent tax credit on qualified in-house research wages that exceed a historical baseline. Because Ozark Freight Dynamics recently constructed a brand-new, dedicated testing facility in Bentonville, it leverages a highly advantageous statutory loophole. Under DFA administrative rules, the initial baseline for a newly established in-house research facility is set at zero dollars ($0) for the first three years following the execution of the financial incentive agreement. Consequently, 100 percent of the eligible QREs incurred during years one, two, and three qualify for the 20 percent state tax credit. It is only in the fourth year that the rolling baseline mechanism activates, using the QREs from year three as the threshold for year four. To remain compliant, the firm must meticulously isolate its R&D payroll from general administrative staff, as state law explicitly restricts the credit to taxable wages and usual fringe benefits for employees directly performing or supervising the research, entirely excluding the materials and hardware components that qualify federally. The resulting state credit can entirely zero out the company’s Arkansas corporate income tax liability.

Case Study 3: Agricultural Biotechnology and Advanced Food Processing

Before the retail and logistics booms of the mid-twentieth century, Benton County was nationally recognized for its agrarian output, serving as the leading apple-producing county in the United States in 1901. However, as the fruit industry declined, the aforementioned rugged geography necessitated a permanent shift toward high-density livestock, establishing a massive poultry farming network across Northwest Arkansas. This regional necessity birthed global food processing conglomerates, including Tyson Foods, which anchored the industry. Today, the State of Arkansas boasts the fifth-largest percentage of food processing workers in the nation, with 522 food and beverage companies employing over 55,000 individuals. Eight of the top ten food and beverage companies globally by revenue maintain manufacturing facilities within the state. To maintain this massive output, continuous research and development is required across the entire agricultural spectrum, encompassing disease mitigation, genetic line performance, feed efficiency, and optimized packaging methodologies that increase shelf life.

Consider Northwest Agri-Genetics, a hypothetical biotechnology firm operating a research farm and laboratory on the outskirts of Bentonville. The company is developing novel, antibiotic-free poultry feed formulations intended to maximize nutrient absorption and prevent catastrophic disease outbreaks in high-density commercial flocks. Historically, many agricultural businesses falsely assumed that the federal R&D tax credit was strictly reserved for white-collar software development or precision manufacturing, entirely overlooking the biological sciences. However, the formulation of new organic feeds and the enhancement of livestock genetics directly address severe biological and technological uncertainties, fulfilling the foundational requirements of I.R.C. § 41.

The application of federal law to Northwest Agri-Genetics is profoundly shaped by the recent, landmark United States Tax Court decision in George v. Commissioner. In this case, the IRS challenged a large poultry producer’s attempt to claim R&D credits for feed additives and flock management techniques, arguing that feed costs were simply ordinary production expenses. The Tax Court firmly rejected the IRS’s position, establishing a monumental taxpayer-friendly precedent. The court validated the concept of the “pilot model” within a live agricultural setting, ruling that the broilers comprising the experimental flocks were produced explicitly to evaluate technical uncertainty. Consequently, the animals themselves, alongside the experimental feed consumed during the trial, were legally classified as qualified supply QREs.

However, the George ruling also reinforced strict documentation standards. The court refused to allow the taxpayer to estimate QREs for its base years, demanding precise records. This aligns directly with the earlier Tax Court ruling in Siemer Milling Company v. Commissioner (2019), which disallowed over $235,000 in credits because the food processor failed to retain supporting documentation proving that an actual scientific process of experimentation occurred. Simply reciting that technical activities took place is insufficient; Northwest Agri-Genetics must maintain contemporaneous laboratory notebooks detailing the control groups, the specific biological hypotheses, the methodical trial variations, and the exact biochemical outcomes of the new feed formulations.

Under Arkansas state law, Northwest Agri-Genetics operates within one of the most highly prioritized sectors. Agricultural, Food, and Environmental Sciences, alongside Biotechnology and Bioengineering, are explicitly codified as targeted areas of strategic value by the ASTA Board of Directors. By applying to the AEDC, the firm qualifies for the 33 percent Area of Strategic Value income tax credit. The interplay between federal and state law here requires sophisticated, bifurcated accounting practices. Thanks to the George decision, the firm can claim the immense costs of the experimental livestock and the raw feed as federal supply QREs. Conversely, the Arkansas DFA strictly interprets state law to exclude all supplies from the strategic credit calculation. Therefore, the state benefit is derived exclusively from the taxable wages and fringe benefits of the firm’s biologists, geneticists, and agricultural technicians, capped at the statutory limit of $50,000 per year.

Case Study 4: Advanced Composite Manufacturing and the Outdoor Recreation Industry

The late twentieth and early twenty-first centuries witnessed a dramatic cultural and economic diversification in Bentonville. Driven by massive philanthropic investments from the Walton Family Foundation, the city aggressively marketed itself as the “Mountain Biking Capital of the World”. By leveraging the unique, rugged topography of the Ozarks, the region constructed hundreds of miles of world-class, interconnected trails, sparking an explosion in tourism and outdoor recreation. This cultural rebranding successfully attracted affluent residents and specialized entrepreneurs, fundamentally altering the local industrial landscape. This environment enticed high-end bicycle manufacturers, such as Allied Cycle Works, to establish operations in Bentonville, with the explicit mission of bringing high-tech carbon fiber frame manufacturing back to the United States. Interestingly, the transition was facilitated by the existing labor pool; workers previously employed in the poultry processing industry possessed high manual dexterity and experience working with their hands, making them highly trainable for the meticulous work required in carbon fiber layup and finishing.

Consider a hypothetical Bentonville manufacturer, Ozark Composite Technologies, a firm producing elite, custom carbon-fiber bicycle frames designed for competitive gravel racing. The company is actively conducting research to scale up production, attempting to design new resin curing processes and automated carbon-cutting techniques that increase output volume without compromising the extreme structural integrity required to survive races like Unbound Gravel. Under federal tax law, the development or improvement of a manufacturing process qualifies entirely as a permitted business component. The engineers at Ozark Composite Technologies face significant technical uncertainty regarding the thermodynamic properties of alternative epoxy resins when subjected to accelerated, high-heat curing cycles. The iterative process of molding frames, altering the chemical composition of the resins, and physically stress-testing the prototypes until catastrophic failure perfectly illustrates a scientific process of experimentation.

For the federal I.R.C. § 41 calculation, the firm can claim the wages of its manufacturing engineers, the cost of the raw carbon fiber sheets and chemical resins consumed and destroyed during the test batches, and the specialized tooling required solely for the experimental molds. Notably, routine quality control testing on the production line does not qualify; the expenses must be strictly isolated to the experimental phase prior to commercial readiness.

The State of Arkansas provides a powerful dual-incentive structure for advanced manufacturers like Ozark Composite Technologies. First, as a mature manufacturing firm, the company conducts laboratory and experimental activities to develop new commercial processes, qualifying it for the 20 percent In-House Research and Development Credit. Assuming the firm has an established history of federal R&D claims, its state credit is calculated based on the incremental increase of its current-year wage QREs over its preceding year’s wage QREs, offsetting up to 100 percent of its corporate income tax liability. Second, and equally vital, the firm benefits from aggressive state sales tax exemptions. According to Arkansas DFA Revenue Legal Counsel Opinion No. 20180315, machinery and equipment purchased to create a new manufacturing facility, expand an existing plant, or replace existing machinery are entirely exempt from state sales tax. To qualify, the machinery must be utilized directly in the actual manufacturing operations, from the initial stage where raw carbon is first acted upon through to the final completion and painting of the bicycle frame. This combination—income tax credits for the intellectual labor of process improvement, and sales tax exemptions for the physical capital equipment—drastically lowers the barrier to domestic manufacturing in Bentonville.

Case Study 5: Medical Technology, Healthcare Education, and Clinical Collaboration

The most recent, and arguably most profound, evolution of Bentonville’s economy is its rapid emergence as a nexus for advanced healthcare, whole-person medicine, and clinical research. Recognizing severe regional health disparities and a national shortage of physicians, philanthropist Alice Walton initiated a massive, multi-faceted healthcare intervention. Following the establishment of the Crystal Bridges Museum of American Art in 2011—which cemented the city as a global cultural destination—she founded the Heartland Whole Health Institute in 2019 to shift the healthcare paradigm toward holistic, preventive practices. This was followed by the creation of the Alice L. Walton School of Medicine (AWSOM) in 2021. Sharing a campus with Crystal Bridges, the 154,000-square-foot medical school features state-of-the-art anatomy and simulation laboratories, medical-grade 3D printers, and virtual reality diagnostic tools. To further solidify this ecosystem, the Alice L. Walton Foundation partnered with the Washington Regional Medical System and the world-renowned Cleveland Clinic to create a new regional health system. This monumental infrastructural investment has acted as a catalyst, drawing specialized medical technology startups and clinical research organizations to Northwest Arkansas.

Consider Bentonville BioMetrics, a newly formed medical device startup developing non-invasive, wearable sensors. These devices utilize microscopic transdermal arrays to continuously monitor interstitial glucose levels and biomechanical stress data, integrating with proprietary software to formulate holistic, real-time patient health metrics. The technological uncertainties surrounding the creation of these devices are immense, including ensuring the biometric accuracy of the sensors across diverse skin types, optimizing battery miniaturization, and securing encrypted data transmission to healthcare providers. The iterative design of the hardware and the complex coding of the accompanying diagnostic software unambiguously satisfy the four-part test under federal law, classifying the project as highly sophisticated, hard-science experimentation.

Because Bentonville BioMetrics is a startup, it lacks the internal clinical infrastructure to test its devices on human subjects safely. Consequently, it must partner with the expanding local medical ecosystem for clinical validation. Under federal I.R.C. § 41, the company can claim “Contract Research Expenses.” Specifically, 65 percent of the payments made to third-party clinical laboratories or universities to conduct human trials qualify as federal QREs. To claim this, the startup must retain the economic risk of the research and hold the rights to the resulting clinical data and patents.

The State of Arkansas heavily incentivizes this exact type of public-private clinical collaboration. Authorized by the Research and Development Tax Credit Program (Arkansas Code §§ 26-51-1101 through 26-51-1105) and Act 759 of 1985, the state offers the highly specific “University-Based Research and Development” credit. If Bentonville BioMetrics formally contracts with an approved Arkansas college, state university, or qualified research organization (such as those integrated with the new medical school initiatives) to perform the clinical validation trials, the startup qualifies for a 33 percent state income tax credit on those precise qualified research expenditures. Unlike the In-House or Strategic Value credits, which rigidly restrict state QREs to internal employee wages, the University-Based credit allows the company to massively subsidize the high costs of external clinical research. To ensure compliance and claim the credit, the taxpayer must demonstrate to the DFA that the Arkansas Science and Technology Authority (ASTA) and the Arkansas Department of Higher Education have explicitly approved the expenditure as part of a “qualified research program,” and the company must attach the corresponding Certificate of Tax Credit to its state income tax return.

Comprehensive Regulatory Framework: The United States Federal R&D Tax Credit

To fully appreciate the financial mechanics utilized in the preceding case studies, a rigorous examination of the underlying statutory architecture is required. The federal R&D tax credit is one of the most significant and lucrative domestic tax incentives remaining under current United States tax law. Administered by the Internal Revenue Service (IRS), the credit serves a dual macroeconomic purpose: it aggressive lowers the capital cost of continuous innovation for domestic firms, ensuring the nation remains competitive against global technological adversaries, and it fundamentally alters corporate cash flow by directly reducing tax liabilities.

The Intersection of I.R.C. § 41 and I.R.C. § 174A

The federal incentive structure is bifurcated into two primary mechanisms: the immediate deduction of research expenses, and the calculation of the tax credit itself. The landscape of expense deductibility was drastically altered by the passage of the One Big Beautiful Bill Act (OBBBA) on July 4, 2025. Prior to the OBBBA, stringent rules required corporations to capitalize and amortize their domestic research and experimental (R&E) expenses over five years, creating significant cash flow bottlenecks for innovative startups. The 2025 legislation reinstated and made permanent the immediate expensing provisions under I.R.C. § 174A. Consequently, a business in Bentonville can now immediately deduct 100 percent of any domestic R&E expenditures paid or incurred during the taxable year.

Operating in tandem with this deduction is the actual R&D tax credit, governed by I.R.C. § 41. While I.R.C. § 174A reduces taxable income, I.R.C. § 41 provides a dollar-for-dollar reduction in the actual tax liability owed to the federal government. The credit is generally calculated as a percentage of the Qualified Research Expenses (QREs) that exceed a historically calculated base amount, rewarding companies that incrementally increase their R&D investments year over year.

The Four-Part Statutory Test

Not all scientific endeavors qualify for the federal credit. Section 41 establishes a rigorous, four-part statutory test that every specific activity must satisfy to generate eligible QREs.

- The Permitted Purpose Test (The Business Component): The research must be undertaken with the explicit intention of discovering information to develop a new or improved “business component”. A business component is strictly defined as a product, a manufacturing process, computer software, a technique, a formula, or an invention that the taxpayer intends to hold for sale, lease, license, or use in their trade or business. The intended improvement must directly relate to the component’s functionality, performance, reliability, or quality, or result in a significant cost reduction. Research undertaken merely for aesthetic, cosmetic, or seasonal design changes is explicitly excluded.

- The Technological in Nature Test: The activity must fundamentally rely on the principles of the hard sciences to discover information. Acceptable sciences include the physical sciences (chemistry, physics), biological sciences (agronomy, genetics), engineering (mechanical, civil, electrical), and computer science. Research based on the soft sciences—such as economics, market research, behavioral psychology, or humanities—does not qualify.

- The Elimination of Uncertainty Test: At the outset of the research project, the taxpayer must face genuine technological uncertainty regarding three specific factors: the capability to develop or improve the business component, the method or methodology by which to achieve the development, or the appropriate design of the final component. If the solution is already known or easily ascertainable by a competent professional in the field without experimentation, the activity fails this test.

- The Process of Experimentation Test: To resolve the identified technological uncertainty, the taxpayer must engage in a structured, systematic process of experimentation. This involves identifying the uncertainty, formulating one or more hypotheses to address it, designing and conducting scientific trials or simulations to test those hypotheses, and carefully analyzing the results to either refine the design or discard the alternative. This is often the most heavily scrutinized element during an IRS audit.

Defining Federal Qualified Research Expenses (QREs)

If a project satisfies the four-part test, the specific costs associated with that project must be quantified. Under I.R.C. § 41, there are three primary categories of federal QREs:

- Taxable Wages: The W-2 wages of employees who are directly engaging in the qualified research (e.g., engineers, coders, laboratory scientists) constitute the bulk of most claims. Furthermore, the wages of employees directly supervising the research (first-line management) and those directly supporting the research (e.g., technicians machining prototype parts, or clerks recording lab data) are fully eligible. Executive salaries and general administrative overhead do not qualify.

- Supplies: The cost of tangible, raw materials that are physically consumed, destroyed, or degraded during the process of experimentation qualifies as a supply QRE. This includes prototype materials, chemicals used in testing, and—as established in George v. Commissioner—biological assets like experimental livestock and their feed. Crucially, standard capital equipment (machinery, computers, testing apparatuses) and real property (land, buildings) are entirely excluded, as is the depreciation associated with them. Cloud computing costs utilized directly for software development environments are frequently included as supply expenses.

- Contract Research Expenses: When a taxpayer hires a third-party contractor to perform the research on their behalf, 65 percent of the invoiced costs qualify as QREs. To claim these costs, the taxpayer must bear the financial risk of the research failing (typically via a time-and-materials contract rather than a fixed-fee guarantee) and must explicitly retain substantial rights to the resulting intellectual property.

Comprehensive Regulatory Framework: The State of Arkansas R&D Tax Credits

The State of Arkansas heavily supplements the federal framework with its own targeted, incentive-based tax credits. Administered jointly by the Department of Finance and Administration (DFA), the Arkansas Economic Development Commission (AEDC), and the Arkansas Science and Technology Authority (ASTA), the state laws are explicitly designed to foster long-term commercial value and attract specific high-tech industries to regions like Bentonville.

Arkansas Code Title 15 § 15-4-2708 governs the primary R&D income tax credits, and the administrative rules explicitly state that the commission adheres to federal guidelines (the four-part test) to determine baseline eligibility. However, the state deviates significantly from the federal government regarding which specific expenses qualify and the magnitude of the credit offered. Arkansas divides its incentives into three mutually exclusive primary tiers.

The 20% In-House Research and Development Credit

This baseline program serves as a discretionary tax incentive directed at mature, established companies performing ongoing, experimental, clinical, or laboratory research within the state to develop new products or uses.

- Credit Magnitude and Offset: The credit allows for a 20 percent reduction in state corporate income tax liability based on the incremental increase of qualified research expenditures. Earned credits can offset up to 100 percent of a business’s annual state income tax liability, and any unused credits feature a generous carryforward period of up to nine years.

- The Baseline Mechanism: The incremental nature of the credit requires the establishment of a base year. For an existing facility with a history of R&D, the baseline is the amount of in-state research claimed for federal R&D tax credits during the most recent preceding year. The state credit is calculated by subtracting the preceding year’s base from the current year’s eligible QREs, and multiplying the excess by 20 percent.

- The New Facility Exemption: Arkansas offers a massive statutory advantage to recruit new firms. For a qualified business establishing a new in-house research facility (such as a logistics firm relocating to Bentonville), the initial baseline is legally set to zero dollars ($0) for the first three years following the signing of the financial incentive agreement. Therefore, in years one through three, 100 percent of all eligible QREs qualify for the 20 percent credit without any incremental reduction. The QREs incurred in year three then become the baseline to calculate the credit in year four, establishing a rolling progression.

- Strict QRE Limitations: Unlike the federal statute, the Arkansas 20% In-House credit strictly limits QREs to in-house expenses for taxable wages and usual fringe benefits specific to the research activities of employees. The DFA regulations explicitly state that the costs of supplies, materials, equipment, and buildings do absolutely not qualify.

The 33% Research and Development in Area of Strategic Value Credit

To intentionally cultivate specific knowledge-based economies, Arkansas offers a significantly higher 33 percent credit for research conducted in fields deemed to have long-term economic or commercial value to the state.

- Strategic Identification: The fields of strategic value are identified and approved within the research and development plan formulated by the Board of Directors of the Arkansas Science and Technology Authority (ASTA). Current and recent strategic sectors closely align with Bentonville’s industrial pillars, including advanced agriculture, resilient food production systems, next-generation transportation and logistics solutions, advanced energy (including the emerging lithium sector), and population health initiatives.

- Application and Limitations: A taxpayer must formally apply to the AEDC and ASTA to qualify their project. While the credit generates a massive 33 percent return on in-house wage QREs, it is statutorily capped. The maximum tax credit that may be claimed by a taxpayer under this specific strategic program is $50,000 per tax year. Like the 20% credit, it offsets up to 100 percent of tax liability, carries forward for nine years, and strictly excludes all supply and equipment costs.

The 33% University-Based Research and Development Credit

Authorized under separate legislation (Act 759 of 1985 and Arkansas Code § 26-51-1102), this program incentivizes public-private collaboration, a critical component of Bentonville’s expanding healthcare and biotechnology sectors.

- Mechanics: An eligible business that executes a contractual agreement with one or more Arkansas state colleges, universities, or other Arkansas-based qualified research organizations to perform research qualifies for a 33 percent income tax credit.

- QRE Inclusion: This is the singular exception in Arkansas law where contract research and external payments are recognized as eligible state QREs. By utilizing this program, companies can subsidize the massive costs of external clinical trials or academic laboratory analyses. The project must be approved by both the ASTA and the Department of Higher Education.

| Expenditure Category | Federal I.R.C. § 41 QRE Status | Arkansas In-House & Strategic Credit QRE Status |

|---|---|---|

| Taxable Wages (R&D Personnel) | Included | Included (Primary mechanism) |

| Fringe Benefits (R&D Personnel) | Generally Excluded (unless specifically defined) | Included |

| Supplies Consumed in Research | Included (crucial for physical prototyping) | Excluded |

| Biological Assets (Experimental) | Included (per George v. Commissioner) | Excluded |

| Capital Equipment / Buildings | Excluded | Excluded |

| Contract Research (Non-University) | 65% Included | Excluded |

| Contract Research (AR Universities) | 65% Included | Included (via independent 33% University Program) |

Documentation Standards and Judicial Scrutiny

The financial benefits outlined above are aggressively audited by both the IRS and the Arkansas DFA. Taxpayers operating in the fast-paced, agile environments of Bentonville’s retail software and logistics sectors frequently fail to secure their credits due to insufficient contemporaneous documentation. The landscape of audit defense is defined by several landmark United States Tax Court decisions.

The foundational standard for documentation was established in Siemer Milling Company v. Commissioner (2019). In this case, a food processor claimed credits for developing new flour products and improving its production lines. The Tax Court disallowed the credits entirely, ruling that the taxpayer failed to retain internal documentation proving that an actual process of experimentation occurred. The court explicitly noted that providing conclusory statements that technical activities took place, or simply reciting the steps undertaken after the fact, is legally insufficient. Taxpayers in Bentonville must maintain contemporaneous records—such as agile software sprint logs, Jira tickets detailing specific technical bugs, laboratory notebooks, and mechanical stress-test reports—that clearly demonstrate a methodical plan involving a series of trials designed to test a specific hypothesis.

For the massive ecosystem of third-party retail software vendors and CPG suppliers orbiting the corporate headquarters in Bentonville, Smith v. Commissioner represents a critical warning regarding contract structuring. The IRS frequently invokes the “funded research exception” to deny credits to contractors. The tax code mandates that if a client’s payment to a developer is not contingent on the success of the research, the research is “funded” by the client, and the developer is legally barred from claiming the R&D credit. Therefore, Bentonville suppliers must meticulously negotiate their Master Service Agreements (MSAs) and Statements of Work (SOWs). Contracts must be structured as fixed-price deliverables, ensuring the vendor bears the absolute financial risk if the technological development fails, and the vendor must explicitly retain substantial rights to the underlying intellectual property (IP) created during the project.

Finally, the recent George v. Commissioner (2024/2025) decision dramatically expanded the applicability of the credit for Bentonville’s foundational agricultural and food processing sectors. By validating that farming activities confront real technological uncertainty (e.g., genetic line performance, vaccine administration, disease outbreaks), the court confirmed that agriculture is rooted in the hard sciences. More importantly, the court approved the use of the “pilot model” rule in agricultural settings, allowing taxpayers to claim the massive costs of the animals themselves and their experimental feed as valid supply QREs under federal law. However, the court delivered a stern rebuke to taxpayers attempting to retroactively model their baseline calculations, firmly rejecting the use of estimates for base period QREs and reinforcing the demand for rigorous historical data tracking.

Final Thoughts

Bentonville, Arkansas, represents a unique crucible of American industry, evolving through sheer geographic necessity and unparalleled corporate gravity from its agricultural roots into a sophisticated, multi-disciplinary nexus of global retail technology, advanced logistics, high-tech composite manufacturing, and pioneering medical research. Both the United States federal government and the State of Arkansas offer powerful statutory mechanisms—most notably I.R.C. § 41, the reinstated OBBBA I.R.C. § 174A expensing provisions, and Arkansas Code § 15-4-2708—designed explicitly to underwrite the immense costs and technological risks associated with this continuous innovation.

For enterprises operating within the Bentonville ecosystem, maximizing R&D tax credits requires moving far beyond basic tax compliance. It demands a highly strategic alignment of human capital accounting, rigorous contract structuring to navigate funded research exclusions, and active, continuous engagement with state bodies such as the Arkansas Economic Development Commission and the Arkansas Science and Technology Authority. By intelligently leveraging the synergies between expansive federal QRE definitions, recent taxpayer-favorable court rulings, and aggressive state-level incentives tailored for new facilities and university partnerships, businesses in Bentonville can secure critical capital, driving the region’s continued technological and economic ascendancy.

The information in this study is current as of the date of publication, and is provided for information purposes only. Although we do our absolute best in our attempts to avoid errors, we cannot guarantee that errors are not present in this study. Please contact a Swanson Reed member of staff, or seek independent legal advice to further understand how this information applies to your circumstances.

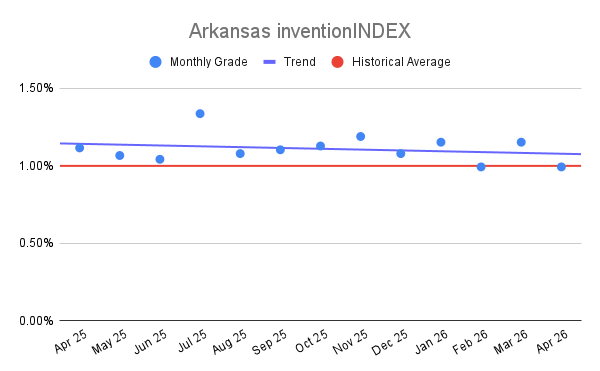

Arkansas inventionINDEX April 2026:<

Arkansas inventionINDEX April 2026:<