The Economic and Historical Development of Conway, Arkansas

To fully comprehend the specific industries that have taken root in Conway, Arkansas, and their subsequent eligibility for complex R&D tax incentives, it is necessary to examine the foundational economic history of the region. Founded in 1871 and officially incorporated shortly thereafter, Conway is located in Faulkner County and was named after a prominent Arkansas family instrumental in the state’s early development. The city’s initial economic engine was driven by its fertile land, making it a vital agricultural hub for timber and cotton. The town quickly became a center for processing and shipping these commodities, heavily reliant on its proximity to the Arkansas River for trade and commerce.

The trajectory of Conway’s economic development shifted dramatically with the arrival of the Little Rock and Fort Smith Railroad in 1879. This vital transportation infrastructure connected Conway to massive national markets, fueling an era of unprecedented economic growth, attracting new residents, and transitioning the local economy from localized agriculture to broader commercial enterprise. However, the most defining characteristic of Conway’s economic history—and the primary catalyst for its modern technology and research sectors—was an intentional, early pivot toward higher education.

In the late nineteenth century, the city’s commercial leadership, operating through the newly formed Conway Area Chamber of Commerce, recognized that sustainable economic development required intellectual capital. Rather than solely courting industrial mills, the chamber actively recruited educational institutions to stimulate the local economy and support local merchants. This strategic foresight led to the establishment of Hendrix College in 1890, Central College (which later became Central Baptist College) in 1893, and the Arkansas State Normal School (now the University of Central Arkansas) in 1907. This intense concentration of academic institutions earned Conway the enduring moniker “The City of Colleges.” For over a century, these institutions have created a permanent, localized pipeline of highly educated talent, researchers, technical professionals, and clinical practitioners, providing the foundational human capital required for intensive research and development activities.

The post-World War II era introduced another wave of deliberate economic modernization. In 1959, local business leaders established the Conway Development Corporation (CDC) with the explicit mission to attract high-paying jobs, retain growing businesses, and generate sophisticated economic development in Conway and Faulkner County. The CDC’s first major success was the creation of the Conway Industrial Park, strategically positioned adjacent to the newly constructed Interstate 40. This combination of a highly educated workforce (supplied by the three colleges), access to a major interstate logistics corridor, and proactive municipal investment created a highly fertile environment for advanced manufacturing, information technology firms, and complex healthcare systems. The synergy between academic talent and industrial infrastructure directly catalyzed the development of the five diverse industries examined in this study, establishing Conway as a premier destination for enterprises seeking to leverage federal and state R&D tax credits.

The United States Federal R&D Tax Credit Framework

The federal Credit for Increasing Research Activities, codified under Internal Revenue Code (I.R.C.) § 41, is a premier corporate tax incentive designed to stimulate domestic economic growth by rewarding businesses that invest heavily in technological innovation within the United States. Navigating this highly complex credit requires a rigorous application of statutory tests, a thorough understanding of what constitutes a qualified expense, and strict adherence to documentation standards enforced by the Internal Revenue Service (IRS) and the United States federal courts.

The I.R.C. Section 41 Four-Part Test

To qualify for the federal R&D tax credit, a taxpayer must demonstrate that their research activity satisfies all four independent elements of the statutory test established in I.R.C. § 41(d). This evaluation must be applied separately to each “business component” developed by the taxpayer. A business component is strictly defined by the tax code as any product, process, computer software, technique, formula, or invention that is to be held for sale, lease, or license, or used by the taxpayer in their own trade or business.

| Statutory Test Element | Legal Definition and IRS Application Guidelines |

|---|---|

| The Section 174 Test (Permitted Purpose) | Expenditures must be eligible to be treated as specified research or experimental expenditures under I.R.C. § 174. The research must be incurred in connection with the taxpayer’s active trade or business and represent an R&D cost in the experimental or laboratory sense. The fundamental goal must be the elimination of uncertainty regarding the development or improvement of a business component. |

| The Technological in Nature Test | The research must be undertaken for the specific purpose of discovering information that is technological in nature. The process of experimentation must fundamentally rely on principles of the hard sciences, specifically the physical sciences, biological sciences, engineering, or computer science. Research based on economics, psychology, or social sciences is strictly excluded. |

| The Business Component Test | The application of the newly discovered technological information must be intended to be useful in the development of a new or improved business component of the taxpayer. The intent to utilize the information to create a tangible commercial or operational advantage is paramount. |

| The Process of Experimentation Test | Substantially all of the research activities must constitute elements of a process of experimentation for a qualified purpose. A “qualified purpose” relates to establishing a new or improved function, enhancing performance, or increasing reliability or quality. Treasury Regulations define “substantially all” as 80 percent or more of the research activities. The process requires identifying an uncertainty, identifying alternatives to eliminate the uncertainty, and conducting a systematic evaluation of those alternatives through modeling, simulation, or trial and error. |

Internal-Use Software and the High Threshold of Innovation

The IRS places additional scrutiny on the development of computer software. If a taxpayer is developing software primarily for internal use (i.e., software not intended to be commercially sold, leased, or licensed to third parties), the activities must meet the requirements of an additional three-part “high threshold of innovation” test, as outlined in Treasury Regulation § 1.41-4(c)(6)(vi). First, the software must be highly innovative, meaning it results in a reduction in cost or an improvement in speed or other measurable metrics that is substantial and economically significant to the taxpayer. Second, the development must involve significant economic risk, meaning the taxpayer commits substantial resources to the development with substantial uncertainty that the resources will be recovered within a reasonable period. Third, the software cannot be commercially available for use by the taxpayer, meaning the taxpayer cannot purchase an off-the-shelf solution and simply install it without significant modification.

Qualified Research Expenses (QREs) and the Section 174 Capitalization Mandate

Under I.R.C. § 41(b), Qualified Research Expenses (QREs) are strictly limited to distinct categories, preventing taxpayers from claiming general overhead or marketing costs as research. The primary category is “In-House Research Expenses,” which includes taxable wages paid to employees for directly performing, directly supervising, or directly supporting qualified research. It also includes amounts paid for supplies used in the conduct of qualified research, defining supplies as tangible property other than land or improvements. The secondary category is “Contract Research Expenses,” which allows taxpayers to capture 65 percent of any amount paid or incurred to a third party (other than an employee) for the performance of qualified research on behalf of the taxpayer. If the third party is a qualified research consortium (an organized scientific research organization described in section 501(c)(3) or 501(c)(6)), the capture rate increases to 75 percent.

A critical operational paradigm shift occurred following the implementation of the Tax Cuts and Jobs Act (TCJA). Beginning in tax year 2022, I.R.C. § 174 requires companies to capitalize their R&D expenses and amortize them over five years for domestic research, or fifteen years for foreign research, rather than immediately deducting the expenses in the year they were incurred. This mandatory capitalization significantly impacts corporate cash flow, effectively raising the upfront cost of innovation for manufacturers and software developers alike. Consequently, meticulously identifying and claiming the Section 41 R&D tax credit has become mathematically imperative for businesses to offset the lost immediate deductions caused by the new Section 174 amortization rules.

United States Tax Court Jurisprudence and IRS Administrative Guidance

Recent rulings by the United States Tax Court have heavily influenced the interpretation of I.R.C. § 41, particularly regarding the documentation of the experimentation process and the definition of “funded research.” Taxpayers in Conway must navigate these precedents when preparing their credit claims.

The landmark case of Phoenix Design Group, Inc. v. Commissioner (2023) emphasized the strict enforcement of the Process of Experimentation test. In this case, the Tax Court denied R&D credits to an engineering design firm primarily because the taxpayer failed to produce robust, contemporaneous documentation demonstrating a systematic evaluation of design alternatives to overcome defined technical uncertainties. The court ruled that merely undertaking highly complex mechanical, electrical, and plumbing engineering is insufficient to qualify for the credit; there must be documented evidence of a true experimental process, such as design iteration logs, failed simulation reports, and formal testing protocols. This ruling elevated the documentation burden for all taxpayers, moving away from broad, retrospective estimations.

Conversely, in Smith et al. v. Commissioner (Docket Nos. 13382-17, 13385-17), the Tax Court provided a favorable ruling for taxpayers regarding the exclusion for “funded research” under I.R.C. § 41(d)(4)(H). The IRS had argued that an architectural design firm’s research was funded—and therefore ineligible—because the firm allegedly did not retain substantial rights to the research and was guaranteed payment regardless of the research’s success. The Tax Court denied the IRS’s motion for summary judgment, highlighting the absolute necessity of meticulously analyzing local contract law to determine if a taxpayer genuinely bears the economic risk of development. If a Conway-based software firm or manufacturer signs a fixed-price contract where they must redesign a failing product at their own cost, they bear the economic risk, and the research is not considered “funded” by the client.

Furthermore, the Supreme Court’s 2024 decision in Loper Bright Enterprises v. Raimondo fundamentally altered how the judicial branch evaluates federal agency interpretations, effectively overturning the decades-old Chevron deference doctrine. For businesses pursuing the federal R&D tax credit, this constitutional shift dramatically improves their ability to challenge overly narrow or aggressive IRS interpretations of the tax code in court. Conway businesses and their tax advisors now possess enhanced legal standing to expand eligibility parameters and protect their R&D claims from arbitrary administrative rejections.

Arkansas State R&D Tax Credit Framework

Complementing the federal system, the State of Arkansas offers a highly lucrative, multi-tiered R&D tax credit framework. Administered concurrently by the Arkansas Economic Development Commission (AEDC), the Arkansas Science and Technology Authority (ASTA), and the Department of Finance and Administration (DFA), the state incentives are designed to retain mature industrial operators while aggressively courting high-technology startups. Arkansas statutes mandate adherence to federal guidelines for determining what constitutes “qualifying research,” but the state applies entirely unique rules for calculating the base amounts, establishing credit rates, and monetizing the resulting tax credits.

Overview of Arkansas R&D Tax Incentive Tiers

Arkansas Code Annotated (ACA) § 15-4-2708 details several distinct R&D incentive programs tailored to different business life cycles and industries. A fundamental statutory provision is the “Non-Combination Rule,” which dictates that taxpayers generally cannot combine multiple in-house research incentives for the exact same expenditures, requiring businesses to strategically elect the most advantageous program.

| Arkansas R&D Program | Credit Calculation | Utilization & Monetization Rules | Eligibility & Administrative Features |

|---|---|---|---|

| In-House Research and Development (20%) | 20% of incremental qualified in-house R&D expenditures (wages and benefits) that exceed the base amount established in the preceding year. | Offsets up to 100% of annual corporate income tax liability. Unused credits carry forward for nine (9) years. Cannot be sold. | Discretionary program for mature firms. For new facilities, the base is $0 for the first three years, allowing all QREs to qualify. Supplies, equipment, and buildings do not qualify. |

| In-House Research by a Targeted Business (33%) | 33% of qualified in-house R&D expenditures (wages and benefits) incurred each year. | Can be sold one time within one year of issuance. Available for a period of up to five (5) years. | Restricted to emerging firms in six specific high-tech sectors. Prohibited from earning job creation tax credits for the same expenditures. |

| Research in Area of Strategic Value (33%) | 33% of qualified in-house R&D expenditures (wages and benefits). | Offsets 100% of tax liability. Carryforward of nine (9) years. Capped at a maximum of $50,000 per taxpayer per tax year. | Must align with an ASTA-approved R&D plan (e.g., advanced energy, lithium, steel manufacturing, next-generation logistics). |

| University-Based Research and Development (33%) | 33% of qualified research expenditures paid under contract to an Arkansas college or university. | Offsets 100% of tax liability. Carryforward of nine (9) years. | Exception to Non-Combination Rule: Can be used in conjunction with other in-house R&D credits, encouraging academic-corporate partnerships. |

Targeted Business Sectors and Administrative Prerequisites

The most lucrative Arkansas incentive is the Targeted Business program, which offers a 33% credit rate and the highly unusual ability to sell the tax credits for immediate cash. To prevent abuse, the AEDC limits this program to businesses operating squarely within six classified sectors: (1) Advanced Materials and Manufacturing Systems, (2) Agricultural, Food and Environmental Sciences, (3) Bio-Based Products, (4) Biotechnology, Bioengineering and Life Sciences, (5) Information Technology, and (6) Transportation Logistics.

The administrative burden for securing these credits is extensive. Unlike the federal credit, which is claimed retroactively on an income tax return, Arkansas credits often require prospective engagement. The business must submit a detailed application and project plan to the AEDC 45 days prior to the company’s tax year-end. This plan must identify the intent of the research, planned expenditures, timelines, and total project costs. Furthermore, claims for research credits strictly require the business to file a Certificate of Tax Credit, officially issued by the Arkansas Science and Technology Authority, alongside their state income tax return.

State Controversy, the Tax Appeals Commission, and DFA Guidance

When disputes arise regarding the validity of R&D tax credit claims in Arkansas, taxpayers must navigate the state’s specific administrative controversy framework. Effective June 30, 2023, the Arkansas legislature enacted Act 586, which closed the DFA’s internal Office of Hearings and Appeals and transferred all adjudicative functions to the newly established, independent Arkansas Tax Appeals Commission. Operating under the Department of Inspector General, the Commission provides an impartial forum for resolving disputes regarding proposed tax assessments and refund claim denials.

The Tax Appeals Commission renders decisions based on the Arkansas Code (specifically Title 26, Chapters 51 and 52 regarding income and gross receipts taxes), formal administrative rules promulgated by the DFA (Code of Arkansas Rules, Title 26, Part 30), and binding case law from the Arkansas Supreme Court. Additionally, taxpayers and their counsel frequently rely on DFA Revenue Legal Counsel opinions as persuasive authority during audits. Under Arkansas Gross Receipts Tax Rule GR-75, a taxpayer can formally request a legal opinion from the DFA to substantiate the taxation or exemption status of a specific transaction or research activity, providing a measure of prospective certainty, provided the opinion is not more than three years old. Recent proceedings before the Tax Appeals Commission in 2024 and 2025 demonstrate the Commission’s willingness to rule in favor of the taxpayer and modify DFA-proposed assessments when the taxpayer provides exhaustive, contemporaneous documentary evidence supporting their claims, reinforcing the necessity of strict record-keeping.

Industry Case Studies in Conway, Arkansas

The following five exhaustive case studies analyze specific enterprises that established operations in Conway, Arkansas. Each study details the historical drivers of their localized development and maps their highly specialized activities to the stringent requirements of both the United States federal and Arkansas state R&D tax credit laws.

Case Study: Information Technology and Data Management (Acxiom)

Historical Development in Conway: The genesis of Acxiom Corporation is intrinsically linked to the early industrial landscape of Conway. The company was founded in Conway in 1969 as Demographics, Inc. by Charles D. Ward. Ward, who also operated a local bus manufacturing business (which later evolved into IC Corporation, another major Conway employer), possessed an early mainframe computer that was severely underutilized in his manufacturing operations. Seeking to assist a political friend, Dale Bumpers, in a gubernatorial campaign, Ward utilized the mainframe to digitize electoral rolls sourced from county clerks across the state of Arkansas, effectively creating the state’s first addressable, computerized mailing list.

The success of this endeavor proved the viability of large-scale data processing. In 1978, the company was acquired by a member of management, Charles D. Morgan, who recognized the explosive potential of computer-based data management and the emerging discipline of direct-mail marketing. Renamed CCX Network, Inc., and ultimately Acxiom in 1988, the company achieved global scale by processing payrolls, managing corporate databases, and pioneering data-driven marketing. Conway provided the ideal incubator for this growth; the presence of the University of Central Arkansas supplied a continuous pipeline of computer science and business graduates, allowing Acxiom to expand into a global leader in marketing data services. Today, Acxiom maintains a massive data processing and corporate headquarters footprint in Conway, functioning as the foundational anchor of the city’s technology sector.

Federal and State R&D Tax Credit Eligibility: Acxiom’s contemporary operations involve managing trillions of monthly data records, resolving consumer identities across complex digital ecosystems without the use of third-party cookies, and developing the data foundations for AI-driven marketing campaigns.

Under federal law (I.R.C. § 41), the continuous development of proprietary algorithms for platforms like Acxiom Real ID™ comfortably satisfies the four-part test. The expenses incurred are in the active trade of data management, and the creation of new data orchestration pipelines relies fundamentally on the principles of computer science, including machine learning, cryptographic hashing, and probabilistic matching, satisfying the Section 174 and Technological in Nature tests. The core business component is the identity resolution software architecture. To overcome the immense technical uncertainties associated with accurately matching billions of fragmented data points in real-time while strictly adhering to complex, evolving data privacy regulations (such as the CCPA), Acxiom’s software engineers must iteratively design, stress-test, and optimize algorithmic models. The systematic evaluation of alternative data structures to decrease computational latency constitutes a qualified process of experimentation. If Acxiom develops proprietary database management tools exclusively for internal back-end operations, these tools must also pass the federal “high threshold of innovation” test, proving they result in substantial economic benefits and involve significant economic risk.

At the state level, Acxiom perfectly aligns with the Arkansas Targeted Business R&D Tax Credit (33%). High-level data analytics, identity resolution, and enterprise software development fall squarely under the “Information Technology” targeted sector recognized by the AEDC. Because Acxiom employs highly skilled, highly compensated software engineers and data scientists in Conway, 33% of their incremental qualified wages could be captured as a state tax credit. Historically, this incentive has allowed technology firms in Arkansas to offset up to 100% of their state income tax liability, or, remarkably, sell the credits for an immediate cash infusion to fund further data infrastructure expansion.

Case Study: Specialty Metal Wire and Tire Cord Manufacturing (Tokusen USA)

Historical Development in Conway: Tokusen USA Inc. was established in the Conway Industrial Park in 1989 as a foreign subsidiary of the diversified Japanese specialty wire manufacturer, Tokusen Kogyo Co. LTD. The massive 500,000-square-foot facility officially opened in October 1990, initially employing 160 workers to produce 300 tons of high-tensile steel cords per month for automotive tire reinforcement. The parent corporation chose Conway due to the robust industrial infrastructure established decades earlier by the Conway Development Corporation, its central geographic access to rapidly expanding automotive manufacturing plants in the American South and Midwest, and the availability of a reliable, technically capable manufacturing workforce.

Over three decades, Tokusen heavily diversified its Conway operations, expanding its product range beyond tire cords to include ultra-fine stainless steel medical wires, semiconductor materials, piano wire, and nano-silver flake for printed electronics. Although severe global market conditions, inflationary pressures, and the imposition of 25% steel tariffs ultimately forced the closure of the Conway plant in early 2025, the facility’s extensive, multi-decade history of metallurgical innovation provides a textbook example of complex manufacturing R&D.

Federal and State R&D Tax Credit Eligibility: Tokusen’s manufacturing processes were exceptionally complex, involving drawing 5.5-mm thick metal wire material down to sub-micron thicknesses. This required proprietary cold working technologies, complex stranding configurations, and highly sensitive heat treatments such as patenting and annealing.

Under I.R.C. § 41, Tokusen’s continual development of new specialty wire products was firmly rooted in metallurgy, inorganic chemistry, and mechanical engineering, satisfying the Technological in Nature test. A quintessential example of their process of experimentation was the development of the “BeCoFree” project—an award-winning, cobalt-free solution for steel cord adhesion. Historically, the tire industry relied on adding cobalt to rubber compounds to ensure the rubber bonded securely to brass-plated steel tire cords. To eliminate cobalt and create a more sustainable, greener tire, Tokusen’s engineers were forced to experiment with entirely new chemical coatings and drawing techniques. This required a rigorous scientific process: formulating alternative plating alloys, testing the tensile strength of the microscopic wires, and conducting accelerated aging tests to measure adhesion degradation over time under extreme thermal stress. Furthermore, under federal regulations, if the entirety of a massive manufacturing process does not qualify for the credit, the IRS applies the “shrink-back rule.” This allows the R&D credit to shrink back to the specific sub-component or localized process step that involved true experimentation—such as the specific electrodeposition chemical bath used exclusively for the cobalt-free wire, rather than the entire factory assembly line.

At the state level, Tokusen’s activities would have qualified seamlessly under the Arkansas In-House Research and Development Tax Credit (20%). Given the advanced nature of their medical guide wires and nano-materials, they could have also petitioned the AEDC for classification under the Targeted Business Credit (33%) within the “Advanced Materials and Manufacturing Systems” sector. Furthermore, if their development of cobalt-free tire cord or advanced medical perfusion materials was directly aligned with an ASTA-approved long-term economic development plan focusing on sustainable materials, Tokusen could have secured the Strategic Value Credit (33%).

Case Study: Automotive Diagnostics and Service Equipment (Snap-on Equipment)

Historical Development in Conway: Snap-on Incorporated, a global conglomerate renowned for professional tools and equipment, established a highly significant manufacturing and engineering presence in Conway, Arkansas. Operating out of a large-scale facility on Exchange Avenue, the Conway plant focuses heavily on the company’s undercar equipment division. Specifically, the facility is responsible for engineering and assembling complex wheel balancers, tire changers, and laser-guided alignment systems.

Snap-on’s strategic placement in Conway is a continuation of the city’s legacy in heavy capital manufacturing, sharing industrial DNA with nearby fabrication facilities. The location allows Snap-on to manufacture large, heavy capital equipment in a central, logistics-friendly location for rapid nationwide distribution. The Conway plant is deeply integrated into the company’s global product development lifecycle; it is not merely a staging ground, but an active engineering center that produces over 12,000 different models of auto service equipment and continuously customizes systems to interface with modern automotive computer networks.

Federal and State R&D Tax Credit Eligibility: As modern passenger and commercial vehicles increasingly integrate Advanced Driver Assistance Systems (ADAS), complex electronic architectures, and electric vehicle (EV) drivetrains, the service equipment required to maintain them must undergo constant, rigorous technological evolution.

Under federal law (I.R.C. § 41), Snap-on’s engineers in Conway routinely engage in qualified research that encompasses both heavy mechanical hardware and sophisticated diagnostic software development. Designing a new generation of computerized wheel balancers involves mechanical engineering, sensor physics, and software engineering, fulfilling the Business Component and Technological in Nature tests. The process of experimentation is intense. For instance, when developing alignment equipment capable of calibrating the delicate optical sensors on a new EV model, engineers face massive technical uncertainties regarding sensor accuracy, vibration isolation on the shop floor, and reverse-engineering software integration with proprietary Original Equipment Manufacturer (OEM) communication protocols. The engineering team must build iterative prototypes, utilize advanced CAD software (like AutoCAD or Inventor) to simulate structural stress on the machinery, and conduct physical, destructive trials to ensure the equipment meets strict micron-level tolerance limits. The wages paid to mechanical engineers, robotics specialists, and software developers based in Conway for this iterative design process are fully eligible QREs. Additionally, the costs of the raw steel, specialized optical sensors, and microprocessors used to build scrap prototypes of new tire changers qualify as supply QREs under federal law.

For state tax purposes, Snap-on operates as a mature, ongoing manufacturing firm, making it an ideal, textbook candidate for the Arkansas In-House Research and Development Tax Credit (20%). Because Snap-on conducts ongoing R&D year over year, they establish a baseline of historical QREs. Any incremental expenditure above that historical baseline—such as hiring a new team of automation engineers or expanding their physical testing laboratory on Exchange Avenue—would earn a 20% state corporate income tax credit. This credit can be carried forward for nine years to consistently offset the facility’s state tax liabilities, rewarding the corporation for maintaining its highly skilled engineering base within Arkansas rather than offshoring it.

Case Study: Educational and Commercial Furniture Manufacturing (Virco)

Historical Development in Conway: Virco Manufacturing Corporation is widely recognized as America’s largest manufacturer and supplier of furniture and equipment for K-12 schools, convention centers, and government facilities. Founded in southern California in 1950, Virco experienced rapid national growth and subsequently expanded its operations to Conway, Arkansas, in 1954 to meet the demands of an exploding mid-century customer base. Conway’s central geographic location was ideal for minimizing nationwide shipping costs, and its burgeoning status as “The City of Colleges” created immediate, organic synergies with Virco’s educational market focus.

Over the decades, Virco continually upgraded and expanded its domestic operations. The Conway campus grew exponentially into a massive multi-plant operation encompassing 1,750,000 square feet of manufacturing and warehousing space. Today, Virco acts as a cornerstone of Conway’s industrial sector, employing hundreds of local workers in heavy fabrication, industrial design, engineering, and logistics, proving that traditional manufacturing remains a vital part of the regional economy.

Federal and State R&D Tax Credit Eligibility: While furniture manufacturing may initially appear traditional and static, commercial educational furniture requires highly rigorous R&D regarding ergonomics, advanced material science, and safety testing under extreme, prolonged wear-and-tear conditions.

Under federal law (I.R.C. § 41), Virco’s research relies heavily on materials engineering, polymer science, and biomechanics, comfortably passing the Technological in Nature test. The company’s product development is grounded in “value-added design,” focusing on integrating complex functional mechanisms. For example, the development of the Sage Series (ergonomic seating designed for dynamic movement) or the MT Series Mobile Bench Tables (which utilize specially designed torsion bars for safe, smooth folding mechanisms) requires substantial, documented experimentation. Virco’s engineers face critical uncertainties regarding how new high-density polyethylene plastics will perform when compression-molded, or how tubular steel frames will withstand repeated dynamic loads from students over a twenty-year lifespan. The R&D process involves designing intricate CAD models, creating physical first-article prototypes, and subjecting them to rigorous destructive testing (e.g., automated drop tests, hydraulic weight limit stress tests) to achieve necessary commercial certifications like BIFMA.

Furthermore, Virco operates an innovative “Take-Back” program, launched at the Conway facility, which requires ongoing industrial engineering to optimize the recycling and repurposing of mixed plastics and metal components from out-of-service desks into entirely new products. Systematically evaluating new thermo-mechanical processes to separate and reform these complex composites qualifies as process-driven R&D under Section 41.

At the state level, similar to Snap-on, Virco operates as a mature, cornerstone manufacturer, qualifying them for the standard Arkansas In-House Research and Development Tax Credit (20%). The taxable wages and fringe benefits of their industrial designers, mechanical engineers, and the specialized technicians building physical prototypes in the Conway facility serve as highly eligible state QREs, incentivizing the company to keep its capital-intensive innovation processes anchored in Faulkner County.

Case Study: Healthcare and Medical Technology (Conway Regional Health System)

Historical Development in Conway: For over a century, the Conway Regional Health System has operated as the primary healthcare provider for Conway and the broader north-central Arkansas region. The hospital system grew in direct tandem with the city’s population boom in the late 20th century, expanding from a localized clinic into a comprehensive medical center. As Conway evolved into a technology and education hub, the hospital adapted, integrating advanced medical technologies and becoming one of the city’s largest economic forces, with over 225 physicians on staff and more than 1,900 employees. The immediate presence of universities like UCA and Hendrix College provided an invaluable, continuous stream of nursing, premed, and healthcare administration talent, allowing the health system to support clinical innovation, deploy advanced patient care delivery systems, and partner with regional health-tech accelerators.

Federal and State R&D Tax Credit Eligibility: Under federal tax law, non-profit hospitals themselves are generally exempt from corporate income tax and thus do not directly utilize R&D tax credits to offset tax liability. However, the ecosystem surrounding Conway Regional—comprising for-profit medical technology companies, specialized software developers, and private clinical research organizations that partner with, or operate within, the hospital’s network—are prime candidates for these massive incentives. Furthermore, if Conway Regional establishes a distinct for-profit subsidiary for commercializing a proprietary technology or algorithm, these credits become directly applicable to that entity.

A critical area of qualified research in the Conway healthcare sector involves the rapid development of healthcare Information Technology (IT). For example, the rapid deployment and optimization of advanced telemedicine platforms during the COVID-19 pandemic required solving highly complex technical challenges related to secure broadband data transmission, HIPAA-compliant video routing, and seamless integration with legacy Electronic Health Records (EHR) systems. Developing a “Personalized Healthcare Information Technology” (pHIT) system intended to safely integrate massive genomic test result datasets into standard EHRs requires software engineers to build entirely new knowledge-based algorithmic models for medical decision support. The rigorous process of evaluating different database architectures to ensure real-time, secure interoperability between disparate medical databases satisfies the Business Component, Technological in Nature, and Process of Experimentation requirements of I.R.C. § 41.

This sector is exceptionally heavily favored by Arkansas state law. Startup medical device and health-tech software firms participating in local commercialization programs (such as the HealthTech Arkansas accelerator, which includes Conway Regional as a strategic partner) can qualify for the Targeted Business Credit (33%) under either the “Biotechnology, Bioengineering and Life Sciences” or “Information Technology” statutory sectors. Additionally, the state offers the University-Based Research and Development (33%) credit. If a for-profit medical device company operating in Conway contracts with the nearby University of Central Arkansas (UCA) or the University of Arkansas for Medical Sciences (UAMS) in Little Rock to conduct specialized clinical trials or baseline biological research, those contract expenditures qualify for a 33% credit. Uniquely, this university-based credit can be legally combined with other in-house R&D credits, serving to maximize the state-level incentive for collaborative healthcare innovation and cementing Conway’s status as a medical research incubator.

Strategic Insights, Compliance, and Future Outlook

Maximizing the financial utility of the intersection between federal and Arkansas state R&D tax credits requires sophisticated strategic foresight, particularly in light of rapidly evolving legal precedents and administrative rules. Companies operating in Conway must proactively adapt to these complex compliance realities.

- The Amplified Importance of Contemporaneous Documentation: The federal Tax Court ruling in Phoenix Design Group serves as a stark, unavoidable warning to all businesses conducting R&D in Conway. It is no longer legally sufficient to simply prove that a highly paid employee was engaged in complex engineering or software development; the company must retain exhaustive, contemporaneous documentation (such as dated design logs, iteration tracking software, CAD file revision histories, and technical meeting minutes) that explicitly proves a systematic evaluation of alternatives occurred to resolve a technical uncertainty. Failure to produce this documentation will result in the total denial of the credit during an IRS audit.

- Navigating the Section 174 Capitalization Burden: The federal legislative requirement to amortize Section 174 R&D expenses over five years dramatically increases the immediate taxable income and tax burden on innovative companies. Consequently, meticulously securing the Section 41 federal credit, combined with capturing the highly lucrative Arkansas state credits (up to 33%), is no longer merely an aggressive tax-planning luxury; it has become a vital, defensive cash-flow preservation strategy required for corporate survival.

- Leveraging the Unique Arkansas “Monetization” Feature: For early-stage tech, biotech, and data firms in Conway that may not yet have generated a state income tax liability to offset, the Arkansas Targeted Business credit contains a highly unique, powerful legislative feature: the tax credits themselves can be legally sold one time within one year of issuance. This allows pre-revenue startups to monetize the credit immediately on the open market, providing critical, non-dilutive capital to fund ongoing engineering operations and payroll without sacrificing equity to venture capitalists.

- Contractual Scrutiny for Supply Chain Manufacturers: For major manufacturers operating in the Conway Industrial Park (like Virco and Tokusen) and massive IT contractors (like Acxiom), client service agreements and supply contracts must be meticulously drafted by legal counsel to ensure the taxpayer retains “substantial rights” to the research results and legally bears the “economic risk” of failure. As explicitly demonstrated in the Smith case, if a contract implies that payment to the manufacturer or developer is guaranteed regardless of whether the R&D succeeds or fails, the IRS will definitively classify the activity as “funded research” and completely disqualify the expenses.

Final Thoughts

Conway, Arkansas, has successfully and deliberately transformed from a nineteenth-century agricultural center into a diversified, twenty-first-century economy driven by higher education, advanced data technology, heavy manufacturing, and sophisticated healthcare. For the multitude of businesses operating within this dynamic economic ecosystem—from legacy manufacturers like Virco and Snap-on to digital pioneers like Acxiom—the United States federal and Arkansas state R&D tax credits offer unparalleled, mathematically massive financial incentives.

By strategically aligning their day-to-day engineering, software development, and manufacturing process improvement activities with the rigorous four-part statutory test of I.R.C. § 41, and by aggressively leveraging Arkansas’s generous 20% and 33% in-house and targeted credit tiers, companies in Conway can successfully offset the rising costs of innovation. However, unlocking these financial benefits requires rigorous, uncompromising adherence to IRS documentation standards, proactive operational engagement with the Arkansas Science and Technology Authority, and an acute, up-to-date understanding of evolving federal case law and state Tax Appeals Commission rulings.

The information in this study is current as of the date of publication, and is provided for information purposes only. Although we do our absolute best in our attempts to avoid errors, we cannot guarantee that errors are not present in this study. Please contact a Swanson Reed member of staff, or seek independent legal advice to further understand how this information applies to your circumstances.

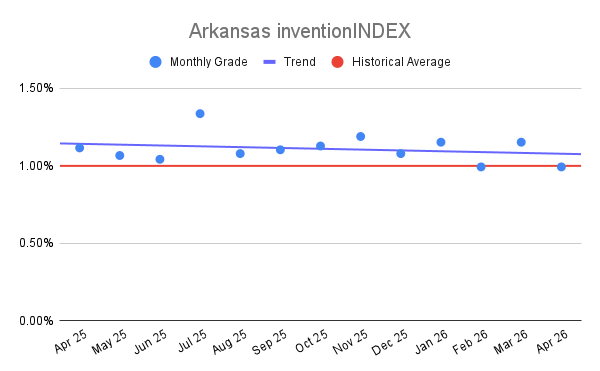

Arkansas inventionINDEX April 2026:<

Arkansas inventionINDEX April 2026:<