Answer Capsule: This comprehensive study analyzes the strategic application of federal and Arkansas state Research and Development (R&D) tax incentives within the commercial ecosystem of Fayetteville, Arkansas. It breaks down the federal four-part test for Qualified Research Expenses (QREs) under IRC Section 41 and contrasts it with Arkansas’s wage-centric, pre-approval credit programs. Through five exhaustive industry case studies—covering poultry science, supply chain logistics, nanotechnology, silicon carbide fabrication, and biomedical informatics—this resource provides critical guidance on tax compliance, audit defense, and financial modeling for technology-driven enterprises.

Introduction: The Strategic Intersection of Innovation and Tax Policy

Fayetteville, Arkansas, has undergone a profound economic metamorphosis over the past century. Originally an agrarian hub situated in the Ozark Mountains, the city has evolved into a premier nexus of technological innovation, heavily anchored by the University of Arkansas, an institution classified by the Carnegie Foundation as an “R1: Highest Research Activity” university since 2011. This academic engine, combined with the city’s aggressive campaign to establish itself as the “Startup City of the South,” has fostered a highly specialized commercial ecosystem that blends legacy industries with cutting-edge technology. The lifeblood of this ecosystem is capital, much of which is subsidized through the strategic utilization of the United States federal Research and Development (R&D) tax credit under Internal Revenue Code (IRC) Section 41, and its state-level counterparts administered by the Arkansas Economic Development Commission (AEDC), the Arkansas Science and Technology Authority (ASTA), and the Arkansas Department of Finance and Administration (DFA).

However, capitalizing on these incentives requires businesses to navigate a labyrinthine regulatory environment. Federal law relies on a retroactive, technically rigorous four-part test aimed at subsidizing the scientific method, while Arkansas state law imposes proactive administrative hurdles, pre-approvals, and stringent expenditure exclusions designed to drive local job creation. For a technology firm or agricultural enterprise operating in Fayetteville, failure to understand the fundamental divergences between the federal and state codes can result in the loss of hundreds of thousands of dollars in statutory tax relief. This study exhaustively delineates the technical parameters of both frameworks, reviews critical litigation that shapes their interpretation, and contextualizes these laws within the specific industrial history and future trajectory of Fayetteville.

The United States Federal R&D Tax Credit Framework (IRC Section 41)

The federal credit for increasing research activities, codified in IRC Section 41, was designed by the United States Congress to stimulate corporate investment in technological innovation, preventing the offshoring of highly skilled scientific jobs and maintaining American competitiveness in the global marketplace. To qualify for this non-refundable general business credit, a taxpayer must establish that their activities generate Qualified Research Expenses (QREs) by satisfying stringent statutory criteria.

The Foundational Four-Part Test for Qualified Research

Under IRC § 41(d), an activity must sequentially pass four distinct tests to be deemed “qualified research.” The Internal Revenue Service (IRS) mandates that these tests be applied separately to each “business component”—defined as a product, process, computer software, technique, formula, or invention—developed or improved by the taxpayer.

| Statutory Requirement | Legal Threshold and Administrative Interpretation |

|---|---|

| The Section 174 Test (Permissibility) | Expenditures must be treated as expenses under IRC § 174. This requires that the cost be incurred in connection with the taxpayer’s active trade or business and represent an R&D cost in the experimental or laboratory sense. Startups without current revenue may qualify if the principal purpose is to use the research results in the active conduct of a future trade or business. |

| Discovering Technological Information | The activity must be undertaken for the purpose of discovering information that is technological in nature. This strictly requires the application of principles of the hard sciences, such as physics, chemistry, biology, agronomy, engineering, or computer science. Psychological, economic, or social sciences are expressly excluded. |

| The Business Component Test | The application of the discovered information must be intended to be useful in the development of a new or improved business component of the taxpayer. The taxpayer must own or retain substantial rights to the component to utilize the results in their operations. |

| Process of Experimentation | Substantially all (interpreted administratively as 80% or more) of the activities must constitute elements of a process of experimentation. This involves a three-step cycle: identifying a genuine technical uncertainty regarding capability, method, or design; identifying alternative solutions; and conducting an evaluative process (e.g., modeling, simulation, or systematic trial and error) to eliminate that uncertainty. |

Statutory Exclusions and the Internal Use Software Limitation

Even if an activity passes the four-part test, IRC § 41(d)(4) outlines specific exclusions. Research conducted after the beginning of commercial production, adaptation of an existing business component to a particular customer’s requirement, duplication of an existing component, surveys, and routine data collection are entirely disqualified from the credit.

Furthermore, the IRS imposes a significantly higher burden of proof on computer software developed primarily for the taxpayer’s internal use. To prevent businesses from subsidizing routine IT upgrades, internal-use software must pass an additional “high threshold of innovation” test. The taxpayer must demonstrate that the software is highly innovative (expected to result in a substantial reduction in cost or improvement in speed), that its development involves significant economic risk due to technical uncertainty, and that the software is not commercially available for use by the taxpayer without modifications that would themselves satisfy the innovation criteria.

Calculating Qualified Research Expenses (QREs)

Section 41(b)(1) defines the base of the credit, known as QREs, as the sum of “in-house research expenses” and “contract research expenses”. The mathematical calculation of the credit generally equals 20% of the QREs for the current year that exceed a historically determined “base amount” (which factors in average annual gross receipts and a fixed-base percentage), or a 14% Alternative Simplified Credit (ASC) calculation.

The composition of QREs is critical for financial modeling:

- In-House Wage Expenses: Taxable wages paid to employees for engaging in the actual conduct of qualified research, engaging in the direct supervision of qualified research (first-line management), or engaging in the direct support of research activities.

- In-House Supply Expenses: Amounts paid for tangible property used in the conduct of qualified research. This includes raw materials, testing substrates, and prototypes consumed or destroyed during the experimental process. Land, depreciable property, and general administrative supplies are excluded.

- Contract Research Expenses: Generally, 65% of amounts paid or incurred by the taxpayer to an external, unrelated third party for qualified research are eligible, provided the taxpayer retains substantial rights to the research results and bears the economic risk of failure (i.e., payment is contingent on success or the taxpayer pays regardless of the outcome but retains the intellectual property). This allowable percentage increases to 75% for amounts paid to a “qualified research consortium” organized primarily to conduct scientific research.

Federal Case Law and Administrative Precedents Shaping R&D Claims

The application of IRC Section 41 is highly litigated. Federal courts have established critical precedents that dictate how taxpayers in specific industries must substantiate their claims, defining the boundaries of what constitutes legitimate scientific experimentation versus routine business operations.

The Agricultural Precedent: George v. Commissioner

The intersection of agribusiness and tax law was fundamentally clarified in George v. Commissioner, T.C. Memo. 2026-10. This Tax Court case involved an S corporation, George’s of Missouri, Inc. (GOMI), which operated a vertically integrated poultry business encompassing hatcheries, feed mills, and processing plants. GOMI engaged a tax consultancy to conduct a retroactive R&D study, subsequently claiming massive QREs—largely comprised of supply costs for feed and vaccines—based on alleged “research trials” intended to create an improved poultry product.

The court delivered a bifurcated ruling that serves as a landmark for agricultural science. First, the court affirmed that farming and agricultural activities can definitively constitute qualified research, establishing that the search for disease resistance, genetic optimization, and novel vaccination methods are rooted in the hard sciences. Crucially, the court validated the “pilot model” concept within agriculture, ruling that live animals (the chickens) and the experimental feed they consumed could be legitimately claimed as qualified supply QREs under Section 174.

However, the taxpayer ultimately lost the majority of its financial claim due to severe evidentiary failures. The court discovered irreconcilable discrepancies between the retroactive narratives crafted by the tax consultants and the contemporaneous daily business records maintained by the farm operators. While the R&D study claimed the farm was testing high-dosage antibiotic regimens, the actual daily feed logs proved the chickens received standard, routine commercial dosages. The court ruled that daily operational records hold superior evidentiary weight over post-hoc consultant reports. The lesson is unequivocal: to claim R&D credits, agricultural businesses must deploy structured experimentation led by capable personnel, and the scientific intent must be contemporaneously documented in daily logs.

Engineering, Architecture, and Contractual Risk Bearing

For engineering, architectural, and manufacturing firms, case law focuses heavily on the funded research exclusion and the presence of genuine technical uncertainty.

- In Cromwell Architects Engineers, Inc. v. United States (Eastern District of Arkansas), a Little Rock-based firm litigated to recover over $1.4 million in federal income taxes by claiming Section 41 credits for designing building envelopes, plumbing systems, and mechanical systems for complex government facilities. The government frequently challenges such claims, arguing they represent routine engineering rather than the resolution of technical uncertainty through experimentation.

- In Norwest Corp. v. Comm’r, the Tax Court clarified the funded research exclusion, establishing that payments made to a taxpayer by another party disqualify the research from tax credits if the taxpayer bears no financial risk (i.e., if they are paid on a time-and-materials basis regardless of the project’s success). Conversely, as seen in Populous Holdings, Inc. v. Comm’r, architectural design conducted under fixed-price contracts—where the firm absorbs the financial loss if the design fails or requires extensive iteration—is considered unfunded and eligible for credits, provided the design work addresses innovative technical uncertainties.

- Manufacturing process improvements were validated in Siemer Milling Co. v. Comm’r, where the Tax Court ruled that activities like shrink-wrapping and packaging can qualify for the credit if they are undertaken to resolve specific technical uncertainties in the manufacturing process through systematic evaluation.

The Arkansas State R&D Tax Credit Framework

While Arkansas statutes dictate that in-house research must first qualify under federal IRC § 41 guidelines to be eligible for state credits, the state’s administrative application, approval mechanisms, and calculation bases diverge radically from the federal code. The Arkansas R&D tax credit is not a unilateral, retroactive entitlement; it is a proactive, discretionary economic development tool administered by the Arkansas Economic Development Commission (AEDC) and the Arkansas Science and Technology Authority (ASTA).

Structural Divergence: The Explicit Exclusion of Supplies

The most profound distinction between the federal and Arkansas R&D tax credit landscapes is the definition of the expenditure base. While the federal credit permits the inclusion of supply costs (which, as demonstrated in the George case, can amount to millions of dollars in feed, chemicals, or raw materials), Arkansas law explicitly excludes supplies, equipment purchases, and facility construction costs from its standard in-house R&D credits.

Under the rules promulgated by the AEDC for the Consolidated Incentive Act of 2003, qualified research expenditures for Arkansas purposes are overwhelmingly restricted to “in-house expenses for taxable wages paid and usual fringe benefits specific to research activities of employees”. Furthermore, general contract research payments to private third parties—which qualify federally at 65%—are generally excluded from the state base unless executed with an Arkansas university. This intense wage-centricity profoundly alters corporate tax strategy. The state intentionally designed the credit this way to incentivize the localized hiring of highly compensated scientific talent within Arkansas borders, rather than subsidizing the bulk procurement of experimental materials from out-of-state vendors.

The Arkansas State R&D Tax Incentive Programs

Arkansas offers a portfolio of distinct R&D incentive tiers, each with unique caps, rates, and eligibility rules designed to target different stages of corporate maturity and specific economic sectors.

| Arkansas R&D Program | Statutory Authority | Credit Rate & Mechanism | Key Parameters, Limitations, and Exclusions |

|---|---|---|---|

| In-House Research and Development (Standard) | Ark. Code Ann. § 15-4-2708(a) | 20% of incremental QREs exceeding a baseline established in the preceding year. | Serves mature companies performing ongoing research. For a new facility, the base year is zero for the first three years. Offsets 100% of tax liability with a 9-year carryforward. Supplies, equipment, and buildings strictly do not qualify. |

| In-House Research by a Targeted Business | Ark. Code Ann. § 15-4-2708(c) | 33% of total QREs incurred each year for up to five years. | Discretionary credit for emerging firms in specific NAICS sectors (e.g., Biotech, IT, Advanced Materials, Transportation Logistics). Granted by AEDC Executive Director. Uniquely, this credit may be sold one time to another taxpayer. Supplies strictly excluded. |

| Research in an Area of Strategic Value | Ark. Code Ann. § 15-4-2708(d) | 33% of total in-house QREs. | For research in fields deemed to have long-term economic or commercial value to the state, as identified in an ASTA-approved R&D plan. Strictly capped at a maximum of $50,000 per taxpayer annually. |

| University-Based Research and Development | Ark. Code Ann. § 26-51-1102 | 33% of qualified research expenditures or 33% of the cost of donated machinery. | For eligible businesses contracting with an Arkansas college or university (e.g., University of Arkansas). Critically, this program uniquely allows for the donation of new machinery or equipment below cost to qualify for the credit, bypassing the standard equipment exclusion. |

The Administrative Mandate: Pre-Approval and Certification

Unlike the federal credit, which is calculated and claimed retroactively on an amended or current-year Form 6765, the Arkansas system requires proactive administrative engagement. An out-of-state business relocating to Arkansas cannot even receive a certificate until it is incorporated in the state, physically relocated, and actively conducting research within state lines.

To claim the credits on the DFA’s AR1000TC Schedule of Tax Credits, a business must possess a formal “Certificate of Tax Credit” issued by the ASTA or AEDC. This certificate is granted only after the submission and approval of a comprehensive project plan detailing the research intent, timelines, and projected payroll costs. Consequently, failure to initiate a formal dialogue and sign a financial incentive agreement with the AEDC prior to or concurrently with the commencement of the research activity permanently precludes state-level tax relief for those initial expenditures.

Arkansas State Case Law and Revenue Legal Counsel Opinions

Tax controversies in Arkansas are adjudicated by the Arkansas Tax Appeals Commission, which strictly interprets the statutes found in Title 26 of the Arkansas Code and the administrative rules promulgated by the DFA in the Code of Arkansas Rules (CAR). Taxpayers cannot rely on federal eligibility alone to win state disputes.

For guidance, taxpayers may request legal opinions from the DFA Revenue Legal Counsel regarding the taxability of a transaction or the eligibility of a specific research activity under Arkansas Gross Receipts Tax Rule GR-75. However, these opinions are subject to strict limitations; they may only be relied upon by the specific taxpayer to whom they are addressed, and they expire automatically after three years.

When disputes escalate to the judicial level, the Arkansas Supreme Court applies state law with rigid adherence to statutory text, regardless of external consequences. In Hudson v. Murphy Oil USA, Inc., the court ruled in favor of a taxpayer seeking a massive refund related to the apportionment of nonbusiness interest expenses following a corporate spinoff. The DFA argued that granting the refund in Arkansas would force the taxpayer to amend returns in multiple other states, creating unfairness. The Supreme Court decisively rejected this argument, stating its sole duty was to apply Arkansas law, unconcerned with the resulting tax implications in other jurisdictions. This precedent reinforces that for R&D claims, the specific textual limitations of the Arkansas Consolidated Incentive Act will always preempt broader federal tax theories.

Fayetteville’s Economic and Historical Evolution: From Agriculture to Innovation

To accurately analyze the application of R&D tax laws in Fayetteville, one must understand the city’s unique economic trajectory. Located in the Boston Mountains within the Ozarks, Fayetteville’s rugged topography historically prevented the widespread cultivation of traditional row crops like cotton and rice that dominated eastern Arkansas. This geographic limitation forced early 20th-century farmers to pivot toward alternative agricultural pursuits, primarily timber, fruit orchards, and poultry.

In 1953, the Arkansas General Assembly rechristened the state “The Land of Opportunity,” a moniker intended to signal a departure from rural traditions toward modern economic development. While aspirational for much of the state, Northwest Arkansas (NWA) manifested this vision. Between 1930 and 1975, the region became the adopted home of risk-taking visionaries who revolutionized American industry. Missourian John W. Tyson established a vertically integrated poultry operation in neighboring Springdale in 1931. Sam Walton launched a retail empire in Bentonville, and J.B. Hunt founded a transportation giant in Lowell. The geographical clustering of these massive enterprises necessitated sophisticated supply chains, creating a regional economic engine that demanded technological advancement.

The catalyst for Fayetteville’s modern technological dominance is the University of Arkansas. Originally established in 1871 as the Arkansas Industrial University under the Morrill Land-Grant College Act, the institution transitioned aggressively toward becoming a research-centered powerhouse in the late 20th century. This shift was formally recognized when the Carnegie Foundation classified the university as “R1: Highest Research Activity” in 2011.

To commercialize faculty research and attract high-tech industry, the university established the Arkansas Research and Technology Park (ARTP) in South Fayetteville. The ARTP has become an unparalleled economic incubator; in the 2023–2024 academic year alone, it generated a $346.3 million economic impact for the state, supporting 30 tenant companies that employ over 430 Arkansans and generating $10.6 million in state and local taxes. Combining this infrastructure with the city’s 2016 declaration to become “The Startup City of the South”—supported by entities like Startup Junkie Consulting and the Ark Angel Alliance—Fayetteville has successfully cultivated a highly specialized commercial ecosystem deeply reliant on R&D tax incentives to sustain its growth.

Exhaustive Industry Case Studies: Tax Credit Application in Fayetteville

The following five case studies provide a granular analysis of how specific industries—deeply rooted in Fayetteville’s history—navigate the intersection of their technological mandates with the complex realities of federal and Arkansas state R&D tax credit laws.

Case Study: Poultry Science, Genetics, and Agricultural Technology

Historical Development in Fayetteville: The poultry industry is inextricably linked to Fayetteville’s identity. In 1893, Millard Berry of Springdale acquired an incubator to raise chickens on a large scale, and by 1914, the Aaron Poultry and Egg Company arrived in Fayetteville seeking contract farmers. Over the decades, local hatchery men engaged in meticulous selective breeding; Jeff Brown developed the Eureka Broadbreast in 1946, followed by the LedBrest Cockerel in 1958, and Peterson Industries introduced the Peterson Male line, which captured 70% of the U.S. market in the 1970s. To support this booming agribusiness sector, the University of Arkansas established the College of Agriculture in 1905, later renamed the Dale Bumpers College of Agricultural, Food and Life Sciences in honor of the former U.S. Senator and Governor. Senator Bumpers secured over $80 million in federal funding to build the John W. Tyson Building, the Poultry Health Laboratory, and the USDA-ARS Poultry Production Research Unit right on the Fayetteville campus.

Applied Tax Case Study: Genetic Modeling for Pathogen Resistance AgriFowl Genetics LLC, an agribusiness operating a research farm adjacent to the U of A agricultural experiment station, is developing a proprietary broiler feed formulation combined with a novel, aerosolized vaccination delivery mechanism designed to enhance resistance to highly pathogenic avian influenza without the use of standard prophylactic antibiotics. The technical uncertainty lies in the precise biochemical dosing ratios, the survivability of the vaccine within an aerosolized state, and the bioavailability of the organic feed compounds within the chicken’s digestive tract over a six-week maturation cycle.

- Federal Eligibility and Case Law Application: Under IRC § 41, the development of the new feed and vaccine regimen clearly passes the four-part test. The activity is technological in nature (biology, chemistry, agronomy), seeks to create a new business component (an improved broiler genetic line and feed product), and relies on a systemic process of experimentation encompassing control groups, blood sampling, and biometric tracking. Critically, following the precedent established in George v. Commissioner, the actual live chickens used in the trials (the “pilot models”) and the massive quantities of experimental feed consumed constitute fully eligible supply QREs.

- Arkansas State Eligibility and Strategic Limitations: As an established firm with an ongoing research program, AgriFowl would logically apply for the 20% In-House R&D credit. However, Arkansas law strictly diverges from the federal standard here. The immense costs of the live chickens, the experimental feed, and the specialized laboratory equipment—which account for the vast majority of their federal claim—are completely excluded from the state credit base. AgriFowl may only claim the taxable wages and fringe benefits of the geneticists, farm technicians, and direct supervisors conducting the trials within Fayetteville.

- Compliance Warning: AgriFowl must meticulously heed the warning of the George case. If the DFA or IRS audits their claim, the tax consultants’ retroactive R&D study will be insufficient. The firm must ensure that the daily barn records, feed logs, and dosage tracking sheets maintained by their Fayetteville farm hands explicitly reflect the experimental scientific methodologies, rather than reading like routine commercial production logs.

Case Study: Supply Chain Optimization and Logistics Technology

Historical Development in Fayetteville: Northwest Arkansas emerged as a global business powerhouse primarily because of its legacy as a dense supply chain cluster. The massive, simultaneous growth of Walmart in Bentonville and Tyson Foods in Springdale necessitated advanced, high-volume movement of goods. In response, J.B. Hunt Transport Services was founded in nearby Lowell, rapidly becoming a Fortune 500 logistics leader. Recognizing the critical need for a highly educated workforce to manage these complex networks, the U of A established the federal Mack-Blackwell Transportation Center and the Supply Chain Management Research Center at the Sam M. Walton College of Business. This academic-industrial partnership spawned a massive local logistics technology sector in Fayetteville, pioneering advancements in freight packaging barcoding, transponder communication, and data-driven procurement routing.

Applied Tax Case Study: Predictive AI Freight Routing Software Ozark FreightTech, an enterprise software firm located in the Fayetteville Commerce District, is developing a proprietary artificial intelligence (AI) and machine learning algorithm designed to dynamically optimize commercial truck routing across the United States. The algorithm attempts to ingest real-time macroeconomic data, localized weather patterns, dynamic traffic conditions, and proprietary driver feedback systems to predict and prevent fuel inefficiencies and supply chain bottlenecks before they occur.

- Federal Eligibility and Case Law Application: Software development is heavily scrutinized by the IRS under § 41. If the software is intended for sale, lease, or licensing to third-party logistics firms, it follows the standard four-part test, with the software engineers’ iterative coding cycles qualifying as a process of experimentation. However, if Ozark FreightTech is developing this software for internal use (e.g., they operate their own fleet of trucks and use the software to route them), it must pass the rigorous three-part “high threshold of innovation” test. This requires proving that the AI algorithm is highly innovative (resulting in massive cost reduction), involves significant economic risk, and is not commercially available off-the-shelf. The wages of the software engineers and data scientists modeling the AI logic are prime QREs.

- Arkansas State Eligibility and Strategic Maximization: Because software development is an inherently intellectual pursuit highly reliant on human capital (wages) and requires virtually no physical supplies, the Arkansas R&D credit framework is exceptionally lucrative for this sector. Ozark FreightTech could apply to the AEDC for the 33% Targeted Business In-House Research Credit, as “Information Technology” and “Transportation Logistics” are explicitly codified as targeted business sectors. Upon approval by the AEDC Executive Director, the company can offset 100% of its state income tax liability with the wages paid to its Fayetteville-based developers. Furthermore, unlike the standard 20% credit, this 33% targeted credit may be sold one time to another taxpayer, providing immediate liquidity to a startup that may not yet have a state tax liability.

Case Study: Nanotechnology and Advanced Material Sciences

Historical Development in Fayetteville: Over the past two decades, the University of Arkansas has made aggressive, targeted investments to become a global leader in nanoscience. This effort culminated in the opening of the state-of-the-art Nanoscale Material Science and Engineering Building in 2011. Directed by Gregory Salamo, the Institute for Nanoscience and Engineering operates with the specific mission to develop Arkansas-based businesses utilizing materials built “one atom at a time”. This world-class infrastructure has led to a fertile environment for interdisciplinary startups at the ARTP, bridging the gap between molecular biology, physical chemistry, and engineering to solve localized and global issues, ranging from agricultural drift to advanced water treatment.

Applied Tax Case Study: Cellulose-Based Water Filtration Membranes Fayetteville NanoSolutions, a startup spun out of the U of A’s Materials Science and Engineering program and currently housed in the ARTP Genesis Technology Incubator, is designing a tunable, polymer-based nanotechnology membrane. The goal is to filter dangerous toxins produced by harmful algal blooms from local water sources, similar to research previously conducted on Lake Fayetteville. The profound technical uncertainty involves chemically tuning the polymer base at the nanoscale to achieve a 99.9% purification rate without causing rapid membrane degradation or clogging under high-volume water pressure.

- Federal Eligibility and Case Law Application: This research represents quintessential hard-science R&D. The formulation of new chemical polymers and the iterative testing of membrane durability in laboratory conditions constitute a robust, undeniable process of experimentation. Federally, the startup can claim the taxable wages of its doctoral researchers, the cost of the raw laboratory chemicals and testing substrates (supplies), and potentially computer rental or cloud-computing costs utilized strictly for theoretical molecular modeling.

- Arkansas State Eligibility and Strategic Limitations: As a highly specialized, emerging technology firm, Fayetteville NanoSolutions is an ideal candidate for the 33% Research in an Area of Strategic Value credit. Advanced materials and environmental sciences unequivocally fall under fields having long-term economic value to the state, subject to ASTA board approval. However, the strategic value credit is strictly capped by statute at a mere $50,000 per taxpayer per year. For a highly capitalized startup, this cap is severely restrictive. To circumvent this limitation and maximize state benefits, the startup should alternatively structure its operations to utilize the 33% University-Based Research and Development credit. By formally contracting with the U of A’s Institute for Nanoscience to conduct portions of the testing using the university’s advanced clean rooms, the startup can leverage world-class infrastructure while subsidizing the cost through state tax relief, bypassing the $50,000 strategic cap.

Case Study: Power Electronics, Energy, and Silicon Carbide (SiC) Fabrication

Historical Development in Fayetteville: In direct response to the massive 2003 Northeast Blackout that exposed severe vulnerabilities in the U.S. electrical grid, the U of A established the National Center for Reliable Electric Power Transmission (NCREPT) in 2005, located at the ARTP. Directed by Distinguished Professor Alan Mantooth, NCREPT rapidly evolved into the highest-powered university test facility in the nation, capable of testing power electronic circuits at operating levels up to 13.8 kV and 6 MVA. Building on this foundational expertise, Fayetteville became a global hub for Silicon Carbide (SiC) semiconductor research—a critical strategic material that outperforms basic silicon in high-temperature, high-voltage energy transmission. This expertise culminated recently in the establishment of the Multi-User Silicon Carbide Facility (MUSiC), the only openly accessible semiconductor fabrication facility of its kind in the United States, positioning Arkansas at the absolute forefront of the national push to onshore semiconductor manufacturing driven by the federal CHIPS and Science Act.

Applied Tax Case Study: Heavy-Duty Vehicular Traction Inverters Ozark Power Electronics, collaborating with the NCREPT facility and drawing talent from the MUSiC fab, is developing an 88 kW SiC-based vehicular traction inverter designed specifically for heavy-duty electric trucks and hybrid-electric aircraft. The paramount engineering challenge is to create a solid-state device capable of continuous, safe operation in a 140°C ambient temperature environment. The engineering team must systematically design, fabricate, and test advanced packaging solutions to prevent catastrophic thermal failure at distribution-level voltages.

- Federal Eligibility and Case Law Application: The iterative design, fabrication, and extreme thermal stress testing of the SiC inverter prototypes perfectly align with the core requirements of IRC § 41. The materials required to build these 15 kV-class prototypes—specifically the raw silicon carbide wafers and specialized thermal packaging materials—are extraordinarily expensive. Federally, these materials qualify as lucrative supply QREs, provided they are consumed in the destructive testing process or lack alternative commercial value if the prototype fails.

- Arkansas State Eligibility and Strategic Maximization: Because Arkansas law explicitly excludes the “purchase or rehabilitation of production machinery and equipment” from its standard in-house credits, Ozark Power Electronics faces a significant financial challenge. The state will heavily subsidize the wages of their electrical engineers, but the exorbitant costs of the testing apparatus and SiC wafers are excluded. However, there is a strategic loophole. If the company formally donates new, state-of-the-art testing machinery to the NCREPT facility (which qualifies as an educational institution) to facilitate joint testing, they may claim a 33% state tax credit on the cost of the donated equipment under the University-Based Research program (Ark. Code Ann. § 26-51-1102). This allows the firm to effectively subsidize its capital expenditures while enriching the university’s research capabilities.

Case Study: Biomedical Informatics and Healthcare Technology

Historical Development in Fayetteville: The foundation of medical science in Arkansas began in 1879 when Dr. P.O. Hooper and a group of physicians pooled $5,000 to establish the first medical school in Little Rock. This institution eventually became the University of Arkansas for Medical Sciences (UAMS). While UAMS is headquartered in the capital, its aggressive expansion into Northwest Arkansas has fundamentally altered the regional healthcare landscape. In 2019, the Northwest Arkansas Council released a comprehensive assessment aiming to transition the region into a “health care destination,” fostering an interdisciplinary research institute and dramatically expanding graduate medical education. Consequently, biotechnology and healthcare informatics have surged in Fayetteville, heavily supported by academic incubators like UAMS BioVentures. These incubators help commercialize faculty research in toxicology, pharmacogenomics, and evidence-based pharmacy benefits, such as the highly successful RxResults program designed to evaluate clinical equivalence and efficacy.

Applied Tax Case Study: Pharmacogenomic Data Processing Algorithms BioOzark Analytics, a bioinformatics startup, is developing a complex digital platform that dynamically cross-references massive datasets of patient genomes against FDA-approved pharmaceutical efficacy rates to predict and prevent adverse drug reactions. The process of experimentation involves creating novel algorithms that can synthesize raw, unstructured genomic sequencing data with current medical literature faster and more accurately than existing commercial diagnostic software.

- Federal Eligibility and Case Law Application: The development of the core algorithm involves advanced computer science and bioinformatics, decisively passing the “technological in nature” test. If BioOzark Analytics lacks the internal laboratory infrastructure and must outsource the actual physical genomic sequencing of biological samples to a private, third-party clinical laboratory in another state, they may claim 65% of contract research payments as federal QREs. This is contingent upon the startup retaining the intellectual property rights to the resulting data and bearing the financial risk of the research.

- Arkansas State Eligibility and Strategic Maximization: General contract research payments to private third parties are broadly excluded from Arkansas in-house credits. Therefore, the massive payments made to private out-of-state clinical labs will yield zero state tax benefits. To optimize their tax position, BioOzark Analytics must strategically restructure its vendor relationships. By contracting specifically with UAMS Northwest or the U of A to perform the genomic sequencing, the startup utilizes the 33% University-Based Research and Development program. Under this specific program, payments made to these Arkansas-based public institutions become fully eligible for the state credit. Furthermore, as a biotechnology firm, their internal software developers’ wages would qualify under the 33% Targeted Business In-House R&D credit, allowing the company to aggressively scale its Fayetteville workforce with heavy state subsidization.

Strategic Compliance, Audit Defense, and Financial Modeling

For corporate taxpayers, Chief Financial Officers, and tax practitioners operating in Fayetteville, navigating the complex interplay between federal audits and state administrative appeals requires rigorous, proactive risk management. The assumption that federal eligibility automatically guarantees state tax relief is a profound, often costly, misconception.

The Preeminence of Contemporaneous Documentation

The U.S. Tax Court’s ruling in George v. Commissioner underscores a critical vulnerability for taxpayers across all technological sectors: the disparity between retroactive tax credit studies and daily operational reality. Firms operating within Fayetteville’s ARTP or the broader commerce district cannot simply rely on sanitized, annual summaries drafted by external tax consultants.

Engineers, biological scientists, and software developers must be trained to maintain rigorous daily logs, version control histories (e.g., GitHub commits for software development), and laboratory notebooks that explicitly state the technical uncertainties being tested, the hypotheses, and the results of those specific experiments. If the Arkansas DFA or the federal IRS audits a claim, these raw, contemporaneous records will carry the absolute highest evidentiary weight. If the raw data contradicts the polished narrative in the tax study, the entire credit claim can be invalidated, resulting in massive financial clawbacks and accuracy-related penalties.

Entity Structuring and Pass-Through Nuances

Fayetteville’s ecosystem is dominated by startups and scaling enterprises that often operate as pass-through entities (S-Corporations, Partnerships, and LLCs). These corporate structures face unique complexities in tax administration. As highlighted by regional tax advisory firms, pass-throughs must determine R&D eligibility and calculate the credit base at the entity level, but the actual financial benefit is allocated to the individual owners based on their ownership percentage.

In instances of corporate restructuring, mergers, or spinoffs—a highly common occurrence as successful startups graduate out of the U of A incubators and are acquired by larger entities—taxpayers must carefully navigate complex state apportionment rules. While the Arkansas Supreme Court case Hudson v. Murphy Oil USA, Inc. primarily dealt with nonbusiness interest expenses related to a corporate spinoff, the ruling powerfully reaffirmed that the Arkansas judiciary will strictly, literally apply Arkansas statutory definitions of income, deductions, and credits, completely regardless of how those financial items are apportioned or treated in other state jurisdictions.

Final Thoughts

Fayetteville, Arkansas, has strategically engineered a civic and academic economy perfectly suited to capitalize on local and federal Research and Development tax incentives. From the deep historical roots of poultry science and logistics optimization to the cutting-edge silicon carbide fabrication occurring at the MUSiC facility today, the city’s diverse industries are deeply engaged in activities that seamlessly satisfy the rigorous four-part test of IRC Section 41.

However, maximizing the financial return on these innovative activities requires a highly bifurcated compliance strategy. Federally, taxpayers must meticulously document their scientific processes in real-time to protect massive supply and wage QREs from aggressive IRS scrutiny, closely heeding the evidentiary warnings of recent tax court jurisprudence like George v. Commissioner.

At the state level, businesses must recognize that the Arkansas R&D credit is not a passive, retroactive entitlement, but an active, pre-negotiated economic development partnership. Because the state aggressively incentivizes human capital—by rewarding high-paying wages and largely excluding physical supplies—and requires preemptive AEDC or ASTA certification, Fayetteville firms must integrate tax planning into their earliest operational, capital expenditure, and human resources strategies. By navigating these dual frameworks with precision, technology-driven enterprises in Fayetteville can significantly reduce their tax liabilities, accelerating both their corporate growth and the broader economic vitality of Northwest Arkansas for decades to come.

The information in this study is current as of the date of publication, and is provided for information purposes only. Although we do our absolute best in our attempts to avoid errors, we cannot guarantee that errors are not present in this study. Please contact a Swanson Reed member of staff, or seek independent legal advice to further understand how this information applies to your circumstances.

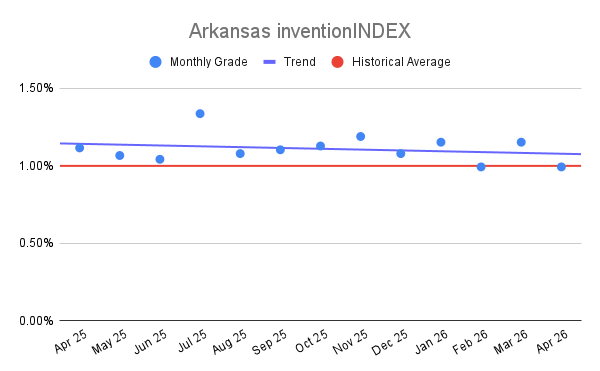

Arkansas inventionINDEX April 2026:<

Arkansas inventionINDEX April 2026:<