The United States Federal Research and Development Tax Credit Framework

The pursuit of technological advancement carries inherent financial risk, which the United States federal government seeks to mitigate through the Research and Development tax credit. Codified under Internal Revenue Code Section 41, this federal incentive was originally enacted in 1981 and subsequently made permanent by the Protecting Americans from Tax Hikes Act of 2015. The federal credit mechanism provides a dollar-for-dollar reduction in a taxpayer’s federal income tax liability based on the accumulation of qualified research expenses. To claim this credit, a taxpayer’s activities must strictly satisfy a stringent, statutorily defined framework commonly referred to as the Four-Part Test, which the Internal Revenue Service and the United States Tax Court utilize to separate routine business operations from true technological innovation.

The initial requirement within this framework is the Section 174 Test, which mandates that the expenditures must be treated as permitted research and experimental costs under Internal Revenue Code Section 174. Specifically, the research must be undertaken for the purpose of resolving technical uncertainty concerning the development or improvement of a business component. This uncertainty must relate directly to the component’s underlying capability, the methodology used to produce it, or the appropriateness of its fundamental design. If a company already possesses the knowledge to achieve a desired outcome using standard industry practices, the activity fails this initial threshold.

Following the establishment of technical uncertainty, the taxpayer must satisfy the Technological Information Test. This criterion demands that the process undertaken to eliminate the uncertainty must fundamentally rely upon the principles of the hard sciences. The Internal Revenue Code explicitly limits these permissible sciences to engineering, physical sciences, biological sciences, or computer science. Discoveries relying on social sciences, economics, humanities, or market research are statutorily excluded from the credit framework.

The third requirement is the Business Component Test, which dictates that the technological information discovered during the research must be intended for application in the creation of a new or improved business component. The Internal Revenue Code defines a business component broadly, encompassing a product, a process, computer software, a technique, a formula, or an invention that is either held for sale, lease, or license, or utilized internally by the taxpayer in their trade or business.

The final and historically most litigated requirement is the Process of Experimentation Test. The statute requires that substantially all of the research activities—historically interpreted as eighty percent or more of the project’s duration or cost—must constitute elements of a rigorous and systematic process of experimentation. This is not merely trial and error; it requires the formulation of a specific scientific hypothesis, the testing of alternatives through formal modeling, simulation, or systematic trial, the meticulous analysis of the resulting data, and the subsequent refinement of the hypothesis.

When these four tests are satisfied, taxpayers may aggregate their qualified research expenses. Under federal law, these expenses primarily consist of three categories. The first is taxable wages paid to employees who are physically performing the qualified research, as well as the wages of managers directly supervising the research and staff providing direct administrative or technical support to the researchers. The second category encompasses the cost of tangible supplies that are consumed or destroyed directly within the research process. Finally, taxpayers may claim a percentage—typically sixty-five percent—of contract research expenses paid to third-party entities performing qualified research on the taxpayer’s behalf, provided the research is conducted within the geographic boundaries of the United States. General overhead, administrative facility costs, and capital expenditures are strictly prohibited from being classified as qualified research expenses.

The Arkansas State Research and Development Tax Credit Landscape

While the federal credit provides a foundational baseline of tax relief, the State of Arkansas supplements this system with an aggressive, multi-tiered portfolio of its own research and development incentives. These state-level programs are primarily governed by the Consolidated Incentive Act of 2003, specifically Arkansas Code Annotated Section 15-4-2708, and are administered jointly by the Arkansas Department of Finance and Administration and the Arkansas Economic Development Commission. Unlike the federal credit, which is calculated based on expenditures reported directly on an annual tax return, the Arkansas credits are highly discretionary. They require proactive engagement, the submission of detailed project plans, and formal administrative approval from the Arkansas Economic Development Commission Executive Director before any credit can be legally claimed.

The Arkansas framework categorizes its research and development incentives into distinct programs based on the maturity of the firm and the specific nature of the research being conducted. The foundational tier is the In-House Research and Development program, which serves as a discretionary tax incentive for mature companies performing ongoing research within the state. To participate, the company must already be claiming the federal research credit for the same activities. The state credit is calculated as twenty percent of qualified research expenditures—which are strictly limited to taxable wages and fringe benefits, explicitly excluding supplies and equipment—that exceed a baseline expenditure established in the preceding year. This twenty percent credit applies over a five-year financial incentive agreement period, can offset up to one hundred percent of the company’s annual state income tax liability, and features a generous nine-year carryforward provision for unused credits.

To cultivate emerging technology sectors and direct capital toward specific areas of the economy, Arkansas offers a premium tier known as the Targeted Business and Strategic Value Research credit. Under this program, the state provides an elevated income tax credit equal to thirty-three percent of qualified research expenditures. To qualify, the research must be conducted in fields identified by the Arkansas Science and Technology Authority as having long-term economic or commercial value to the state. The Arkansas Economic Development Commission explicitly defines these strategic sectors as Advanced Materials and Manufacturing Systems, Agriculture, Food and Environmental Sciences, Biotechnology, Bioengineering and Life Sciences, Information Technology, Transportation Logistics, and Bio-Based Products.

The strategic value credits are highly regulated. For standard businesses, the thirty-three percent credit is capped at a maximum of fifty thousand dollars per taxpayer annually. However, for start-up technology enterprises that receive formal certification as a Targeted Business—which requires operating for less than five years, meeting specific high-wage thresholds, and demonstrating an equity investment of at least two hundred and fifty thousand dollars—the credit cap is effectively lifted, and the earned credits may be sold one time upon application and approval by the state. This transferability feature provides immediate capital injection for pre-revenue technology firms operating in the state.

The final tier of the state framework is the University-Based Research and Development program. This incentive is available to eligible businesses of any size that contract directly with one or more Arkansas colleges or universities to perform research that qualifies under federal guidelines. This program provides a thirty-three percent income tax credit for the qualified expenditures paid to the academic institution and can be used to complement a company’s internal research initiatives.

| Feature Parameter | Federal R&D Credit (IRC Section 41) | Arkansas In-House R&D Credit | Arkansas Strategic/Targeted R&D |

|---|---|---|---|

| Statutory Authority | Internal Revenue Code Section 41 | Arkansas Code Annotated § 15-4-2708(b) | Arkansas Code Annotated § 15-4-2708(c) |

| Base Credit Rate | Varies based on calculation method | 20% of incremental qualified wages | 33% of qualified expenditures |

| Qualifying Expense Types | Wages, Consumed Supplies, Contracted Research | Wages and Fringe Benefits Only | Wages (Transferable if Targeted) |

| Administrative Prerequisites | Must satisfy IRS Four-Part Test | Federal eligibility plus AEDC Approval | Federal eligibility plus AEDC and ASTA Approval |

| Tax Liability Offset | Subject to General Business Credit limits | 100% of state income tax liability | 100% of state income tax liability |

| Unused Credit Carryforward | 20 years | 9 years | 9 years |

The Historical and Economic Evolution of Jonesboro, Arkansas

To accurately assess the application of these complex tax laws, it is necessary to thoroughly analyze the specific industrial landscape of Jonesboro, Arkansas. Located in Craighead County in the northeastern quadrant of the state, Jonesboro stands as the fifth largest municipality in Arkansas and serves as the definitive economic and cultural hub of the region. The industrial history of the city is deeply tethered to its unique geographic positioning on the edge of the Mississippi Delta and the fertile agricultural lands of Crowley’s Ridge.

The modern economic trajectory of Jonesboro commenced in 1909 when local civic leaders successfully lobbied the Arkansas General Assembly to establish the First District State Agriculture School in the city. These early advocates argued that an institution dedicated to applied agricultural research would yield massive economic dividends for the surrounding rural population. Their predictions proved accurate, as this institution eventually evolved into Arkansas State University, which today supports an annualized enrollment of over twenty-one thousand students and generates a staggering two billion five hundred million dollar annual economic impact across the state.

Concurrently with the establishment of the agricultural school, local area farmers in 1910 began experimenting with the cultivation of rice in the fields outside the town. The unprecedented success of these localized agricultural trials transformed the entire regional economy. By 1921, the Arkansas Rice Growers Cooperative Association was formed, and in 1939, this cooperative expanded its industrial footprint by purchasing a major rice mill directly in Jonesboro. This entity, later known as Riceland Foods, continued to pioneer industry-first techniques, including the first implementation of combine harvesting, artificial drying, and bulk storage of rice in 1944. By the 1970s, Riceland had renovated its Jonesboro operations to create what was recognized as the largest rice mill in the world.

Because agricultural commodities are exceptionally heavy and expensive to transport in their raw state, mid-stream food processing facilities naturally clustered in Jonesboro to minimize supply chain friction. The massive agricultural base attracted a secondary wave of multinational consumer food brands, resulting in the establishment of major manufacturing plants by Frito-Lay, Conagra Brands, Unilever, and Nestle Prepared Foods.

By the mid-twentieth century, Jonesboro’s strategic location—proximate to major interstates, commercial rail lines, and the Mississippi River—made it an ideal logistical nexus. This geographic advantage spurred a tertiary industrial wave in heavy manufacturing and material handling. A pivotal moment occurred in 1962 when Tom Loberg relocated the Hytrol Conveyor Company from Wisconsin to Jonesboro with just twenty-six employees. The success of Hytrol initiated the region’s dominance in material handling systems, which was subsequently reinforced by the arrival of other manufacturers like Great Dane Trailers.

Today, Jonesboro’s economy is sustained by a highly diversified manufacturing sector. Economic data indicates that growth from existing industries accounts for approximately eighty percent of all new job creation within the city. As these legacy manufacturers and newly recruited targeted businesses face intense global pressures to increase production throughput, eliminate environmental waste, and comply with evolving federal regulations, they are heavily engaged in continuous engineering and biological research. This relentless pursuit of optimization triggers millions of dollars in potential federal and state tax credits, provided the companies can navigate the stringent legal precedents governing these programs.

Industry Case Study: The Food Processing and Agricultural Science Sector

The food processing industry represents the historical bedrock of the Jonesboro economy. The region’s agricultural dominance, initiated by Riceland Foods, has attracted a dense cluster of specialized food manufacturers. Beyond legacy institutions like Frito-Lay and Nestle, the sector continues to expand rapidly. In early 2026, InnovAsian Cuisine Enterprises, a subsidiary of Nichirei Foods, announced a capital contribution of one hundred and five million dollars to construct a one hundred and seventy-five thousand square foot state-of-the-art frozen food manufacturing facility in the Craighead Technology Park. This facility is designed to significantly increase production capacity for complex, high-growth multi-serve Asian entrees and will create approximately two hundred new jobs.

The formulation and mass production of consumer food products is a highly technical endeavor that routinely qualifies for federal and state tax incentives. Facilities in Jonesboro engage in qualified research when they experiment to achieve specific analytical requirements, such as precise pH balancing, exact brix levels, acid content manipulation, and targeted product viscosity. Scaling a delicate culinary recipe to a massive industrial continuous-flow oven requires intense engineering. Developing new batching sequences, testing automated mixing times, and optimizing thermal cooking temperatures to reduce biological waste and extend shelf life directly satisfy the federal Four-Part Test. Furthermore, under Arkansas law, these activities fall squarely within the Agriculture, Food, and Environmental Sciences strategic sector, potentially qualifying new market entrants for the thirty-three percent Targeted Business credit, while mature entities utilize the twenty percent in-house credit.

However, taxpayers in this sector must carefully heed the warnings established by recent federal tax court litigation. The ruling in Siemer Milling Company v. Commissioner of Internal Revenue serves as a critical cautionary precedent. Siemer Milling, an established agricultural processing company, claimed research credits for new product development, including wheat hybrids and flour heat treatments. The United States Tax Court completely disallowed the claims, stripping the company of hundreds of thousands of dollars in credits. The court determined that while the company asserted they engaged in experimentation, they failed the statutory Process of Experimentation test because they lacked adequate documentation demonstrating a methodical plan involving a series of trials to test a hypothesis, analyze data, and refine that hypothesis. The ruling reinforced that routine quality control and recipe tweaking do not constitute research without strict scientific rigor. Favorably, the court did explicitly rule that the development of a single business component can span more than one tax year, and employees do not need formal degrees in the hard sciences to perform qualified research.

A more recent 2026 decision in George v. Commissioner directly impacts the agricultural supply chains rooted in Jonesboro. In a case involving a fully integrated poultry producer processing millions of birds weekly, the court confirmed that active farming activities and the use of live animals as pilot models constitute qualified research. The court ruled that animals and experimental feed used during trials could be claimed as supply costs. However, the taxpayer lost a significant portion of their financial claim due to a discrepancy between their retrospective research study and actual daily operational logs, which showed the livestock receiving standard, rather than experimental, dosages.

For massive facilities like InnovAsian and Riceland Foods operating in Jonesboro, the legal mandate is clear. To successfully claim the federal and Arkansas state credits, these companies must ensure that their daily production logs, batch records, and quality assurance testing data contemporaneously align with any formal research narratives prepared for the Internal Revenue Service or the Arkansas Department of Finance and Administration.

Industry Case Study: Material Handling and Logistics Automation

If agriculture planted the seed of the local economy, heavy manufacturing built the modern infrastructure of Jonesboro. The anchor of this sector is the Hytrol Conveyor Company. Having relocated to the city in 1962, Hytrol capitalized on the region’s central location and dedicated workforce to grow into the largest conveyor manufacturer in North America. Operating out of a six hundred and sixty thousand square foot headquarters, Hytrol, alongside other heavy manufacturers like Great Dane Trailers, forms a dense logistics and material handling cluster. Driven by the exponential global increase in e-commerce, Hytrol established a dedicated forty-five thousand square foot Technology Center in Jonesboro to centralize its new innovations, including the development of sliding shoe sortation systems and its revolutionary EZLogic automation technology.

The design and manufacturing of technologically advanced automation systems are quintessential examples of qualified research. Designing complex tooling, evaluating alternative high-durability materials for payload distribution, and implementing robotics and intelligent material handling algorithms all require intensive mechanical and software engineering. The thousands of hours spent by engineering teams mitigating technical uncertainties surrounding maximum load capacities, motor thermal efficiency, and precision conveyor speeds seamlessly qualify for federal wage allocations. Under the Arkansas regulatory framework, Intelligent Material Handling and Automated Systems are explicitly codified under the Transportation Logistics strategic value area, allowing these manufacturers to aggressively leverage state-level tax offsets.

Despite the clear technological nature of the work, manufacturing companies face massive legal hurdles regarding the treatment of supplies used during research versus supplies used for ordinary commercial production. This distinction was litigated extensively in Union Carbide Corporation and Subsidiaries v. Commissioner of Internal Revenue. Union Carbide claimed research credits for supply costs incurred during one hundred and six separate process improvement projects conducted on active commercial production lines. The United States Tax Court ruled, and the Second Circuit Court of Appeals subsequently affirmed, that the supplies used in these process improvement experiments were not eligible as qualified research expenses. The courts determined that the raw materials constituted indirect research expenses because the company would have consumed those exact materials to produce commercial inventory regardless of whether the experiment took place.

For industrial manufacturers operating in the Craighead Technology Park, distinguishing between product research and process research is a critical compliance mandate. When a Jonesboro plant runs a test batch of aluminum or steel on a live commercial production line to improve an assembly process, the raw metal used in that test likely cannot be claimed as a supply expense under the Union Carbide precedent, as it remains an ordinary production cost. However, the wages of the mechanical engineers monitoring and calibrating that test do qualify. Conversely, if a completely separate, non-commercial prototype or pilot model is built in a dedicated environment, such as Hytrol’s Technology Center, the materials for that specific model may qualify, provided it is not subsequently sold to a customer.

Industry Case Study: Environmental Engineering and Air Pollution Control

Jonesboro is also home to highly specialized manufacturing subsets, most notably in the realm of environmental control technologies. Camfil Air Pollution Control, a subsidiary of a Swedish global group with manufacturing sites and research centers worldwide, has operated in Jonesboro for over two decades. The company manufactures premium industrial dust, fume, and mist collection systems, such as their flagship Gold Series X-Flo system, which handles toxic and combustible dusts to keep massive manufacturing and processing facilities safe. In early 2020, a devastating tornado completely destroyed their local manufacturing facility. Rather than abandon the region, the company demonstrated a profound commitment to Jonesboro by investing over thirty-seven million dollars into a new two hundred and ninety thousand square foot manufacturing and office facility, rebuilding a state-of-the-art operation from the ground up.

Environmental engineering is an inherently experimental field. Developing industrial filtration systems capable of capturing heavy, fine, and fibrous dust loads without severely impeding continuous airflow requires advanced mastery of fluid dynamics, materials science, and mechanical engineering. The rapid prototyping of new filter media, the aerodynamic testing of high-velocity intake valves, and the precise design of systems to mitigate catastrophic combustible dust explosions all face significant technical uncertainties. Under the Arkansas Economic Development Commission rules, environmental issues related to manufacturing and waste minimization are specifically codified as areas of Strategic Value under the Advanced Materials and Environmental Sciences sectors.

To maximize the federal tax credit, environmental engineering firms must navigate complex administrative burdens, specifically regarding labor tracking. The Internal Revenue Service Audit Techniques Guide emphasizes the substantially all rule, which historically requires a taxpayer to demonstrate that at least eighty percent of the activities for a given project are qualified in order to claim the full scope of the project’s costs. Specialized firms can uncover hundreds of thousands of dollars in qualified expenses by meticulously applying time-allocation analyses to employees who may not hold the formal title of researcher, but who nonetheless devote substantial hours to designing bespoke air filtration challenges for clients.

Firms rebuilding or establishing modern facilities in Jonesboro must leverage their capital expenditure and engineering payroll simultaneously. Under recent legislative changes to Internal Revenue Code Section 174, the amortization of research and experimental expenditures requires careful long-term tax planning, though certain immediate expensing options remain available for specific manufacturing processes. Furthermore, by coordinating directly with the Arkansas Department of Finance and Administration, such facilities must obtain their Certificates of Tax Credit prior to claiming the twenty percent or thirty-three percent state offsets on their corporate returns, ensuring full compliance with the Consolidated Incentive Act.

Industry Case Study: Consumer Packaged Goods and Chemical Formulation

The consumer packaged goods sector in Jonesboro is prominently represented by Nice-Pak Products, recognized as the global leader in the manufacturing of wet wipes. The company established a presence in the city in 2008 and 2009 with a modest workforce of thirty-five employees operating two production lines. Over the subsequent decade, the facility underwent perpetual expansion, transforming into a massive six hundred and seventy thousand square foot converting arena featuring ten high-speed production lines and employing nearly four hundred local associates. A significant catalyst for this sustained growth in Jonesboro was a major initiative by Walmart, headquartered in nearby Bentonville, Arkansas, which pledged to spend an additional two hundred and fifty billion dollars to procure American-made products. Because of its geographic proximity to Walmart’s corporate center, Jonesboro serves as an ideal manufacturing locus for private-label goods such as Equate and Parent’s Choice wipes.

The development and mass production of wet wipe products involve highly complex chemical engineering and materials science. Nice-Pak, having historically introduced industry firsts such as the first alcohol hospital swab and the first flushable wipe constructed from plant-based materials, engages in continuous formulation research. Evaluating alternative substrate materials for durability and flushability, formulating new liquid solutions including shampoos, hand sanitizers, and body washes that do not degrade the non-woven wipe fabric, and engineering the heavy converting machinery to fold and seal the products at high speeds without tearing all constitute qualified research activities.

The chemical and consumer goods formulation process relies on iterative trial and error, which introduces a primary compliance risk for multistate corporations operating within Jonesboro regarding strict geographic limitations. Under Internal Revenue Code Section 41, research must be conducted physically within the United States to qualify for the federal credit. Even more restrictive, under Arkansas Code Annotated Section 15-4-2708, the state in-house research credit is strictly limited to activities conducted exclusively within the physical borders of the State of Arkansas.

If a multinational consumer goods company designs a new chemical formulation at a corporate laboratory in New York, but subsequently tests the scale-up and manufacturing viability of that exact formulation on the converting lines in Jonesboro, the tax application is bifurcated. For the Arkansas state credit, only the wages and direct support activities performed by the employees physically located in the Jonesboro facility qualify for the state offset. Multistate corporations must therefore deploy highly sophisticated payroll allocation software to apportion qualified research expenses accurately by state jurisdiction. Failure to accurately geographically silo these expenses routinely leads the Arkansas Department of Finance and Administration’s Office of Revenue Legal Counsel to disallow the credits entirely during field audits.

| Allowable vs. Disallowable Qualified Research Expenses by Category |

|---|

| Allowable Federal and State QREs |

| Wages paid to engineers conducting fluid dynamics testing in a Jonesboro laboratory. |

| Time allocated by floor managers directly supervising a live trial-and-error manufacturing run. |

| Substrate materials destroyed during the testing of a non-commercial prototype filter. |

| Contract expenses paid to an Arkansas university to develop agricultural software algorithms. |

| Disallowable Federal and State QREs |

| Wages paid to corporate executives performing general management or market research. |

| Raw materials consumed during a process improvement test on a commercial product intended for final sale (per Union Carbide). |

| Capital expenditures utilized to purchase new, commercially available manufacturing equipment. |

| Wages for research conducted in a laboratory outside the boundaries of the State of Arkansas (Disallowed for State Credit only). |

Industry Case Study: University-Backed Bioinformatics and Information Technology

The formidable presence of Arkansas State University fundamentally transforms Jonesboro from a traditional heavy manufacturing hub into a modern, knowledge-based economy. Evolving from its 1909 agricultural origins, the university today acts as a primary incubator for technology startups through the A-State Innovation System, which actively assists emerging businesses with patent development, mechanical prototyping, and software engineering. Furthermore, the ongoing construction of the state’s first public College of Veterinary Medicine, slated for completion in the spring of 2026, alongside the established medical college on campus, creates a dense, highly educated ecosystem ripe for bioinformatics, software development, and advanced life sciences.

Software development, sophisticated database systems, and state-of-the-art applications for healthcare informatics and spatial agricultural technology are all explicitly targeted areas of Strategic Value under Arkansas law. Startups spinning out of the university’s innovation programs, or private corporations contracting with university faculty to develop proprietary logistics algorithms, predictive agricultural yield models, or medical sensor technologies, are conducting high-value research. If a Jonesboro business contracts directly with the university to perform this qualified research, the business becomes eligible for the unique thirty-three percent University-Based Research and Development income tax credit, which provides a massive subsidy for outsourced academic intelligence.

For software developers and technology startups operating in this sector, the judicial precedent established in Suder v. Commissioner of Internal Revenue provides the foundational legal benchmark. In this case, the chief executive officer and majority owner of a telecommunications software company claimed massive research credits for the development of new, proprietary telephone systems. The Internal Revenue Service challenged the eligibility of the software projects, attacked the methodology used to document employee time, and argued that the extraordinarily high wages claimed by the chief executive were unreasonable.

The United States Tax Court ruled overwhelmingly in favor of the taxpayer regarding the fundamental eligibility of the software projects. The court established that a business does not have to completely reinvent the wheel to qualify for the credit, provided there was genuine technical uncertainty regarding the specific method or appropriate design required to reach the technological goal. Furthermore, the court accepted the company’s methodology of estimating employee research time through the credible testimony of senior management, validating their internal record-keeping processes. However, the taxpayer suffered a catastrophic loss regarding executive compensation. The court determined that the chief executive’s wages were unreasonably high compared to standard industry compensation metrics for the actual hours devoted to technical research, resulting in a severe reduction of the allowable wage expenses.

For founders and startup entities operating out of the Jonesboro innovation ecosystem, the Suder decision dictates that while the Internal Revenue Service will accept reasonable allocations of time for software development based on credible testimony, founder compensation claimed as a qualified research expense must strictly align with reasonable market rates for technical labor, rather than reflecting executive privilege or profit distribution.

Tax Administration, Legal Counsel, and Audit Defense Strategies

The convergence of federal statutes and specific Arkansas state laws requires businesses operating in Jonesboro to implement meticulous, audit-ready administrative protocols to successfully claim and defend these tax credits. The Internal Revenue Service Audit Techniques Guide explicitly warns field examiners to intensely scrutinize aggressive strategies, particularly instances where taxpayers attempt to classify ordinary operational business expenses as qualified research, or manipulate historical base periods to artificially inflate their current-year credit calculations.

As definitively established in the Siemer Milling and George v. Commissioner precedents, both federal and state tax authorities demand rigorous, contemporaneous documentation. Taxpayers cannot rely solely on retrospective research studies generated by external tax consultants months or years after the activities conclude. To survive an audit, Jonesboro businesses must systematically maintain detailed project charters that outline specific technical uncertainties before a project begins, daily operational logs demonstrating trial and error, testing matrices, and robust time-tracking software that clearly delineates hours spent on conceptual design versus routine commercial fabrication.

Administratively, Arkansas is unique in that its highest-value credits—the thirty-three percent Strategic Value and Targeted Business credits—are completely discretionary and governed by the Arkansas Economic Development Commission rather than strictly operating through the Department of Finance and Administration. To secure these state-level advantages, a Jonesboro firm must navigate a rigid bureaucratic process. Before the research is concluded, the company must submit a highly detailed project plan to the state, identifying the precise intent of the research, the start and end dates of the project, and an accurate estimate of total anticipated costs.

Once approved, the taxpayer receives a formal Certificate of Tax Credit. When subsequently filing the Arkansas corporate income tax return through the state’s online portal, the taxpayer must physically attach this certificate to the return. Failure to append this specific document results in the immediate administrative disallowance of the credit. Furthermore, Arkansas law strictly prohibits overlapping incentives; a business earning targeted research credits is legally prohibited from simultaneously claiming job creation tax credits for the exact same payroll expenditures.

The Arkansas Department of Finance and Administration’s Office of Revenue Legal Counsel routinely scrutinizes these claims to ensure absolute compliance. While Arkansas has recently passed legislation to conform to several provisions of the federal Tax Cuts and Jobs Act regarding depreciation and research laws, state auditors remain highly aggressive. Businesses must remain vigilant, as the state will initiate immediate clawbacks—assessing both compounding interest and substantial financial penalties—if a taxpayer fails to produce the underlying scientific documentation and contemporaneous records during a formal field audit.

Final Thoughts

Jonesboro, Arkansas, represents a distinct microcosm of the broader American industrial evolution. From its foundational roots in localized rice farming and agricultural processing to its modern iteration as a highly sophisticated hub for advanced material handling, environmental engineering, consumer goods converting, and university-backed software development, the industries within the city are deeply engaged in high-level technological research.

By strategically aligning their daily operational activities with the stringent requirements of Internal Revenue Code Section 41 and Arkansas Code Annotated Section 15-4-2708, corporations operating in Jonesboro can capture substantial financial value to subsidize their growth. However, the legal precedents established by Siemer Milling, George v. Commissioner, Union Carbide, and Suder v. Commissioner explicitly mandate that technical innovation must be accompanied by equally rigorous administrative documentation. The successful monetization of these federal and state tax credits requires a symbiotic, ongoing effort between shop-floor engineers documenting their technical failures and financial executives securing the necessary discretionary approvals from state authorities.

The information in this study is current as of the date of publication, and is provided for information purposes only. Although we do our absolute best in our attempts to avoid errors, we cannot guarantee that errors are not present in this study. Please contact a Swanson Reed member of staff, or seek independent legal advice to further understand how this information applies to your circumstances.

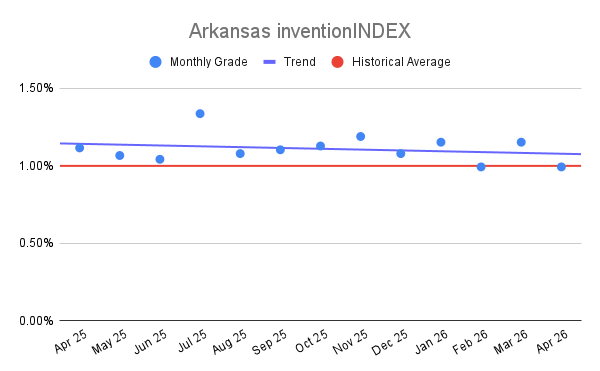

Arkansas inventionINDEX April 2026:<

Arkansas inventionINDEX April 2026:<