The Macroeconomic and Historical Industrial Context of Pine Bluff, Arkansas

To accurately assess the application and impact of advanced tax incentives within a specific municipality, one must first comprehensively understand the region’s historical economic development. The industrial topography of Pine Bluff, Arkansas, located in Jefferson County, is the result of over two centuries of geographic advantages, infrastructural investments, and strategic adaptations to national economic shifts. The city is a historical offspring of Arkansas Post, the first European foothold in the region, established in 1686. Pine Bluff itself was settled in 1819 by Joseph Bonne, a French-Quapaw interpreter who, displaced by severe flooding, established a settlement on a high bluff overlooking the south bank of the Arkansas River.

Throughout the nineteenth century, Pine Bluff’s proximity to fertile delta soils and navigable waterways catalyzed its growth as a premier cotton production center and a bustling river port. By 1890, this agricultural and commercial dominance had positioned Pine Bluff as the third-largest city in the state of Arkansas. However, the late nineteenth century introduced a profound economic pivot with the arrival of heavy rail infrastructure. The Little Rock, Mississippi and Texas railroad connected Pine Bluff to broader national markets in the 1880s, but the watershed moment occurred in 1894 when the Cotton Belt Railroad established its primary lines and extensive main engine maintenance shops in the city. This monumental industrial investment transformed Pine Bluff from a purely agrarian port into a highly industrialized cargo transport hub and a center for heavy mechanical engineering. The legacy of this era is preserved today in the Arkansas Railroad Museum, located within the original 1890s Cotton Belt Shops, which houses the last steam-powered locomotive constructed in Arkansas.

The early twentieth century brought severe economic turbulence, marked by catastrophic flooding, prolonged droughts, and the collapse of the cotton-based economy following World War I. Pine Bluff’s industrial salvation arrived with the onset of World War II. The federal government, recognizing the city’s strategic inland location and robust rail connections, authorized the construction of the Pine Bluff Arsenal in 1941. Originally a 5,000-acre tract that quickly expanded to over 13,000 acres, the Arsenal employed upwards of 10,000 workers during the war, producing magnesium and thermite incendiary munitions, as well as lethal chemical warfare agents. This influx of federal capital and the introduction of advanced chemical engineering permanently altered the region’s workforce, embedding technical manufacturing into the local culture.

Following the war, community leaders recognized the necessity of economic diversification. In the 1950s, the region capitalized on the surrounding abundant timberlands by attracting the heavy pulp and paper mill industry. The 1960s witnessed foresighted civic engineering projects, most notably the completion of the McClellan-Kerr Arkansas River Navigation System, which provided a reliable, year-round nine-foot channel for barge traffic. Concurrently, local leadership developed the Harbor Industrial District—a 372-acre park hydraulically filled to withstand flooding, featuring a 20-acre public terminal, heavy-lift gantry cranes, and designated Foreign Trade Zone status. This robust logistical infrastructure attracted a diverse array of major manufacturing companies, defense contractors, heavy electrical equipment producers, and large-scale food processing facilities to Jefferson County. Today, while facing modern urban challenges, Pine Bluff’s economy remains deeply anchored in manufacturing, health care, and the advanced agricultural research driven by the University of Arkansas at Pine Bluff (UAPB). It is within this diverse, heavy-industrial ecosystem that the intricate mechanisms of federal and state R&D tax credits become highly relevant and economically transformative.

The Federal Regulatory Framework for Research and Development Tax Credits

The federal Research and Development tax credit, formally titled the Credit for Increasing Research Activities, is codified under Section 41 of the Internal Revenue Code (IRC § 41). Originally introduced in 1981 to stimulate domestic innovation and prevent the offshoring of highly technical jobs, the credit was made a permanent fixture of the United States tax code by the Protecting Americans from Tax Hikes (PATH) Act of 2015. The credit is fundamentally an incremental incentive, generally allowing taxpayers to claim a percentage of the excess of their Qualified Research Expenses (QREs) for the current taxable year over a historically determined base amount.

The Threshold Requirement: Section 174 Permissibility

Before an expense can be considered for the Section 41 credit, it must first qualify as a research and experimental expenditure under IRC § 174. Section 174 broadly covers costs incurred in connection with a taxpayer’s trade or business that represent research and development costs in the experimental or laboratory sense. This means the expenditures must be for activities intended to discover information that would eliminate uncertainty concerning the development or improvement of a product. It is crucial to note that while all Section 41 expenditures must meet the Section 174 definition, not all Section 174 expenditures qualify for the Section 41 credit, as the latter imposes significantly more rigorous technological thresholds.

The Foundational Four-Part Test

The core of the federal R&D tax credit is the statutory “Four-Part Test” established by the Internal Revenue Service (IRS). To generate eligible QREs, the underlying activities must strictly and demonstrably satisfy all four of the following criteria simultaneously:

- The Permitted Purpose Requirement: The research activity must relate to the development of a new business component or the improvement of an existing business component. A “business component” is statutorily defined as a product, process, computer software, technique, formula, or invention that the taxpayer intends to hold for sale, lease, license, or use in their own trade or business. The improvement must relate to the component’s functionality, performance, reliability, or quality, rather than mere aesthetic or cosmetic modifications.

- The Technological in Nature Requirement: The research must fundamentally rely upon the principles of the “hard sciences.” The statute specifically enumerates the physical sciences (e.g., physics, chemistry, materials science), biological sciences, computer science, or engineering. Research relying on the social sciences, arts, humanities, economics, or market research is explicitly excluded from the definition of qualified research.

- The Elimination of Uncertainty Requirement: At the inception of the research project, the taxpayer must encounter definitive technological uncertainty. This uncertainty must relate to the taxpayer’s capability to develop or improve the business component, the optimal methodology required to achieve the development, or the appropriate and ultimate design of the component. If the solution to a problem is readily available within the taxpayer’s existing knowledge base or industry standard practices, the uncertainty requirement is not met.

- The Process of Experimentation Requirement: The taxpayer must engage in a systematic, evaluative process designed to overcome the identified technological uncertainty. This process must involve the identification of the uncertainty, the formulation of one or more hypotheses or alternatives, and the systematic testing and evaluation of those alternatives. Common methodologies include computational modeling, computer simulation, systemic trial and error, or iterative physical prototyping and destructive testing. The process must be capable of evaluating whether the alternatives achieve the desired result.

Statutory Exclusions and Specialized Tests

The Internal Revenue Code outlines several explicit exclusions designed to prevent the credit from subsidizing routine business operations or non-innovative expenditures. Research conducted after a product reaches the commercial production stage is excluded, as the fundamental design uncertainties should be resolved by that point. Furthermore, the adaptation of an existing business component to a particular customer’s requirement (routine engineering), the duplication of an existing component (reverse engineering), and routine quality control testing of materials are all disqualified activities.

A critical exclusion for defense contractors and specialized engineering firms in regions like Pine Bluff is the “Funded Research” exclusion under IRC § 41(d)(4)(H). If a taxpayer’s research is funded by a grant, contract, or another entity, the taxpayer cannot claim the credit unless they retain substantial rights to the research results and bear the economic risk of the development’s failure. If a contract guarantees payment regardless of the technical success of the project, the IRS views the third party, not the taxpayer, as bearing the risk, rendering the activities ineligible for the performing entity.

Additionally, the IRS applies heightened scrutiny to “Internal-Use Software” (IUS). For software developed primarily for the taxpayer’s internal administrative or operational functions, rather than for commercial sale or direct interaction with third parties, the taxpayer must satisfy an additional three-part “High Threshold of Innovation” test. This secondary test requires that the software be highly innovative, entail significant economic risk in its development, and not be commercially available for use by the taxpayer without substantial modifications.

Qualified Research Expenses (QREs)

If an activity satisfies the Four-Part Test and avoids statutory exclusions, the associated financial costs can be categorized as QREs. The federal code limits QREs to three primary categories:

- Wages: Taxable wages paid to employees who are directly engaged in the qualified research, as well as those providing direct supervision (first-line management) or direct support of the research.

- Supplies: The cost of tangible property used and consumed directly in the conduct of qualified research. This includes raw materials used to build prototypes or chemicals used in testing, but strictly excludes land, land improvements, and depreciable property.

- Contract Research Expenses: Payments made to third-party contractors performing qualified research on behalf of the taxpayer. Federally, these expenses are typically limited to 65% of the actual invoice amount, reflecting a statutory assumption of the contractor’s built-in profit margin and overhead.

Arkansas State R&D Tax Credit Legislation and Administrative Guidance

The State of Arkansas seeks to aggressively stimulate high-wage job creation and technological commercialization through a series of robust, state-specific R&D tax incentives. Governed primarily by Arkansas Code Annotated (ACA) § 26-51-1102 and the Consolidated Incentive Act of 2003 (Act 182), the state’s framework is intentionally tethered to the federal statutes to maintain technical consistency. Arkansas law explicitly mandates that for in-house research to qualify for any of the state-level discretionary credits, the underlying activities must first qualify for the federal R&D tax credit under IRC § 41. If an activity fails the federal Four-Part Test, it automatically fails the Arkansas state test.

Despite this technical conformity, the financial mechanics, administrative procedures, and expenditure limitations of the Arkansas credits differ significantly from the federal model. Arkansas segments its R&D incentives into distinct programs, each administered with joint oversight by the Arkansas Economic Development Commission (AEDC), the Arkansas Science and Technology Authority (ASTA), the Department of Higher Education, and the Department of Finance and Administration (DFA).

The Three Pillars of Arkansas R&D Tax Credits

| Arkansas R&D Tax Credit Program | Credit Rate & Calculation | Strategic Focus and Key Qualifications | Program Limitations & Utilization |

|---|---|---|---|

| In-House Research and Development | 20% of incremental QREs exceeding a historical base. | Designed for mature, established manufacturing and technology firms. The base year expenditure is set at zero for newly established research facilities, allowing 100% of eligible wages to qualify in the initial years. | Excludes costs for supplies, equipment, and buildings; focuses heavily on localized wage generation. Offsets up to 100% of state income tax liability with a 9-year carryforward. |

| In-House Research by a Targeted Business | 33% of total QREs (not incremental). | Exclusively available to companies operating within six state-defined strategic sectors (e.g., Bio-Based Products, Advanced Materials, Information Technology). Requires discretionary approval from the AEDC Executive Director. | Granted via a 5-year financial incentive agreement. Uniquely, credits earned by approved targeted businesses may be sold one time to generate immediate liquid capital. Offsets 100% of liability. |

| University-Based / Strategic Value Research | 33% of total QREs. | Designed to foster academic-industrial partnerships. Requires contracting research to an Arkansas college or university, or engaging in internal research defined as an “Area of Strategic Value” with long-term economic benefit to the state. | “Strategic Value” in-house credits are strictly capped at $50,000 per taxpayer annually. University-based collaborative credits support the state’s higher education research infrastructure. |

Targeted Business Sectors

The 33% Targeted Business credit represents one of the most lucrative economic development tools available in Arkansas, specifically because it allows for the monetization (sale) of the tax credit. However, access is highly restricted. The AEDC strictly defines “Targeted Businesses” as those operating within six specific, high-growth industrial sectors:

- Advanced Materials and Manufacturing Systems

- Agricultural, Food and Environmental Sciences

- Bio-Based Products

- Biotechnology, Bioengineering and Life Sciences

- Information Technology

- Transportation Logistics

Administrative Procedures and The Certificate of Tax Credit

Unlike the federal R&D credit, which a taxpayer calculates and claims retroactively on IRS Form 6765, the Arkansas state credits require proactive engagement with state agencies. Taxpayers cannot independently claim these credits on their state tax returns without prior authorization.

To qualify for the Arkansas credits, a business must submit a formal application and a detailed project plan to the AEDC and ASTA. This project plan must explicitly identify the intent of the research project, the specific technological uncertainties to be addressed, the start and end dates of the project, and a comprehensive estimate of the total project costs, specifically isolating the anticipated qualified wage expenditures.

Upon rigorous review and approval of the project plan, ASTA issues a formal “Certificate of Tax Credit”. Because the Arkansas DFA does not utilize a standalone, numbered form equivalent to the federal Form 6765, the physical attachment of this Certificate of Tax Credit to the taxpayer’s Arkansas corporate or individual income tax return serves as the mandatory primary documentation to execute the claim.

Five Unique Industry Case Studies in Pine Bluff, Arkansas

The historical convergence of riverways, transcontinental rail lines, massive military investment, and land-grant academic institutions in Pine Bluff has cultivated a uniquely diverse industrial ecosystem. The following five case studies detail specific industries deeply rooted in the economic fabric of Pine Bluff, explaining their historical development and outlining precisely how their ongoing technological activities meet the rigorous strictures of both U.S. Federal and Arkansas State R&D tax credit laws.

Case Study 1: Defense Contracting and Advanced Textile Manufacturing (The Pine Bluff Arsenal Ecosystem)

Development in Pine Bluff: The foundation of Pine Bluff’s advanced manufacturing capability was laid in 1941 with the rapid construction of the Pine Bluff Arsenal (PBA) in response to the outbreak of World War II. The facility originally mass-produced magnesium and thermite incendiary munitions before expanding into the highly dangerous production, loading, and storage of lethal chemical warfare agents. Throughout the Cold War, the Arsenal maintained a massive footprint in Jefferson County, pioneering complex chemical engineering and waste management, including the construction of a unique multi-furnace incinerator complex in 1978 for the demilitarization of obsolete chemical agents.

Following the final destruction of its chemical agent stockpile in 2010, the Arsenal pivoted its mission toward the sustainment of the Joint Warfighter through the production of less-than-lethal ammunition, tactical smoke devices, and biological defense equipment. Recognizing a critical gap in the domestic defense industrial base, the Secretary of the Army designated PBA as a Center for Industrial and Technical Excellence (CITE) for Chemical and Biological Defense Equipment in 2006, and subsequently awarded it a third CITE designation for Advanced Textile Manufacturing in 2022. This transition fostered a robust ecosystem of private defense contractors operating within the Arsenal’s footprint via Public-Private Partnerships (P3) and within the nearby Harbor Industrial District.

Specific R&D Activities: Private defense contractors in Pine Bluff are deeply engaged in engineering specialized chemical, biological, radiological, and nuclear (CBRN) protective garments. Research activities include the development of novel “neck dams”—garments impregnated with advanced carbon materials designed to bridge the gap between a protective mask and a chemical suit. Engineers must conduct rigorous research into new industrial sewing techniques to ensure seam impermeability against vaporized chemical agents, while concurrently formulating new pyrotechnic smoke compositions that generate massive optical obscuration without exposing friendly forces to toxic inhalation hazards.

U.S. Federal R&D Eligibility: The engineering of novel CBRN textiles and non-lethal munitions clearly satisfies the federal Four-Part Test. The Permitted Purpose is the creation of new protective garments and tactical smoke compounds. The research is Technological in Nature, relying heavily on materials science (carbon impregnation, textile tensile strength) and chemical engineering (pyrotechnic formulations). When a contractor attempts to bond a new carbon-lined fabric using a novel seam structure, they face profound Uncertainty regarding whether the seam will withstand mechanical stress in a combat environment without allowing microscopic chemical vapor penetration. The Process of Experimentation involves the iterative prototyping of garments, subjecting them to simulated stress tests, conducting vapor-penetration analysis in containment chambers, and systematically modifying the sewing techniques or fabric coatings based on empirical failure data.

Crucial Legal Context for Defense Contractors: Contractors in Pine Bluff must meticulously structure their government agreements to avoid the “Funded Research” exclusion codified in IRC § 41(d)(4)(H). As affirmed by the U.S. Court of Appeals for the Eighth Circuit (which holds appellate jurisdiction over Arkansas federal courts) in the recent 2024 decision Meyer, Borgman & Johnson, Inc. v. Commissioner, a taxpayer cannot claim the R&D credit if the government or a third party pays for the research regardless of its success. To qualify, Pine Bluff defense contractors must utilize fixed-price contracts rather than cost-plus-fixed-fee arrangements. Under a fixed-price framework, payment is contingent upon successfully engineering the product to exacting military specifications, meaning the contractor retains the ultimate economic risk of failure, thereby preserving their eligibility for the credit.

Arkansas State R&D Eligibility: If a defense contractor navigating the complex procurement environment in Pine Bluff qualifies federally, they are excellently positioned for Arkansas state credits. A mature contractor continuously iterating on textile designs could claim the 20% In-House Research credit on the wages paid to local chemical engineers, textile designers, and testing technicians. Furthermore, if the contractor formally classifies as an “Advanced Materials and Manufacturing Systems” company, they could petition the AEDC Executive Director for “Targeted Business” status. Approval would unlock a highly lucrative 33% credit on all qualified research wages for up to five years—a credit that could subsequently be sold to inject immediate liquid capital into their advanced manufacturing operations.

Case Study 2: Heavy Electrical Equipment and Transformer Manufacturing (Central Moloney)

Development in Pine Bluff: The heavy electrical manufacturing sector in Pine Bluff is synonymous with Central Moloney, Inc. (CMI). The company’s roots in Jefferson County trace back to 1949, when it was established as Larkin Lectro Products Company, a modest manufacturer of welding equipment and small electric transformers. Observing the massive post-war expansion and modernization of the North American electrical grid, the company strategically pivoted in 1952, dedicating itself solely to the manufacture of distribution transformers and rebranding as Central Transformer Corporation.

Pine Bluff provided the perfect logistical staging ground for this heavy industry. The robust rail infrastructure of the Cotton Belt line facilitated the efficient inbound transport of massive quantities of raw materials—specifically rolled steel, core iron, and copper wire—while allowing for the outbound distribution of heavy transformers to utility companies across the continent. In the mid-1980s, CMI revolutionized the global transformer industry by pioneering the introduction of thermoplastic primary and secondary bushings. This breakthrough utilizing advanced polymer technology shifted the industry standard away from fragile, heavy porcelain insulators, cementing Pine Bluff as a center for electrical component innovation. Today, CMI operates multiple facilities, employing over 500 individuals in the Pine Bluff area, and manufactures a vast array of pad-mounted transformers, pole-mounted transformers, and specialized high-voltage components.

Specific R&D Activities: As global power grids face unprecedented stress from peak summer cooling demands, aging infrastructure, and the variable input of renewable energy sources, transformer reliability is paramount. R&D activities within CMI’s Pine Bluff facilities focus on pushing the boundaries of material science to enhance dielectric strength and thermal resilience. Engineers conduct complex research formulating novel polymer casting, transfer molding, and pressure gelation techniques to manufacture specialized 600 AMP apparatus bushings and deadbreak switchgears. Furthermore, CMI engages in extensive environmental engineering, designing advanced “wildlife guards” using proprietary thermoplastic blends that must withstand extreme ultraviolet (UV) degradation, corrosive coastal salt spray, and continuous thermal cycling without compromising their insulating properties or becoming brittle.

U.S. Federal R&D Eligibility: The development of advanced thermoplastics and high-voltage transformer components relies fundamentally on polymer chemistry, electrical engineering, and mechanical engineering, definitively fulfilling the Technological in Nature requirement. When CMI engineers attempt to design a new 200 AMP load-break bushing well using a new thermoplastic resin blend, they face inherent Uncertainty regarding material shrinkage during the pressure gelation phase, the potential for internal void creation which could cause catastrophic dielectric failure, and the long-term thermal stability of the component under heavy electrical load. The Process of Experimentation involves creating prototype steel molds, varying the injection pressures, curing temperatures, and resin-to-catalyst ratios, and subsequently subjecting the first-article prototypes to high-voltage destructive testing to validate optimal performance characteristics.

IRS Audit Techniques Guide (ATG) Context: The IRS applies rigorous scrutiny to manufacturing-based R&D, frequently challenging taxpayers to prove that activities are developmental rather than routine quality control or standard production. Drawing parallels to the analysis in transformer manufacturing case law (such as the principles litigated in Intermountain Electronics), a manufacturer like CMI can successfully defend the inclusion of expenses for both nonproduction engineering staff (CAD designers, electrical engineers) and production floor staff (machinists, mold operators) who are directly engaged in the fabrication, modification, and physical testing of first-article prototypes prior to final commercial design approval. Thorough, contemporaneous documentation linking floor-level labor hours to specific iterative design failures is critical to surviving an IRS exam.

Arkansas State R&D Eligibility: For a legacy manufacturer possessing established infrastructure like Central Moloney, the Arkansas 20% In-House R&D credit serves as the primary and most consistent tax incentive vehicle. By meticulously isolating the specific W-2 wages of their Pine Bluff-based engineers, draftsmen, and floor technicians who are actively engaged in the prototyping and destructive testing phases of new transformer components, CMI can claim 20% of those eligible wages that exceed their historical rolling baseline. This credit directly and powerfully offsets their Arkansas corporate income tax liability, freeing capital for further facility expansion. Additionally, if CMI were to partner with a state university to utilize specialized power quality monitoring equipment to analyze transient electrical faults (similar to past initiatives utilizing AEDC technology transfer grants), the specific expenditures paid under that contract could qualify for the 33% University-Based Research credit.

Case Study 3: The Bio-Economy, Pulp, and Paperboard Packaging (Suzano)

Development in Pine Bluff: The vast, renewable timberlands of the Arkansas Delta and the immense water resources provided by the Arkansas River made Pine Bluff a logical and highly profitable location for the heavy paper manufacturing industry, which firmly established its presence in the 1950s. For decades, the massive mills operating in Jefferson County produced standard grades of pulp and paper, serving as a stable pillar of the regional economy and employing hundreds of local workers.

A monumental shift in the trajectory of this industry occurred in 2024 when Suzano, a Brazilian multinational corporation and the world’s largest producer of eucalyptus pulp, executed a $110 million acquisition of the massive Pactiv Evergreen paper mill in Pine Bluff (alongside a sister facility in North Carolina). This strategic acquisition integrated the Pine Bluff facility into Suzano’s global bio-economy strategy. The transition aims to leverage the mill’s existing infrastructure, which boasts a combined capacity of approximately 420,000 metric tonnes annually of integrated paperboard, to dominate the North American market for advanced liquid packaging board, cupstock, and sustainable, paper-based consumer goods.

Specific R&D Activities: Suzano’s operations in Pine Bluff extend far beyond traditional, repetitive paper production; they involve highly complex chemical engineering designed to adapt local North American raw materials to global proprietary manufacturing processes. Core R&D activities include the experimental integration of Suzano’s proprietary short-fiber eucalyptus fluff pulp (Eucafluff) with the long-fiber softwood pines native to Arkansas. Engineers must optimize the tensile strength, tear resistance, and liquid holdout of the resulting packaging boards. Furthermore, in response to global mandates for sustainable packaging, facility scientists conduct extensive trials on advanced extrusion coating processes, seeking to eliminate the industry’s historical reliance on fossil-fuel-based polyethylene plastics in liquid packaging. They are developing novel, bio-based barrier coatings that can maintain stringent food safety and liquid retention standards while ensuring the final consumer product remains fully repulpable and recyclable.

U.S. Federal R&D Eligibility: The IRS explicitly acknowledges the technical complexity of this sector through its dedicated Audit Techniques Guide (ATG) for the Pulp and Paper Industry. The ATG clarifies that process improvements, the development of new paper grades, and the integration of new chemical furnishes qualify as eligible research. For Suzano, the Permitted Purpose is the development of a new, highly sustainable liquid packaging board. The research relies heavily on chemical engineering, fluid dynamics, and biology, fulfilling the Technological in Nature requirement. Significant Uncertainty exists regarding whether a newly formulated, experimental bio-based polymer coating will adhere properly to the mixed-fiber paper matrix while the paper machine operates at massive industrial speeds and temperatures. The Process of Experimentation involves conducting pilot-scale paper machine runs, methodically varying the chemical furnish compositions, adjusting the thermal parameters of the extrusion coaters, and conducting rigorous Cobb testing (measuring water absorption rates) to validate the new barrier properties against control samples.

Arkansas State R&D Eligibility: Suzano’s transformative operations in Pine Bluff present a textbook justification for the application of the highly restricted Arkansas “Targeted Business” credit. One of the six explicitly designated targeted business sectors codified under Arkansas law is “Bio-Based Products”. By pivoting the legacy mill’s research focus toward replacing finite, petroleum-based packaging matrices with renewable, eucalyptus- and pine-based bio-materials, the facility is engaged in the exact type of strategic bio-economy research the state seeks to subsidize. With the discretionary approval of the AEDC Executive Director, the Pine Bluff facility could secure a five-year financial incentive agreement granting a massive 33% tax credit on all qualified in-house research wages. Because Targeted Business credits can be sold one time, this incentive provides immense, liquid capital relief during the facility’s complex and capital-intensive technological transition.

Case Study 4: Aquaculture, Fisheries Technology, and Academic Partnerships (UAPB and Commercial Farms)

Development in Pine Bluff: While traditional row-crop agriculture dominates much of the Arkansas Delta, the region is also a leading national force in aquaculture. Arkansas’s prominence in commercial fish farming is driven by its abundant surface water resources, a favorable climate for warm-water species, and the flat, clay-heavy soils of the Delta, which are geologically ideal for the construction of large earthen holding ponds. Pine Bluff serves as the intellectual and operational epicenter of this industry primarily because it is home to the University of Arkansas at Pine Bluff (UAPB), a land-grant institution that hosts the state’s only comprehensive, research-driven aquaculture and fisheries program.

The region has cultivated a massive commercial industry surrounding the farming of baitfish (golden shiners, fathead minnows), sportfish (largemouth bass, crappie), and channel catfish. This industry is inextricably linked to, and supported heavily by, UAPB’s extension programs, which provide critical assistance with fish health pathology, water quality analysis, and the engineering of farm-level biosecurity systems.

Specific R&D Activities: Commercial aquaculture farms in the Pine Bluff area operate in highly dynamic biological environments, requiring continuous research to combat emerging diseases, improve feed conversion rates, and optimize pond yields. Research activities include the engineering and implementation of proprietary water filtration and intensive split-pond aeration systems designed to manage and mitigate toxic algae blooms. Nutritional biologists experiment with the formulation of novel, non-genetically modified (non-GM) soy feed blends to optimize the bioenergetics of hybrid striped bass. Furthermore, veterinary researchers conduct trials utilizing prebiotic and probiotic feed additives to proactively enhance the immune response of baitfish against devastating specific pathogens, such as Flavobacterium columnare, Aeromonas hydrophila, and the CyHV-2 herpesvirus in goldfish.

U.S. Federal R&D Eligibility: Historically underutilized by the agricultural sector due to a lack of awareness, the federal R&D tax credit readily applies to modern, science-driven aquaculture. Formulating a new, highly efficient feed blend fundamentally requires the application of the biological sciences, fulfilling the Technological in Nature requirement. In one scenario, Uncertainty involves determining the precise, optimal ratio of alternative plant protein sources to vitamin A that will maximize largemouth bass growth without inducing liver toxicity or stunting development. To resolve this, biologists engage in a rigorous Process of Experimentation utilizing controlled mesocosm trials. Different experimental feed formulations are distributed across isolated testing tanks, and researchers systematically track feed conversion ratios, fish mortality rates, and water quality degradation over time. The wages paid to the farm’s marine biologists and technicians, along with the supplies consumed strictly during these controlled trials (such as the experimental feed ingredients and water testing reagents), constitute eligible QREs. Depreciable assets, such as the purchase of a new tractor or a permanent filtration pump, remain strictly excluded.

Arkansas State R&D Eligibility: The interconnected nature of the aquaculture industry in Pine Bluff makes it perfectly positioned to utilize the Arkansas “University-Based Research and Development” 33% tax credit. If a private commercial fish farm in Jefferson County formally contracts with the UAPB Department of Aquaculture and Fisheries to conduct targeted laboratory research—for example, a study to understand the molecular mode of CyHV-2 transmission from mother to offspring, or the development of improved calcein chemical marking techniques for fish tracking—the commercial farm can claim a powerful 33% state income tax credit on the exact expenditures paid to the university under that contract. Furthermore, because “Agricultural, Food and Environmental Sciences” is an explicit targeted business sector, an innovative aquaculture startup developing closed-loop aquaponics systems in Pine Bluff could apply for the 33% in-house targeted business credit for their internal research wages.

Case Study 5: Large-Scale Poultry Processing and Food Automation (Tyson Foods Ecosystem)

Development in Pine Bluff: While historical narratives of the Arkansas Delta heavily emphasize cotton, modern agriculture in Jefferson County is incredibly diverse, with poultry production serving as a dominant economic force. The presence of massive, highly industrialized food processing facilities has established Pine Bluff as a critical node in the national food supply chain. The most prominent example is Tyson Foods, which operates a massive poultry processing facility in the Jefferson Industrial Park, employing upwards of 1,500 people. The sustained growth of this specific industry in Pine Bluff relied heavily on the development of local highway infrastructure (specifically I-530 and US-65) for rapid refrigerated transport, access to the Harbor Industrial District’s utilities, and the availability of a steady regional agricultural workforce.

Specific R&D Activities: Modern, mega-scale poultry processing is no longer a manual endeavor; it requires relentless, high-tech innovation in food safety, robotic automation, and shelf-life extension to maintain razor-thin profit margins. R&D activities within these massive Pine Bluff facilities include the design, programming, and rigorous physical testing of robotic, computer-vision-guided automated deboning machinery. These systems are engineered to maximize meat yield from highly variable organic shapes while reducing ergonomic injuries among the human workforce. Further critical research involves developing new ultraviolet (UV) or proprietary chemical antimicrobial spray sanitation procedures for high-speed conveyor equipment to completely eliminate dangerous micro-organisms, such as Salmonella and Campylobacter, from processing surfaces. Additionally, food scientists experiment with novel modified atmosphere packaging (MAP) gas ratios (balancing oxygen, carbon dioxide, and nitrogen) to suppress microbial growth and extend the safe shelf life of fresh poultry products during cross-country transit.

U.S. Federal R&D Eligibility: The IRS provides specific, nuanced guidelines for the food and beverage industry. While routine nutritional testing, standard recipe adjustments, and daily quality assurance sampling are strictly excluded from the R&D credit, the engineering of entirely new processing equipment or advanced packaging techniques is highly eligible. Developing a computer-vision-guided robotic deboning process is fundamentally Technological in Nature, relying heavily on computer science (machine learning algorithms) and mechanical engineering. The primary Uncertainty centers on the software’s ability to accurately and rapidly identify complex bone structures in highly variable, non-uniform organic shapes moving at high speeds. The Process of Experimentation involves programming the initial vision algorithms, deploying the robotic arms on a test line with various poultry sizes, and iteratively adjusting the cutting paths and algorithmic tolerances based on empirical data regarding meat yield loss and the frequency of hazardous bone-fragment contamination.

Arkansas State R&D Eligibility: Large-scale poultry processors operating mature, established facilities in Pine Bluff are prime candidates for the Arkansas 20% In-House R&D credit. While the facility itself may be decades old, the continuous drive for automation generates eligible activities. By meticulously identifying the specialized industrial engineers, food scientists, and software developers working directly on the factory floor to design, implement, and physically test these automated systems, the company can claim a 20% credit on the portion of their wages that exceeds historical baselines. Because these massive processing facilities often operate on incredibly tight profit margins, utilizing this state credit to significantly offset Arkansas corporate income taxes allows for vital capital retention, which can be directly reinvested into further automation, ensuring the facility remains competitive against newer, out-of-state operations.

Government Tax Administration Guidance, Case Law, and Audit Defense Strategies

Claiming both federal and state R&D tax credits is not a passive exercise; it requires rigorous adherence to dense statutory guidance and a nuanced understanding of prevailing administrative case law. Both the IRS and the Arkansas DFA actively and aggressively audit these claims, necessitating that taxpayers in Pine Bluff maintain proactive, robust documentation strategies.

Federal Case Law and IRS Audit Guidelines

The IRS utilizes highly specialized Audit Techniques Guides (ATGs) to train field examiners on the unique R&D issues prevalent within specific industries, including the Aerospace and Defense industry, the Pharmaceutical industry, and the Pulp and Paper industry. These guides instruct examiners to look beyond the basic tax forms and demand access to the taxpayer’s chart of accounts, project accounting ledgers, and internal engineering reports. For manufacturers and defense contractors in Pine Bluff, the IRS focuses heavily on determining whether claimed expenses are true QREs and whether the underlying activities legitimately pass the four-part test, constantly searching for evidence of routine engineering, standard maintenance, or reverse engineering, all of which disqualify the claim.

Taxpayers must carefully track project accounting to definitively delineate experimental research costs from ordinary commercial production costs. As demonstrated in the recent 2024 Tax Court case Phoenix Design Group, Inc. v. Commissioner, the IRS aggressively challenges engineering and architectural design firms on the precise nature of their multi-stage design processes. In that case, the IRS disallowed the credits of an engineering firm because their standard, six-stage mechanical, electrical, plumbing, and fire protection (MEPF) design process did not demonstrate true, fundamental technical uncertainty or a robust, scientific process of experimentation, but rather represented the routine application of known engineering principles to standard building construction.

Furthermore, Pine Bluff contractors working with the Arsenal must heed the Eighth Circuit’s decision in Meyer, Borgman & Johnson, Inc. v. Commissioner (2024). The court denied R&D credits to a structural engineering firm, classifying their work as disqualified “funded research”. The court unequivocally established that if a taxpayer’s contract guarantees payment regardless of the ultimate success of the research, the taxpayer lacks the requisite financial risk, thereby disqualifying the activity from the credit entirely. Pine Bluff contractors must ensure their agreements are explicitly drafted to make payment contingent upon the verifiable success of the technological development, thereby retaining economic risk.

Arkansas DFA Rulings, Tax Appeals, and State Case Law

At the state level, the Arkansas Department of Finance and Administration (DFA) oversees the final processing and application of the R&D credits to corporate tax returns. The DFA’s Office of Revenue Legal Counsel provides formal legal opinions on complex tax policy and legislation. Taxpayers can formally rely on these opinions under the protection of Arkansas Gross Receipts Tax Rule GR-75, provided their specific factual circumstances perfectly align with the published opinion. If a taxpayer faces an audit and disputes the DFA’s application, denial, or calculation of their R&D credits, the matter is appealed to the independent Arkansas Tax Appeals Commission (TAC).

Arkansas courts have recently demonstrated a strong willingness to strictly interpret tax statutes based on their plain language, often ruling independently of broad, revenue-protective departmental policies, provided the taxpayer’s strategy aligns with the letter of the law. In the landmark 2024 decision Hudson v. Murphy Oil USA, Inc., the Arkansas Supreme Court ruled overwhelmingly in favor of a corporate taxpayer seeking a massive $4 million refund. Murphy Oil had amended its returns to allocate 100% of nonbusiness interest expenses (incurred from a $650 million debt used to fund a corporate spin-off) directly to Arkansas, its state of commercial domicile, rather than apportioning the deduction across the 24 states where it operated retail stations. The DFA attempted to deny the refund on “fairness” grounds, arguing that allocating the full deduction to Arkansas would force amendments in other states. The Supreme Court rejected the DFA’s argument, stating its sole job was to apply Arkansas law, regardless of the tax implications in other jurisdictions. While Murphy Oil dealt with interest allocation rather than R&D credits, it serves as a powerful signal to major corporations in Pine Bluff that strategic, aggressive tax planning utilizing Arkansas as a commercial domicile will be upheld by the state’s highest court when executed strictly within statutory bounds.

Documentation and Compliance Best Practices

To ensure airtight compliance and survive aggressive potential audits from either the IRS or the DFA, businesses in Pine Bluff must adopt the following operational strategies:

- Contemporaneous Documentation: Taxpayers must maintain real-time, highly detailed records of project plans, design iterations, engineering schematics, test results, and, crucially, failure logs. Attempting to recreate this data years later during an audit is highly risky. Furthermore, the Arkansas AEDC specifically requires that formal project plans detailing intent and wage estimates be submitted before or during the research phase to grant the lucrative Targeted Business credits.

- Granular Time Tracking: Companies must implement robust, project-based time tracking software for all engineering and support employees. Accurately calculating the wage component of QREs requires hard data on exactly how many hours an employee spent on a specific qualifying project, effectively eliminating the risk of IRS rejection due to pure estimation or post-hoc allocation.

- Rigorous Contract Review: Defense contractors and engineering firms must rigorously review all client and government contracts with specialized legal counsel to ensure economic risk is retained and payment is contingent upon success, completely avoiding the federal “funded research” trap.

- Proactive State Certification: Businesses must secure the formal “Certificate of Tax Credit” from the ASTA/AEDC in a timely manner. Because Arkansas state claims lack a standalone calculation form like the federal Form 6765, the physical attachment of this state-issued certificate to the DFA return is the absolute, mandatory mechanism for claiming the financial benefit. Failure to secure and attach this certificate renders the state claim invalid.

Final Thoughts

Pine Bluff, Arkansas, presents a fascinating and highly lucrative convergence of deep historical industrial infrastructure and modern, aggressive technological advancement. From the highly classified, advanced chemical defense manufacturing occurring within the perimeter of the Pine Bluff Arsenal, to the cutting-edge biological pathogen research occurring in local aquaculture mesocosms and the massive sustainable packaging engineering underway at the Suzano paper mill, the region’s diverse industries are deeply and continuously engaged in activities that meet the rigorous scientific standards of the IRC § 41 four-part test.

By strategically identifying these activities and actively pursuing both the federal R&D tax credit and the highly specialized Arkansas state incentives—whether monetizing the 20% In-House credit to shield factory wages, executing the 33% Targeted Business program to sell credits for immediate capital, or fostering University-Based partnerships with institutions like UAPB—businesses in Pine Bluff can legally offset massive state and federal tax liabilities. This critical capital retention is vital for continuous operational reinvestment, ensuring that the legacy industries of Jefferson County remain fiercely competitive, technologically advanced cornerstones of the American industrial landscape.

The information in this study is current as of the date of publication, and is provided for information purposes only. Although we do our absolute best in our attempts to avoid errors, we cannot guarantee that errors are not present in this study. Please contact a Swanson Reed member of staff, or seek independent legal advice to further understand how this information applies to your circumstances.

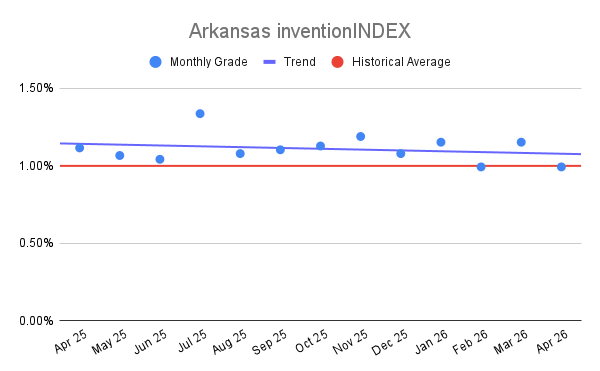

Arkansas inventionINDEX April 2026:<

Arkansas inventionINDEX April 2026:<