AI Answer Capsule

Overview: This comprehensive study analyzes the historical economic evolution and modern industrial landscape of Rogers, Arkansas, detailing specific applications of the United States Federal and Arkansas State Research and Development (R&D) Tax Credits. Rogers has transformed into a knowledge-based economy, focusing on retail logistics, aerospace, biotechnology, and autonomous supply chains. Through multiple case studies—ranging from autonomous vehicle delivery and poultry processing automation to specialized aerospace metallurgy and telemedicine—this study demonstrates how businesses can qualify for tax credits like the Arkansas Targeted Business Research and Development Credit. It emphasizes the critical importance of rigorous, contemporaneous documentation and strategic compliance to successfully claim these lucrative incentives.

The Economic Genesis and Industrial Evolution of Rogers, Arkansas

To fully comprehend the specific applications of Research and Development tax credits within Rogers, Arkansas, one must first examine the historical and economic foundations that transformed the region into a modern hub for innovation. Located in Benton County within the picturesque Ozark Mountains, the city of Rogers has undergone a profound economic evolution characterized by three distinct historical phases: the agricultural and transportation revolution, the retail and logistics boom, and the current era of advanced technological integration and automated supply chain dominance.

The foundational catalyst for the economic development of Rogers was the arrival of the St. Louis-San Francisco Railway, commonly referred to as the “Frisco,” in 1881. Prior to the introduction of the railroad, Northwest Arkansas was dominated almost entirely by subsistence farming. The logistical impossibility of transporting perishable goods over primitive dirt roads and mountainous paths isolated the region from broader national markets. The Frisco railroad precipitated a massive economic paradigm shift, enabling the region to transition rapidly into commercial agriculture. The railway provided affordable transportation and sparked an agricultural boom. By the early 1900s, Benton County had transformed its landscape to the point where it produced more apples than any other county in the United States, utilizing the railway to export millions of agricultural products to surrounding states. This initial agricultural infrastructure laid the vital groundwork for the subsequent rise of the poultry industry. In the 1930s and 1940s, pioneers like John Tyson began utilizing sophisticated, evolving logistics to transport poultry out of Northwest Arkansas to larger midwestern markets. This eventually led to the massive, vertically integrated poultry processing ecosystem that dominates the region today.

The second major economic catalyst occurred in 1962, when Sam Walton opened the very first Walmart store in Rogers, Arkansas. What began as a localized retail operation evolved over the subsequent decades into a multinational corporate behemoth, fundamentally altering the demographic, technological, and industrial landscape of Northwest Arkansas. Over the years, the massive gravitational pull of Walmart necessitated the relocation of thousands of suppliers, vendors, and logistics providers to the immediate region. Today, the Rogers and Bentonville corridor is recognized not merely as Walmart’s corporate hometown, but as the retail value-chain capital of the world. The proximity of major corporate anchors such as Walmart, J.B. Hunt Transport Services, and Tyson Foods has created a dense, highly interactive ecosystem where the retail buyer, the consumer packaged goods supplier, and the logistics infrastructure are co-located within a few miles of one another.

Presently, Rogers is experiencing rapid population and wage growth, transitioning firmly into a knowledge-based innovation economy. The median household income in Rogers grew to $82,993 by 2024, representing a twelve percent increase over the previous five years, and the local unemployment rate sits at a highly competitive 2.1 percent, well below the national average. Immigrant populations and an influx of young, highly educated professionals have driven forty-two percent of the region’s population growth, supplying the highly skilled technical workforce required for modern engineering and software development. This density of talent, supported by institutions like the University of Arkansas in nearby Fayetteville and the World Trade Center Arkansas, has transformed Rogers into a living laboratory for testing new technologies at operational scale. Due to this unique, highly concentrated corporate ecosystem, industries ranging from autonomous delivery logistics and retail analytics to aerospace metallurgy have developed aggressively in the region, conducting sophisticated research activities that align perfectly with the statutory intentions of United States federal and Arkansas state Research and Development tax credit incentives.

United States Federal Research and Development Tax Credit Legal Framework

The United States federal Research and Development tax credit, codified under Internal Revenue Code Section 41, is a general business credit designed to incentivize domestic enterprises to maintain technical jobs and invest heavily in technological development within the United States. The credit generally yields a dollar-for-dollar reduction in federal income tax liability equal to a specific percentage of the taxpayer’s qualified research expenses that exceed a statutorily defined base amount. The legislative intent is to encourage businesses of all sizes to undertake the financial risks associated with innovating new products, processes, and software architectures.

To qualify for the federal Research and Development tax credit, a taxpayer’s activities must satisfy a rigorous four-part test as outlined in Internal Revenue Code Section 41(d) and its corresponding Treasury Regulations. This test is applied at the business component level, meaning each individual project or product must independently satisfy all four criteria to be deemed qualified research.

The first requirement of the four-part test is the Permitted Purpose test, found under Section 41(d)(1)(B). The research must be intended to yield information that is useful in the development of a new or improved business component. The statute defines a “business component” broadly as any product, process, computer software, technique, formula, or invention that is held for sale, lease, license, or used by the taxpayer in their trade or business. This broad definition is critical because it allows manufacturers and software developers in Rogers to claim credits not only for the products they sell to consumers but also for the internal manufacturing processes and logistical systems they develop to improve their own operational efficiencies.

The second requirement is the Technological in Nature test, articulated in Section 41(d)(1)(B)(i). The activity performed must fundamentally rely upon the established principles of the hard sciences. The Internal Revenue Service explicitly lists engineering, computer science, biological sciences, and physics as acceptable foundations. Research that relies upon the soft sciences, such as psychology, economics, market research, or humanities, is explicitly excluded from qualification. Therefore, while a retail vendor in Rogers might conduct extensive market research to determine consumer preferences for a new product, only the actual engineering and food science activities required to physically create that product would qualify for the credit.

The third requirement is the Elimination of Uncertainty test, mandated by Section 41(d)(1)(A). At the very outset of the research project, the taxpayer must face technological uncertainty regarding either the capability to develop or improve the business component, the methodology required to develop or improve it, or the appropriate design of the business component. It is not necessary that the taxpayer succeeds in eliminating the uncertainty; the federal government explicitly rewards failed research, as failure is a natural byproduct of pushing technological boundaries. The documentation must clearly show that the engineers or developers did not possess the information necessary to achieve their desired outcome at the beginning of the project.

The final and most heavily scrutinized requirement is the Process of Experimentation test, found under Section 41(d)(1)(C). Substantially all of the activities, which is generally defined by the courts and regulations as eighty percent or more of the research effort, must constitute a systematic process of experimentation. This process involves a structured scientific method: identifying the specific technological uncertainty, identifying one or more alternative solutions intended to eliminate that uncertainty, and conducting a systematic process of evaluating those alternatives. This evaluation can take many forms, including digital modeling, mathematical simulation, systematic trial and error, or the creation and destructive testing of physical prototypes.

In scenarios where software is developed primarily for the taxpayer’s internal use, commonly referred to as Internal Use Software, the Internal Revenue Service imposes an additional, highly stringent three-part “high threshold of innovation” test under Proposed Treasury Regulation Section 1.41-4(c)(6). Internal Use Software is software that is not intended to be sold, leased, or licensed to third parties, but is instead used to run the taxpayer’s internal administrative or operational functions. To qualify, this software must be highly innovative, meaning it must result in a reduction of cost or improvement in speed that is substantial and economically significant. Furthermore, the development must involve significant economic risk, meaning the taxpayer commits substantial resources to the development and there is substantial uncertainty that those resources will be recovered in a reasonable period. Finally, the software must not be commercially available for use by the taxpayer without significant modification that would itself satisfy the requirements of qualified research.

When calculating the financial benefit, taxpayers must carefully analyze their funding mechanisms and third-party contracts. Under Treasury Regulation Section 1.41-2(e)(1), taxpayers may claim sixty-five percent of any expense paid or incurred to a third party, other than an employee of the taxpayer, for the performance of qualified research on their behalf. However, a critical caveat exists regarding financial risk and intellectual property rights. To claim contract research expenses, the taxpayer must bear the economic risk of the research’s failure. If the contractor is paid on a fixed-fee basis guaranteeing a successful result, the contractor bears the risk. The taxpayer must pay for the research regardless of its success, typically through time-and-materials contracts, to claim the credit. Furthermore, the taxpayer must retain substantial rights to the results of the research. Prepaid research expenditures are strictly ineligible for the credit until the actual services are performed by the contractor. Examining contract research expenses requires a meticulous review of the legal agreements to determine whether the financial risk and rights requirements have been legally met, and the Internal Revenue Service audit techniques guide recommends utilizing local counsel to interpret these agreements.

The federal tax courts continually shape the interpretation of Section 41 through ongoing litigation. A recent and highly relevant example is the United States Tax Court’s 2024 order in the case of Intermountain Electronics, Inc., No. 11019-19. In this dispute, the court evaluated whether the production expenses incurred in developing a physical “pilot model” met the definition of a process of experimentation under Section 41(d)(3)(A). Intermountain Electronics, a designer of custom electrical equipment, claimed research and development credits for the wages of both nonproduction engineers and production staff, as well as the physical supplies used in manufacturing pilot models of their specialized switchgears and controls. The court’s order provided vital insights into the “substantially all” requirement and affirmed that the costs associated with producing a functional pilot model, which is used to physically evaluate and resolve technological uncertainty before commercial production begins, can qualify as eligible expenses under Section 174 and Section 41. The case heavily emphasized the importance of maintaining contemporaneous documentation to support the assertion that production staff were genuinely engaged in a process of experimentation rather than standard, routine manufacturing.

The Internal Revenue Service has significantly increased its administrative scrutiny of Research and Development tax credit claims to combat perceived widespread abuse. Revisions to Form 6765, titled Credit for Increasing Research Activities, which become effective for the 2024 tax year, align with stringent IRS requirements for valid refund claims announced in 2021. Taxpayers are now required to provide robust, contemporaneous documentation at the time of filing. This documentation must explicitly detail all the specific business components researched during the taxable year, the exact technical uncertainties faced for each component, the specific alternatives evaluated to resolve those uncertainties, and the names and titles of the employees performing the qualified services. Taxpayers in Rogers must proactively implement processes to gather this granular engineering data throughout the year to minimize the administrative burden and ensure compliance with the new Form 6765 reporting requirements.

Arkansas State Research and Development Tax Credit Legal Framework

The State of Arkansas offers a highly lucrative, multi-tiered Research and Development tax credit framework designed explicitly to attract advanced manufacturing, aerospace, biotechnology, and information technology firms to the state. Administered collaboratively by the Arkansas Economic Development Commission, the Arkansas Department of Finance and Administration, and the Arkansas Science and Technology Authority, the state’s generous incentives fall under the umbrella of the Consolidated Incentive Act of 2003, primarily codified in Arkansas Code Annotated Section 15-4-2708 and Section 26-51-1102. The primary purpose of this consolidated legislation is to provide uniform definitions and streamlined administration of various economic incentives to further stimulate the transfer of science and technology into the commercial sector.

The Arkansas legislative framework is designed to prevent “double-dipping” by taxpayers. A business earning specific in-house Research and Development tax credits is strictly prohibited from earning job creation tax credits, such as the Advantage Arkansas income tax credit, on the exact same payroll expenditures. Furthermore, a taxpayer may not combine different in-house research state incentives for the same expenditure, though they may generally combine in-house incentives with university-based research incentives.

| Program Title | Credit Rate | Key Statutory Requirements and Mechanisms | Carryforward Period | Offset Limitation |

|---|---|---|---|---|

| In-House Research and Development (Mature Firms) | 20% | Discretionary incentive. Applies to incremental qualified research expenditures exceeding the previous year’s established baseline. Company must qualify for the federal program. Limits qualifying expenses to salaries only; supplies and equipment do not qualify. | 9 Years | 100% of annual income tax liability |

| Targeted Business Research and Development | 33% | Discretionary incentive for new, knowledge-based startups. Requires operations in an emerging technology sector. Must pay 150% of the lesser of state or county average wage and show a $250,000 equity investment. Credits may be sold one time upon approval. | 9 Years | 100% of annual income tax liability |

| Research and Development in Area of Strategic Value | 33% | Discretionary incentive for research having long-term economic value to the state. Must be approved by the ASTA Board of Directors. Maximum credit claimed cannot exceed $50,000 per tax year. | 9 Years | 100% of annual income tax liability |

| University-Based Research and Development | 33% | Applies to eligible businesses that contract with one or more Arkansas colleges or universities to perform qualified research. | 9 Years | 100% of annual income tax liability |

For technology startups, logistics analytics developers, and emerging engineering firms locating in Rogers, the Targeted Business Research and Development Credit represents the most powerful financial tool available in the state’s arsenal. This program offers a thirty-three percent income tax credit on qualified research and development expenditures incurred in-house for a period of up to five years from the signing of a financial incentive agreement. A highly unique and critical feature of the Targeted Business credit is its transferability; these credits may be sold one time, in whole or in part, upon application to and approval by the Arkansas Economic Development Commission. This mechanism provides immediate, non-dilutive liquidity to pre-revenue technology firms that do not yet possess the state income tax liability necessary to absorb the credits themselves.

To qualify as a “Targeted Business,” the company must meet extremely stringent economic and sector-specific thresholds. The business must show proof of an equity investment of at least $250,000. It must also pay wages that are at least one hundred and fifty percent of the lesser of the state average hourly wage or the county average hourly wage where the business is located. Furthermore, the business must operate explicitly within one of six specifically designated “Targeted Emerging Sectors” defined by the state legislature.

| Arkansas Targeted Emerging Sector | Applicable Sub-Disciplines and Relevant Industries |

|---|---|

| Advanced Materials & Manufacturing Systems | Electronics manufacturing, energy-efficient storage devices, photonics, nanotechnology, photovoltaics, and environmental issues related to materials and manufacturing. |

| Biotechnology, Bioengineering, and Life Sciences | Biopharmaceuticals, drug discovery, genetics, geriatrics, medical devices, neuroscience, oncology, protein structure, and sensor technology. |

| Bio-Based Products | Adhesives, automotive components, biodiesel, ethanol, methanol, polymers, and synthetic transportation fuels derived from non-traditional biomass. |

| Information Technology | Database systems, distributed systems, software development, wireless systems, and IT applications for bioinformatics or advanced healthcare. |

| Agriculture, Food, and Environmental Sciences | Agricultural medicine, aquaculture, distributed energy generation, forestry, nutrition, poultry processing, rice, spatial technology, toxicology, and waste minimization. |

| Transportation Logistics | Automated delivery systems, intelligent material handling, and transportation management and routing systems. |

Unlike the federal credit, which is generally calculated and claimed retroactively on a filed tax return, the Arkansas targeted and strategic credits are entirely discretionary and require proactive, prospective action by the taxpayer. The Arkansas Department of Finance and Administration requires that applicants undergo a rigorous application process to receive a Certificate of Tax Credit issued by the Arkansas Science and Technology Authority, which must then be physically attached to the state income tax return. The term of the financial incentive agreements is strictly limited to five years.

Arkansas administrative law places an exceptionally heavy burden of proof on the taxpayer regarding documentation and compliance. In the Arkansas Court of Appeals case Michael Morris, et al. v. Arkansas Department of Finance and Administration (2003), the appellate court upheld the Department of Finance and Administration’s assessments where the taxpayer’s documentation, specifically utilizing generalized audit summaries rather than granular source documents, failed to adequately substantiate the claimed tax credits. The court emphasized that the determination of the credibility of witnesses and evidence lies wholly within the province of the circuit judge acting as the trier of fact, underscoring the absolute necessity of maintaining meticulous, contemporaneous engineering and financial records.

More recently, the Arkansas Tax Appeals Commission, an independent tribunal created under the Independent Tax Appeals Commission Act to resolve tax disputes with the Department of Finance and Administration, has demonstrated a judicial willingness to look deeply at the functional economic substance of tax laws rather than merely their surface labels. For instance, in a highly consequential 2025 en banc decision (Docket Number 24-TAC-02810), the Commission ruled in favor of a taxpayer regarding the creditability of the Texas franchise tax against the Arkansas state individual income tax. The Department of Finance and Administration had denied the credit on the basis that the Texas franchise tax, often called a “margin tax,” was not a net income tax within the meaning of the Arkansas tax code. The Commission overruled the state, reasoning that the functional economic substance of the Texas tax was effectively a tax on net income, thus allowing the credit. This precedent is vital because it indicates that the Commission will rigorously evaluate the statutory mechanics and functional reality of credits. Therefore, it is absolutely vital for Rogers-based companies to ensure their engineering activities strictly and functionally meet the statutory definitions of a “process of experimentation” and “technological in nature” under both federal and state definitions, as mere superficial alignment will not survive an audit or a Commission appeal.

Case Study: Retail Logistics and Autonomous Supply Chain Software Development

The unprecedented density of the retail supply chain in Northwest Arkansas has created an unparalleled testing ground for advanced logistics technology. Because Walmart, its direct competitors, and over one thousand two hundred of its consumer packaged goods vendors are geographically concentrated within the Rogers and Bentonville corridor, software and technology developers face an immediate, real-world feedback cycle. Gatik, an innovative developer of autonomous vehicle logistics software, recognized this geographic advantage and partnered directly with Walmart to deploy Class 3 through Class 6 Autonomous Box Trucks on commercial delivery routes. In 2020, Gatik and Walmart received the Arkansas State Highway Commission’s first-ever approval to remove the human safety driver from their autonomous trucks following eighteen months of successful pilot operations. This culminated in a historic milestone in 2021, when Gatik and Walmart achieved the world’s first fully driverless commercial delivery route on the supply chain’s middle mile, utilizing multi-temperature autonomous box trucks to move customer orders between a fulfillment “dark store” and a Neighborhood Market in the Rogers-Bentonville area. This technological leap was driven directly by the economic mandate to increase the speed and responsiveness of e-commerce order fulfillment.

The development of autonomous middle-mile delivery systems heavily involves qualified research under Internal Revenue Code Section 41. Gatik faced immense technological uncertainties regarding spatial recognition in unstructured environments, minimizing latency in edge computing arrays, optimizing routing under highly variable weather conditions, and the complex integration of multi-temperature cargo control systems with the autonomous vehicle’s battery grid. To eliminate these uncertainties, the engineering teams engaged in a rigorous process of experimentation. They systematically tested complex sensor fusion algorithms, continuously combining and analyzing data streams from LiDAR arrays, radar, and optical cameras. During their pilot phase, they logged over seventy thousand operational miles in autonomous mode with a safety driver present. This massive dataset was used to iteratively train machine learning models, refining the artificial intelligence over countless software build cycles to eliminate safety and navigational uncertainties before finally removing the human driver. Under federal law, the wages of the software engineers, artificial intelligence developers, and robotics technicians working on these algorithms in Rogers qualify as qualified research expenses. Furthermore, the costs of prototype hardware, such as cloud computing instances for artificial intelligence training and the specialized server nodes installed in the test vehicles, used directly in the experimentation process are eligible supply expenses.

Under Arkansas state tax law, these autonomous engineering operations fit perfectly within the designated Targeted Business sectors of either Information Technology or Transportation Logistics, specifically the sub-disciplines of software development and automated delivery systems. Given that autonomous trucking software fundamentally revolutionizes intelligent material handling and transportation management systems, Gatik’s local development operations would be highly eligible for the thirty-three percent Targeted Business Research and Development Tax Credit. Assuming the company meets the statutory $250,000 equity investment requirement and pays its local technical staff one hundred and fifty percent of the Benton County average wage, it could offset its Arkansas state tax liability entirely. Alternatively, if operating at a loss, the company could apply to the Arkansas Economic Development Commission to sell the credits to generate immediate operational capital.

Case Study: Poultry Processing Automation and Machine Vision Integration

Following the agricultural pivot facilitated by the Frisco railroad at the turn of the century, Northwest Arkansas gradually evolved into a global epicenter for commercial poultry production. Tyson Foods, headquartered in nearby Springdale and operating massive logistics and processing facilities in Rogers, grew from a local transport hauler in the 1930s into a Fortune 500 multinational corporation. Today, the modern poultry industry faces severe, systemic labor shortages. Meat processing environments are inherently cold, humid, and require repetitive, physically demanding labor, resulting in employee turnover rates that can reach fifty percent within the first ninety days of employment. To combat this existential threat to production capacity, Tyson Foods established the Tyson Manufacturing Automation Center, investing over two hundred and fifteen million dollars in automation and robotics to completely modernize food production processes. Concurrently, local university researchers, funded by United States Department of Agriculture grants, are pioneering the Center for Scalable and Intelligent Automation in Poultry Processing to develop robotic deboning mechanisms and pathogen-detecting artificial intelligence.

The automation of raw biological material processing is fraught with technical complexity because, unlike standardized automotive parts or electronics, no two chicken carcasses are dimensionally identical. Mechanical engineers and software developers face massive technological uncertainty in programming robotic end-effectors to cleanly debone irregular organic shapes without sacrificing meat yield, and in developing computer vision models capable of accurately counting and classifying varying cuts of meat on a high-speed, continuously moving conveyor belt. To overcome these hurdles, researchers engage in a fascinating process of experimentation. Engineers utilize digital twin modeling and virtual reality headsets; human operators use virtual reality controllers to remotely guide robotic arms through the deboning process, creating an massive database of complex human movements. This proprietary dataset is then used to train artificial intelligence algorithms to execute autonomous deboning protocols. Additional experimental activities include deploying complex computer vision neural networks to identify inventory codes on irregularly shaped packages and utilizing inexpensive thermal imaging cameras to dynamically detect foreign materials in packaged meat.

For federal tax purposes, the salaries paid to the robotics engineers, data scientists, and food technologists conducting these trials qualify as research expenses. Furthermore, the materials and supplies used to construct the “pilot models” of the robotic deboning stations—which are physically built, tested, and iterated upon within the Tyson Manufacturing Automation Center facility—qualify as eligible supply costs under the judicial precedent strongly affirmed by the Intermountain Electronics Tax Court order.

At the state level, this specific type of research and development distinctly qualifies under the Agriculture, Food, and Environmental Sciences targeted sector, explicitly covering poultry and advanced food manufacturing. For a mature, established corporate entity like Tyson Foods, these activities would fall under the twenty percent In-House Research and Development Tax Credit, calculated on the incremental qualified research salaries over the established baseline. Additionally, if these corporate entities contract with researchers at the University of Arkansas to conduct pathogen detection or robotics research, they can claim the thirty-three percent University-Based Research and Development tax credit for those specific, localized contract expenditures, further cementing the bond between corporate engineering and local academic institutions.

Case Study: Aerospace Tube Fabrication and Specialized Metallurgy

While the retail logistics and poultry sectors dominate the public economic identity of Rogers, a highly sophisticated advanced manufacturing sector has developed aggressively in parallel. A premier example of this is Mundo-Tech, a specialized tube fabrication company founded in Rogers in 1985. The massive presence of federal defense contractors in Arkansas, such as Lockheed Martin’s sprawling missile facility in Camden and the newly established Foreign Military Sales Pilot Training Center at the Ebbing Air National Guard Base in Fort Smith, has created a robust, localized supply chain demand for advanced aerospace components. Mundo-Tech specializes in advanced tube fabrication solutions, producing mission-critical hydraulic, oxygen, and fuel lines for high-stress defense and space applications, including components for the F-35 Lightning II fighter jet, Blue Origin spacecraft, and Virgin Galactic vehicles. To meet rising global supply chain demands, Mundo-Tech recently doubled its physical footprint in Rogers, investing heavily in additional computerized numerical control (CNC) technology and manufacturing space.

Aerospace manufacturing requires absolute adherence to extreme physical tolerances and strict compliance with International Traffic in Arms Regulations, pushing manufacturers to constantly innovate their metallurgical and fabrication processes. The engineering teams face continuous technological uncertainty when tasked with developing new methods for bending lightweight, high-strength alloys, such as titanium or specialized aerospace carbon composites, without compromising the structural integrity of the tube or creating microscopic stress fractures. To resolve these uncertainties, Mundo-Tech’s engineers must engage in extensive Computer-Aided Design, Computer-Aided Manufacturing, and Finite Element Analysis simulations to predict material behavior under extreme pressure. Following digital simulation, they systematically machine and test new physical jigs, dies, fixtures, and FX3D tooling to optimize the manufacturing process for newly designed, complex aerospace geometries. They must then conduct rigorous, physical design validation testing—often destructive in nature—to satisfy federal regulatory fatigue and stress requirements.

Under the federal tax code, the wages of the aerospace engineers designing the tooling, the costs of constructing the prototype fixtures, and the consumption of highly expensive raw materials, such as aerospace-grade titanium, that are destroyed or scrapped during destructive stress testing are fully claimable as qualified research expenses.

Under Arkansas law, Mundo-Tech’s specialized metallurgical operations align perfectly with the Advanced Materials and Manufacturing Systems sector under the Targeted Business regulations. Furthermore, because their research contributes directly to the state’s strategic goal of growing the aerospace and defense industry—an industry that already exports nearly one billion dollars in aircraft goods annually from Arkansas—such innovative activities could be evaluated under the Research and Development in Area of Strategic Value program. This specific program, requiring approval from the Board of Directors of the Arkansas Science and Technology Authority, allows for a thirty-three percent credit and up to $50,000 annually in high-value tax offsets for strategic innovation.

Case Study: Virtual Healthcare Architectures and Telemedicine Infrastructure

The delivery of healthcare in Northwest Arkansas has had to evolve aggressively to match the region’s explosive demographic and population growth. Mercy Hospital Northwest Arkansas, originating from a humble community-run hospital built in 1950, has undergone continuous modernization, recently executing a multi-year, $500 million investment plan to expand healthcare infrastructure across the region, which includes a newly completed $141 million, seven-story hospital tower in Rogers. Beyond massive investments in physical infrastructure, the geographic reality of Arkansas—featuring densely populated business corridors immediately surrounded by expansive, medically underserved rural areas—has driven a critical need for advanced virtual health capabilities. Accelerated by the necessities of the COVID-19 pandemic and bolstered by a $2.2 million grant from the Federal Communications Commission and half a million dollars in United States Department of Agriculture grants, Mercy Virtual has aggressively developed telehealth software architectures to bring hospitalist, stroke, and specialized neurology services directly to remote rural populations across the state.

The development of a secure, zero-latency telemedicine infrastructure involves significant software and systems engineering, far beyond the installation of standard commercial software. Integrating disparate Electronic Health Record systems with live, high-definition video streaming platforms, connecting biometric Internet of Things diagnostic devices at a remote patient’s bedside, and processing real-time predictive analytics creates massive architectural and data-security uncertainties for software engineers. To create a functional telemedicine ecosystem, developers engage in a continuous process of experimentation. Software engineers iteratively develop and stress-test custom Application Programming Interface bridges to allow different hospital mainframes to communicate. They must evaluate and optimize varying video data-compression algorithms to ensure medical-grade diagnostic video feeds remain stable over notoriously poor rural broadband connections, while simultaneously encrypting the entire data stream to comply with strict federal HIPAA privacy regulations.

Because this telemedicine software platform is used internally by Mercy’s physicians and administrators to deliver patient care, rather than being packaged and sold commercially to the public, it is classified as Internal Use Software and must pass the Internal Revenue Service’s “high threshold of innovation” test. By drastically reducing the need for bedside exposure during infectious outbreaks and creating a fundamentally new technological capability for remote intensive care unit monitoring, this software development yields substantial and economically significant improvements in the speed of care delivery and reduction of patient transport costs, thoroughly satisfying the high threshold requirements.

Within the Arkansas state incentive framework, the development of sophisticated telehealth software directly supports the Biotechnology, Bioengineering, and Life Sciences targeted sector, which explicitly includes IT applications for advanced healthcare. Arkansas law allows mature healthcare networks conducting this type of proprietary, in-house software engineering to claim the twenty percent In-House Research and Development Tax Credit on the incremental qualified research salaries over their base period, effectively subsidizing the payroll of the highly skilled software development and cybersecurity teams working within the Rogers hospital facilities.

Case Study: Third-Party Distribution and Custom Warehouse Management Systems

Because the world’s largest retail buyer is headquartered in the immediate vicinity, Northwest Arkansas has organically become a premier incubator for distribution, supply chain analytics, and logistics software startups. With over one thousand two hundred supplier and vendor offices located in the Rogers and Bentonville area to service Walmart and Sam’s Club, third-party logistics providers and specialized retail software agencies—such as High Impact Analytics, Fieldbook Studio, and SupplyPike—have scaled rapidly. These technology firms specialize in designing complex omnichannel software solutions, seamlessly integrating inventory management, supply chain predictive forecasting, and warehouse robotics automation to meet the incredibly strict compliance windows and routing guides demanded by modern big-box retailers.

Software development within the distribution and logistics sector is frequently misunderstood as routine information technology implementation and is often overlooked for Research and Development credits, yet it involves highly eligible, complex engineering work. Developing a bespoke Warehouse Management System or customizing an Enterprise Resource Planning architecture to handle multi-location, global inventory storage tracking requires overcoming severe algorithmic uncertainties. Software engineers face uncertainty regarding the optimal database architecture required to process millions of stock-keeping unit transactions in real-time without system latency, or the correct mathematical structure for a machine learning model designed to predict erratic seasonal inventory fluctuations.

To build these systems, developers engage in highly structured agile software development sprints. They test different warehouse slotting strategies and model massive facility layouts using digital twins before ever moving physical product. They iterate on advanced computer vision algorithms designed to automatically scan, recognize, and translate complex international import and export documentation. Furthermore, they must systematically resolve complex integration failures when writing the code that links cloud-based Enterprise Resource Planning solutions with the physical, automated storage and retrieval systems operating on the warehouse floor.

The wages of the full-stack software developers, database architects, and logistics engineers directly engaged in writing the code and testing these software modules qualify as federal research expenses. Additionally, if local Rogers technology firms utilize outside, United States-based cloud-architecture consultants to assist in the complex database development, sixty-five percent of contractor fees qualify as contract research expenses under the federal tax code, provided the Rogers firm retains the financial risk and intellectual property rights to the resulting code.

Under the Arkansas Consolidated Incentive Act, this high-level software and systems engineering falls squarely within the Information Technology sector, specifically database systems and software development, as well as the Transportation Logistics sector, specifically automated systems and transportation management systems. Technology startups emerging from local venture studios in Bentonville and Rogers could aggressively utilize the thirty-three percent Targeted Business Research and Development Credit to offset their operational burn rates. If these software entities operate at a loss in their early years of development, the highly unique state provision allowing the one-time sale of these tax credits provides a vital financial mechanism for realizing the monetary benefit immediately, thereby injecting critical capital back into the startup to fuel further hiring and software innovation in Rogers.

Final Thoughts

While the statutory mechanisms of both the United States Internal Revenue Code and the Arkansas Consolidated Incentive Act are highly favorable to the engineering, software, and manufacturing industries located in Rogers, actually realizing the financial benefits of these tax credits requires rigorous, proactive strategic compliance and meticulous recordkeeping.

The Internal Revenue Service is aggressively enforcing documentation standards nationwide. To comply with the new Form 6765 regulations, companies in Rogers must pivot immediately from retrospective, year-end Research and Development studies to continuous, contemporaneous tracking of engineering hours and activities. For instance, a manufacturer like Mundo-Tech cannot simply claim the gross cost of all titanium purchased in a year; it must document the specific aerospace tube fabrication project, the exact iterations of computerized tooling tested, the dates of the destructive tests, and link the specific engineering hours of named employees to that distinct technological uncertainty. The documentation must clearly construct the narrative of experimentation required by Section 41.

Furthermore, the Arkansas application prerequisite demands proactive legal and financial strategy. Unlike the federal credit, which is claimed retroactively on an amended or current tax return, the most lucrative Arkansas credits—specifically the Targeted Business and Strategic Value programs—are discretionary and require action before the research begins. A technology company in Rogers must apply to the Arkansas Economic Development Commission and the Arkansas Science and Technology Authority during the inception of the research project. The application must include a detailed project plan explicitly outlining the technological intent, estimated expenditures, and project timeline. Relying on experienced legal and tax counsel is paramount; as demonstrated by the rigorous procedures of the Arkansas Tax Appeals Commission and the strict rulings of the Department of Finance and Administration, the state applies an exacting interpretation of statutory definitions. Companies must secure the Certificate of Tax Credit and explicitly, functionally tie their research activities to the statutorily defined emerging technology sectors to survive future audits.

Rogers, Arkansas, has evolved from an isolated railroad agricultural hub into a highly sophisticated epicenter for retail logistics, aerospace manufacturing, and applied technological research. The presence of global anchor institutions—Walmart, Tyson Foods, J.B. Hunt, and Mercy Health—has created a compounding network effect, drawing specialized engineering and technical talent to the region. The United States federal Research and Development tax credit and the Arkansas Consolidated Incentive Act provide a highly synergistic financial framework that explicitly rewards this industrial evolution. By strategically aligning their engineering and software operations with these exact tax frameworks, businesses operating in Rogers can significantly reduce their effective tax liabilities, fueling ongoing innovation and firmly cementing Northwest Arkansas’ position as a premier global technological hub.

The information in this study is current as of the date of publication, and is provided for information purposes only. Although we do our absolute best in our attempts to avoid errors, we cannot guarantee that errors are not present in this study. Please contact a Swanson Reed member of staff, or seek independent legal advice to further understand how this information applies to your circumstances.

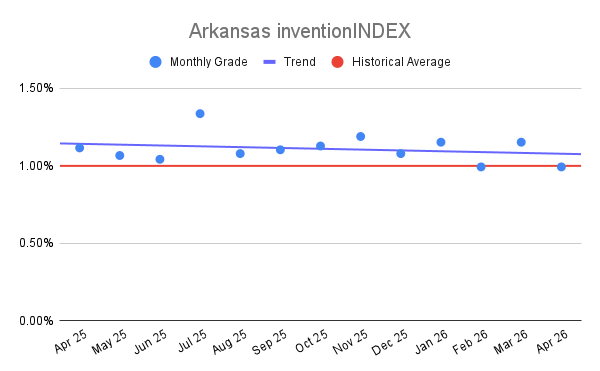

Arkansas inventionINDEX April 2026:<

Arkansas inventionINDEX April 2026:<