What are the R&D tax credit requirements in Shawnee, Kansas? To qualify for the Research and Development (R&D) tax credit in Shawnee, Kansas, businesses must satisfy the IRS four-part test (Permitted Purpose, Technological in Nature, Elimination of Uncertainty, and Process of Experimentation) and incur Qualified Research Expenses (QREs) within the state. Kansas offers a robust 10% credit on excess QREs, which is fully transferable for entities lacking state tax liability, further amplified by federal IRC Section 41 and 174A benefits.

This study provides an exhaustive, multi-layered analysis of the United States federal and Kansas state Research and Development (R&D) tax credit frameworks, focusing strictly on statutory requirements, recent legislative overhauls, and relevant judicial precedents. Through five detailed industry case studies, this document illustrates how specific sectors developed in Shawnee, Kansas, and how their localized technological initiatives satisfy the rigorous eligibility standards of both federal and state tax laws.

Industrial Topography and Industry Case Studies in Shawnee, Kansas

To fully comprehend the strategic application of R&D tax credits in Shawnee, Kansas, one must first examine the historical and macroeconomic forces that transformed this municipality into a highly specialized industrial and technological nexus. Located in western Johnson County and encompassing forty-two square miles, Shawnee currently operates as the third fastest-growing city in the State of Kansas. However, its modern economic ecosystem is the result of centuries of infrastructural evolution.

The region’s earliest economic foundations were rooted in its geographical positioning. Originally part of the Shawnee Indian reservation, the territory was opened to widespread settlement following the passage of the Kansas-Nebraska Act of 1854. During this period, the area became a crucial transit point, serving the Fort Leavenworth-Fort Scott Military Road, as well as critical branches of the Oregon, California, and Santa Fe Trails. From its brief stint as the county seat of Johnson County under the name “Gum Springs” to its strategic location near the Campbellton stop on the Kansas City, Ft. Scott & Gulf Railroad in 1870, Shawnee’s early survival depended entirely on logistics, transportation, and agricultural support.

By the 1920s, Shawnee had evolved into a premier agricultural service town, gaining a regional reputation as a leading fruit and vegetable producer. The intense focus of Shawnee’s truck farmers on agricultural yield, soil health, and efficient market logistics allowed the local economy to weather the Great Depression far more successfully than other Midwestern regions. This foundational agrarian science laid the conceptual groundwork for the food processing, animal health, and agricultural technology sectors that currently anchor the region’s economy. Following World War II, the transition from a rural agricultural economy to a suburban industrial powerhouse was dramatically accelerated by the introduction of interurban rail lines, specifically the Hocker Grove Line, and the paving of Kansas State Highway 10. These infrastructural arteries directly connected the skilled labor pool of Shawnee to the heavily industrialized center of Kansas City, Missouri, fostering an environment ripe for advanced manufacturing and professional services.

Today, the culmination of this historical development is a hyper-concentrated ecosystem of innovation. The city leverages immediate access to major interstate highways, including I-35, I-435, and K-7, which serve as the primary east-west retail and transportation lifelines in western Johnson County. More importantly, Shawnee benefits profoundly from localized public investments, most notably the Johnson County Education Research Triangle (JCERT), which utilizes a dedicated sales tax to fund world-class clinical research, animal health, and advanced engineering institutes within the immediate vicinity. It is within this rich historical and infrastructural context that the following five industry case studies operate, conducting qualified research that meets the strict parameters of United States and Kansas state tax law.

Case Study: Animal Health Contract Development and Manufacturing Organizations (CDMOs)

Industry Profile: Argenta (Shawnee Manufacturing Facility)

The presence of advanced pharmaceutical and biological manufacturing in Shawnee is a direct result of the region’s deliberate integration into the Kansas City Animal Health Corridor. Formalized in 2004, this corridor represents a highly targeted economic development initiative stretching from Manhattan, Kansas, to Columbia, Missouri. This geographic zone houses over three hundred animal health companies and accounts for an estimated sixty to sixty-seven percent of global animal health product revenue. Global pharmaceutical companies strategically locate facilities in Shawnee to gain immediate proximity to the graduates and research output of Kansas State University’s veterinary and food science programs, as well as the University of Kansas’s clinical research centers. Argenta, a global Contract Development and Manufacturing Organization (CDMO) dedicated exclusively to the animal health sector, exemplifies this localized industrial strategy. The company expanded its United States operations by acquiring a world-class manufacturing site in Shawnee, specifically targeting the facility’s market-leading capabilities in sterile fill-finish technology, non-sterile liquids, pastes, and oral solid dose manufacturing.

From a tax administration perspective, Contract Development and Manufacturing Organizations face highly specific challenges in claiming the federal and state R&D tax credits, primarily revolving around the “funded research exclusion” outlined in Internal Revenue Code (IRC) Section 41(d)(4)(H). When a CDMO like Argenta enters into a contract with a pharmaceutical sponsor to scale up a biological molecule from a laboratory environment to commercial manufacturing, the IRS requires the CDMO to establish that their contracts place the absolute economic risk of development failure on the CDMO itself, rather than the sponsor. Furthermore, the CDMO must retain substantial rights to the manufacturing processes and engineering techniques they develop during the engagement. Legal precedents, particularly the determinations in the Populous and Smith v. Commissioner tax court cases, provide critical guidance here. If the manufacturing contract operates on a firm-fixed-price basis where payment is entirely contingent upon the successful delivery of viable, FDA-compliant sterile batches, the courts generally recognize that the economic risk requirement is satisfied. If the scale-up fails and the batch must be destroyed, the CDMO absorbs the financial loss, thereby legitimizing the research expenses for the tax credit.

The specific engineering and biological activities conducted within the Shawnee facility must comprehensively satisfy the IRS four-part test to be deemed qualified research. The permitted purpose of these activities is typically the development of a new aseptic manufacturing process designed to increase pharmaceutical throughput or ensure absolute sterility for a novel veterinary therapeutic. This work is fundamentally technological in nature, relying extensively on the hard sciences of microbiology, organic chemistry, and chemical engineering to analyze active pharmaceutical ingredient (API) degradation, fluid dynamics, and microbial contamination parameters. At the onset of scaling up a new veterinary biological drug, substantial technical uncertainty exists regarding the optimal temperature controls, the specific blending times required for uniform API dispersion across a massive batch, and the exact lyophilization (freeze-drying) parameters needed to maintain the drug’s long-term efficacy. To eliminate this uncertainty, the CDMO’s engineering teams must engage in a rigorous process of experimentation. They hypothesize varying pressure and temperature gradients, test multiple batch sizes in a sandbox environment, conduct complex stability and purity assays utilizing High-Performance Liquid Chromatography (HPLC), and iteratively adjust the mechanical filling line variables until strict pharmacopeial standards are successfully achieved. The wages of the chemical engineers, microbiologists, and quality assurance personnel directly involved in these validation runs, alongside the vast quantities of raw materials and chemical reagents consumed during the testing phases, constitute Qualified Research Expenses (QREs). These expenses are fully eligible for both the United States federal R&D tax credit and the ten percent Kansas state credit under K.S.A. §79-32,182b.

Case Study: Freight Logistics and Supply Chain Technology

Industry Profile: Tallgrass Freight Co.

The logistical dominance of Shawnee is a modern manifestation of its historical origins as a critical waypoint for nineteenth-century pioneer trails. As the region matured, good city planning and economic development practices deliberately concentrated commercial and industrial distribution along major traffic arteries to protect residential enclaves. Today, immediate access to Interstate 35, Interstate 435, and Highway K-7 provides logistics and transportation industries with unparalleled access to the North American market. Utilizing this network, goods shipped by truck from Shawnee can reach twenty-five percent of the United States population within a single day, and ninety percent within two days. This geographical advantage has attracted massive distribution centers for companies such as Amazon, FedEx Ground, and Target. Tallgrass Freight Co., an independent freight agency network headquartered in Shawnee, exemplifies the rapid evolution of this industry from traditional manual freight brokerage to highly advanced, technology-driven supply chain management. Dissatisfied with the severe limitations of off-the-shelf software, Tallgrass Freight invested heavily in the development of a proprietary Customer Relationship Management (CRM) and algorithmic logistics routing platform, transforming themselves into a technology company that brokers freight.

The development of proprietary software for supply chain management subjects the taxpayer to the highly scrutinized Internal Use Software (IUS) regulations under United States tax administration guidance. Because the software developed by Tallgrass Freight is primarily intended for the taxpayer’s internal use to broker freight and manage complex agent relationships, rather than being developed for external commercial sale, the IRS mandates that the development activities must meet the standard four-part test plus an additional “high threshold of innovation” test. To satisfy this elevated threshold, the software must be highly innovative, resulting in a substantial and measurable reduction in cost or a profound improvement in operational speed. Furthermore, the development must involve significant economic risk, where substantial financial resources are committed with a high degree of technical uncertainty regarding the project’s ultimate success, and the software cannot be commercially available without modifications that would themselves satisfy the IUS requirements.

The permitted purpose of Tallgrass Freight’s software engineering was the creation of a novel algorithmic routing and CRM architecture designed to exponentially improve the speed, functionality, and reliability of complex freight matching. This undertaking was inherently technological, relying on the hard principles of computer science, specifically advanced database architecture, algorithmic optimization, and complex Application Programming Interface (API) integration. Significant technical uncertainty existed at the project’s inception regarding whether a newly constructed architectural framework could simultaneously process millions of disparate, real-time data points encompassing truck geographic locations, fluctuating load requirements, and federal compliance data without suffering from catastrophic system latency. Further uncertainty surrounded the programmatic methodologies required to bridge legacy, fragmented transportation networks with a unified, cloud-based infrastructure. To overcome these hurdles, the software engineers engaged in systematic agile development methodologies. They hypothesized multiple database structures, evaluating the performance metrics of relational versus non-relational databases under heavy simulated loads. They coded alternative caching algorithms specifically designed to reduce data retrieval latency, conducted rigorous beta testing across isolated network nodes, and repeatedly refactored the core code base when stress testing revealed systemic computational bottlenecks. The cloud hosting costs representing computer time-sharing, along with the W-2 wages of the software developers, systems architects, and quality assurance testers involved in the coding and beta testing phases, constitute highly defensible QREs for both the federal credit and the Kansas state R&D credit.

| Representative Logistics and Transportation Operations in Shawnee/Johnson County |

Core Industry Focus |

Workforce Scale |

| FedEx Ground Package System, Inc. |

Regional Hub Distribution |

1,450 |

| JC Penney Catalog Logistics |

E-commerce Distribution |

700 |

| OptumRx |

Pharmaceutical Distribution |

1,200 |

| YRC Worldwide |

Trucking and Freight Logistics |

1,000 |

| Tallgrass Freight Co. |

Freight Technology and Brokerage |

Agent Network |

Case Study: Consumer Healthcare and Over-the-Counter Therapeutics

Industry Profile: B.F. Ascher & Company, Inc.

Following the conclusion of World War II, the rapid suburbanization of western Johnson County created a profound demand for light manufacturing facilities, pharmaceutical distribution centers, and corporate headquarters that were distinct from the dense, heavy industrial zones historically located in the Kansas City West Bottoms. Founded in 1949 and headquartered in Shawnee Mission, B.F. Ascher & Company leveraged this expanding commercial infrastructure and the region’s highly stable workforce to develop into a prominent national provider of consumer and professional healthcare products. The company operates a significant portfolio of over-the-counter (OTC) pharmaceutical products, most notably the MOBISYL transdermal pain relief cream and the AYR saline family of sinus and allergy relief products.

The formulation, testing, and continuous improvement of over-the-counter pharmaceuticals require relentless scientific iteration to meet evolving consumer demands, improve clinical efficacy, and ensure absolute compliance with stringent Food and Drug Administration (FDA) OTC monographs. The permitted purpose of the research activities conducted by a company like B.F. Ascher involves the development of new variations of saline delivery systems, such as transitioning from traditional aerosolized sprays to highly viscous gels, or improving the molecular absorption rates of transdermal pain relief creams. These activities are deeply rooted in the hard sciences of analytical chemistry, pharmacology, and material sciences.

When a pharmaceutical manufacturer attempts to eliminate a specific, outdated preservative from a legacy formula to create a modern, “clean-label” or natural product line, profound technical uncertainty is introduced into the manufacturing process. It is uncertain whether the newly proposed chemical formulation will maintain its required multi-year shelf life, phase stability, and specific viscosity when subjected to various extreme thermal conditions during global shipping and warehousing. To methodically eliminate this uncertainty, the company’s formulation chemists must execute a highly documented process of experimentation. They formulate multiple prototype batches using varying, precise ratios of novel excipients, active pharmaceutical ingredients, and chemical surfactants. These prototypes are then subjected to rigorous accelerated environmental testing within specialized high-heat and high-humidity environmental chambers. The resulting degradation data is chemically analyzed using mass spectrometry and chromatography to determine precisely which formulation structure successfully mitigates the breakdown of the active ingredients over time. This continuous feedback loop leads to iterative adjustments in the chemical compounding process until a stable, effective product is finalized.

Historically, the massive expenditures associated with formulation chemistry, prototype batch destruction, and long-term stability testing were highly scrutinized. Under the restrictive regime of the Tax Cuts and Jobs Act (TCJA), these domestic research and experimental expenditures were required to be capitalized and amortized over five years, severely impacting the working capital of pharmaceutical manufacturers. However, under the restorative provisions of the One Big Beautiful Bill Act (OBBBA) enacted in 2025, these critical chemical engineering costs can once again be fully expensed under IRC Section 174A in the year they are incurred, providing an immediate and substantial federal cash benefit. Simultaneously, the wages of the chemists and the cost of the destroyed raw chemical supplies generate robust Kansas state tax credits, which, under K.S.A. §79-32,182b, can be carried forward indefinitely if the company’s current state tax liability is fully saturated by other localized incentives.

Case Study: Unified Communications and Enterprise Audiovisual Integration

Industry Profile: SKC Communications (Merged with AVI-SPL)

The high concentration of major corporate headquarters in the immediate vicinity of Overland Park, Lenexa, and Shawnee—including multinational entities such as Garmin, numerous financial services firms, and major telecommunications providers—created an immense, localized demand for sophisticated, high-tier corporate communications infrastructure. SKC Communications, founded in Shawnee in 1986, capitalized directly on this regional demand by designing, building, and managing next-generation multimedia environments and advanced IP telephony systems. The deep pool of electrical and software engineering talent cultivated within Johnson County facilitated SKC’s rapid growth into an industry-leading integrator holding the prestigious Avixa Audiovisual Provider of Excellence (APEx) certification. This trajectory of technological excellence eventually culminated in its strategic acquisition by AVI-SPL, the world’s leading digital enablement solutions provider, further expanding the Shawnee hub’s capabilities in global unified communications and collaboration (UCC) strategies.

Within the realm of tax law, systems integration frequently occupies a complex space between routine installation engineering and qualified research and development. To legally qualify for the federal and state tax credits, the integrating entity must overcome unique, project-specific technological hurdles that cannot be solved through the standard application of vendor manuals or routine industry practices. The permitted purpose of SKC’s research activities involves the architectural design and complex engineering of highly customized, interoperable audiovisual and unified communications networks tailored for massive enterprise environments. This work is fundamentally technological, relying heavily on the advanced principles of electrical engineering, computer science, and acoustic physics.

Profound technical uncertainty routinely arises when engineering teams are tasked with integrating highly disparate legacy hardware systems, such as older Avaya telephony PBX networks, with modern, cloud-based video infrastructure like Microsoft Teams or Zoom. The engineering uncertainties encompass highly complex issues regarding digital signal processing, catastrophic network packet loss, acoustic feedback loops within unconventional architectural spaces, and the integration of highly secure, encrypted network protocols. To resolve these engineering challenges, the integration team must construct a physical or virtual sandbox environment to methodically test alternative architectural schematics. The engineers hypothesize specific network configurations, simulate extraordinarily heavy bandwidth loads to proactively test for latency or network jitter, engineer custom APIs to force disparate, proprietary hardware components to communicate seamlessly, and systematically adjust electrical impedance and digital acoustic routing to completely eliminate echo and feedback in complex structural environments.

Contractually, the eligibility of SKC’s complex integration activities is heavily governed by the legal precedents established in Smith v. Commissioner and the highly relevant Populous decision regarding architectural and engineering fixed-price contracts. Because the firm is engaged in the highly complex engineering design of bespoke IT systems, provided their enterprise contracts are structured such that the firm strictly bears the financial cost of system redesign and labor overruns if the delivered system fails to meet the client’s rigorous interoperability specifications, the firm successfully retains the required economic risk. Therefore, the extensive labor hours of the systems engineers, network architects, and custom programmers clearly qualify for both the United States federal and the Kansas state R&D tax credits.

Case Study: Agricultural Technology and Sustainable Food Processing

Industry Profile: Seaboard Foods

Shawnee’s early history as a prominent truck farming community in the 1920s established a regional cultural and economic identity deeply tied to agricultural yield, soil health, and complex food systems. As the Kansas City metropolitan area expanded outwards, the region systematically transitioned from local, small-scale farming to housing the administrative, logistical, and technological nerve centers of global agricultural conglomerates. Seaboard Corporation, a diverse multinational agribusiness with historical roots tracing back to 1918 as a humble flour broker in Atchison, Kansas, maintains its corporate headquarters in Merriam, which shares the immediate borders, workforce, and economic infrastructure of the Shawnee Mission area. Seaboard Foods, a primary subsidiary, manages a uniquely integrated and connected food system involving advanced genetic breeding, highly engineered feeding operations, and state-of-the-art pork processing. Their strategic location in the Shawnee region leverages immediate logistical access to the Midwest grain belt for feed procurement, while also capitalizing on proximity to the world-class food science, microbiology, and veterinary research centers located at Kansas State University.

Modern, large-scale pork production is an intensely scientific and data-driven endeavor. Seaboard Foods heavily invests capital in cutting-edge swine genetics and complex environmental engineering, specifically focusing on the construction of covered anaerobic digester lagoons and sophisticated biomethane upgrading facilities designed to capture and refine Renewable Natural Gas (RNG). The permitted purpose of these research and development activities encompasses the design of improved anaerobic digestion processes to efficiently convert massive volumes of swine waste into ultra-low carbon intensity (CI) renewable energy, as well as the continuous improvement of the genetic lineage of commercial swine to enhance natural disease resistance and meat quality. This research is deeply embedded in the hard biological sciences, encompassing genetics and microbiology, alongside advanced chemical and environmental engineering principles.

In the development of bespoke biomethane upgrading facilities, profound technical uncertainty exists regarding the optimal bacterial compositions, precise temperature controls, and specific hydraulic retention times required to maximize the methane yield from highly variable, location-specific waste profiles. Simultaneously, within the genetics division, uncertainty constantly exists regarding precisely which complex cross-breeding lineages will yield the optimal feed-to-weight conversion ratios while simultaneously maintaining the lean muscle mass demanded by the global market. The process of experimentation for RNG development requires environmental engineers to test multiple pilot digester configurations. They systematically manipulate critical input variables such as moisture content, internal pH levels, and co-digestion materials, carefully recording the corresponding outputs of total biogas volume and ultimate methane purity. They utilize sophisticated software to mathematically model the complex kinetics of the anaerobic process and iteratively refine the physical infrastructure, such as mechanical agitation systems, based on empirical, real-world data.

The financial expenditures associated with these highly technical activities—ranging from the salaries of the geneticists, environmental engineers, and data scientists, to the vast supplies consumed during the pilot digester testing phases—are prime candidates for the federal R&D tax credit. Furthermore, the State of Kansas, which explicitly recognizes that forty-two percent of its entire state economy is inextricably tied to agriculture, heavily incentivizes these exact types of technological advancements through the robust ten percent state R&D credit, strategically ensuring that advanced food system engineering remains firmly anchored within state borders rather than relocating to competing agricultural states.

Detailed Analysis: The United States Federal R&D Tax Credit Framework

The United States federal Research and Development tax credit, statutorily codified under Internal Revenue Code Section 41, remains the premier financial incentive designed to stimulate domestic technological innovation, foster high-wage job creation, and drive overall macroeconomic growth. The legislative intent underlying the credit is to deliberately encourage taxpayers to incur the massive financial risks inherently associated with the development of new or improved products, manufacturing processes, computer software, techniques, formulas, or inventions. However, eligibility for this lucrative credit is not granted merely for the generalized pursuit of scientific knowledge or routine operational improvements; it requires rigorous, highly documented adherence to statutory guidelines, defined primarily by the IRS’s four-part test, the stringent regulatory definitions surrounding QREs, and an ever-evolving body of complex case law.

The Rigorous Application of the IRS Four-Part Test

To legally qualify for the federal R&D tax credit, an activity must comprehensively satisfy all four distinct criteria of the test outlined in IRC Section 41(d). The burden of proof in an audit scenario rests entirely upon the taxpayer, who must maintain contemporaneous documentation to substantiate that these requirements are met for every single business component claimed.

The first statutory requirement is the Permitted Purpose test. The research activities must be undertaken with the specific intention to discover information that is useful in the development of a new or improved business component to be utilized by the taxpayer. A “business component” is legally defined as a product, process, computer software, technique, formula, or invention that is to be held for sale, lease, or license, or used by the taxpayer in their own trade or business. The targeted improvement must strictly relate to enhanced functionality, increased performance, superior reliability, or elevated quality. Any research efforts directed solely at aesthetic, cosmetic, or seasonal design enhancements are explicitly excluded from eligibility by statute.

The second requirement demands that the research be Technological in Nature. The process of experimentation undertaken by the taxpayer must fundamentally rely upon the established principles of the hard sciences. This is statutorily limited to the physical sciences, biological sciences, engineering disciplines, or computer science. Research that relies upon the soft sciences, such as economics, behavioral psychology, management studies, or general market research, categorically fails this test and does not qualify for the credit. The discovery of information must be inherently technological, meaning that the fundamental principles utilized to eliminate the uncertainty are firmly rooted in these recognized scientific disciplines.

The third requirement is the Elimination of Uncertainty. At the exact outset of the research endeavor, there must be a definitive, recognizable technological uncertainty concerning either the overall capability of developing the business component, the specific method or process required for developing or improving the business component, or the appropriate final design of the business component. Technical uncertainty legally exists if the information available to the taxpayer and their engineering teams at the beginning of the project does not clearly establish the capability or method of achieving the desired result, or the optimal design necessary to accomplish the permitted purpose.

The fourth and final requirement is the Process of Experimentation. The taxpayer must engage in a systematic, evaluative process designed specifically to analyze one or more alternatives to achieve a result where the capability or the method of achieving that result remained uncertain at the beginning of the taxpayer’s activities. This rigorous process typically involves formulating scientific hypotheses, designing and executing highly structured testing methodologies, mathematically analyzing the resulting data, and iteratively refining the original hypothesis based on the empirical outcomes. Activities such as advanced predictive modeling, complex digital simulation, and documented, systematic trial and error are the critical hallmarks of satisfying this requirement.

The Complex Dynamics of IRC Section 174 and Qualified Research Expenses

Expenditures that are deemed eligible for the credit, formally known as Qualified Research Expenses, generally fall into three highly specific statutory categories. The first and typically largest category encompasses the W-2 taxable wages paid to employees who are directly engaging in, immediately supervising, or directly supporting the qualified research activities. The second category includes the cost of tangible supplies that are directly consumed, destroyed, or heavily utilized during the research and development process, explicitly excluding land or depreciable property. The third category allows taxpayers to capture sixty-five percent of the costs associated with hiring third-party contract researchers, provided the taxpayer retains the economic risk and substantial rights to the research.

The interaction between IRC Section 41, which governs the tax credit calculation, and IRC Section 174, which governs the deductibility of research and experimental (R&E) expenditures, is profoundly complex and has recently undergone transformative, highly disruptive legislative shifts. Historically, Section 174 served as a taxpayer-friendly provision that allowed businesses to immediately deduct all R&E expenditures in the exact year they were incurred, providing vital liquidity to innovative firms. However, this paradigm was shattered by the enactment of the Tax Cuts and Jobs Act (TCJA). Under the TCJA, taxpayers were suddenly required to strictly capitalize all domestic R&E expenditures and systematically amortize them over a five-year period (and fifteen years for foreign research) for all tax years beginning after December 31, 2021.

This aggressive capitalization mandate significantly altered corporate cash flows, artificially inflating taxable income for highly innovative companies and massively increasing compliance burdens. This highly contested environment persisted until the sudden enactment of the “One Big Beautiful Bill Act” (OBBBA) on July 4, 2025. Under the newly established framework of IRC Section 174A, the pre-TCJA deductibility of domestic R&E expenditures was permanently restored for tax years beginning after December 31, 2024.

The OBBBA legislation provided critical, highly specific transition rules allowing taxpayers to strategically navigate the damage caused between 2022 and 2024. Taxpayers are now permitted to deduct their previously capitalized and unamortized domestic R&E expenditures over a highly flexible one- or two-year period. Applying the new Section 174A rules for domestic expenditures constitutes a formal change in method of accounting, which is implemented on a cut-off basis as clarified by Revenue Procedure 2025-28. This effectively untethers billions of dollars of trapped innovation capital, providing an immediate, massive cash benefit that elegantly avoids the administrative nightmares associated with filing complex amended returns for the prior periods.

| Regulatory Regime |

Domestic R&E Treatment |

Foreign R&E Treatment |

Transition / Recovery Mechanism |

| Pre-2022 (Historical IRC 174) |

Immediate full deduction |

Immediate full deduction |

N/A |

| 2022-2024 (TCJA Mandate) |

Mandatory 5-year amortization |

Mandatory 15-year amortization |

N/A |

| Post-2024 (OBBBA IRC 174A) |

Immediate full deduction restored |

Mandatory 15-year amortization remains |

1- or 2-year accelerated deduction of unamortized 2022-2024 costs |

The Funded Research Exclusion and Evolving Judicial Precedents

A critical barrier to claiming the federal R&D credit, particularly relevant for the architecture, engineering, and contract manufacturing sectors prevalent in Shawnee, is the “funded research exclusion” dictated by Section 41(d)(4)(H). The statute strictly mandates that if research is funded by a government grant, a private contract, or another entity, the taxpayer actually performing the research is completely ineligible to claim the tax credit for those specific activities. To successfully navigate this treacherous exclusion, a taxpayer must conclusively demonstrate two critical, heavily audited elements: they must legally bear the financial economic risk of the research failing, and they must retain substantial rights to the resulting intellectual property or developed technology.

Recent decisions by the United States Tax Court have heavily scrutinized the minutiae of commercial contract terms to determine funding status. In the highly publicized case of Phoenix Design Group, Inc. v. Commissioner, the Tax Court ruled decisively against a professional engineering firm. The court determined that the firm had not engaged in qualified research because it failed to satisfy the strict, historical requirements of Section 174 and Section 41, highlighting the IRS’s rigorous, unyielding enforcement of the exact regulatory language regarding what constitutes true experimental expenditures versus routine engineering.

Conversely, taxpayers have achieved significant victories when their contract structures are properly aligned with the law. In Smith v. Commissioner, a prominent architectural firm successfully defended against an aggressive IRS motion for summary judgment. The IRS had vigorously argued that the firm’s clients fundamentally funded the research because the firm was only contractually required to meet standard professional engineering standards, which allegedly shielded them from any real financial risk if a design failed. The court recognized, however, that specific, carefully drafted contract provisions could indeed place the ultimate financial burden of failure squarely on the design firm, thus establishing the requisite economic risk.

The Populous case further solidified the specific parameters for contractors, particularly concerning the widespread use of firm-fixed-price contracts. The court logically concluded that research conducted under a standard firm-fixed-price contract is generally not considered “funded” by the client. This is because the taxpayer is not being paid an hourly rate specifically to conduct the research activities themselves; rather, they are being paid a flat fee for the successful delivery of a final, working product or design. If the underlying research fails, the taxpayer must absorb the entire cost of the overruns and the subsequent redesigns, thereby unequivocally bearing the economic risk of the endeavor. Furthermore, the court clarified that as long as the taxpayer retains the legal right to utilize the research results, methodologies, and engineering techniques in their broader trade or business—even if the specific client retains the exclusive rights to the final, specific project deliverables—the substantial rights requirement is successfully met, clearing the path for the R&D credit claim.

Detailed Analysis: The Kansas State R&D Tax Credit (K.S.A. §79-32,182b)

State-level Research and Development tax credits serve as a highly powerful, localized complement to federal incentives. The Kansas Research and Development Tax Credit, statutorily governed by K.S.A. §79-32,182b, has been structurally modernized and aggressively expanded to attract and retain high-technology industries, advanced manufacturing, and biological research within the state’s borders. This critical incentive provides a direct offset against Kansas state income tax liabilities and is strictly administered by the Kansas Department of Revenue (KDOR), which manages the complex lifecycle of the incentive from pre-claim certification through post-filing compliance auditing.

Prior to the legislative sessions of 2022, the Kansas R&D credit, while useful, was restricted in its overall economic utility. It offered a moderate 6.5 percent rate and was exclusively available to traditional C-corporations. This structural limitation effectively excluded the vast majority of pass-through entities—such as S-corporations, Partnerships, and Limited Liability Companies (LLCs)—which form the vital backbone of many innovative startup and mid-market technology sectors. Recognizing the urgent macroeconomic need to competitively position the state’s economy against neighboring technology hubs, the Kansas legislature enacted sweeping, transformative enhancements through House Bill 2239, which became fully effective for all taxable years commencing after December 31, 2022.

Core Provisions and Modernizations of K.S.A. §79-32,182b

The most immediate and impactful change was the Increased Credit Rate. The statutory rate applied to excess QREs was increased by an impressive fifty-four percent, moving from the historical 6.5 percent to a robust 10 percent. The credit is precisely calculated based on the amount by which the current year’s Kansas-sourced expenditures exceed the taxpayer’s average of the actual expenditures made for such purposes in the current taxable year and the two immediately preceding taxable years. This specific mathematical formulation is designed to consistently reward incremental, year-over-year growth in research activities within the state.

The second major modernization was the Expanded Entity Eligibility. The antiquated C-corporation limitation was entirely abolished. The credit is now universally available to any Kansas income taxpayer, explicitly including individuals, S-corporations, partnerships, and LLCs. This critical expansion allows the tax benefit to seamlessly pass through the corporate structure directly to the individual shareholders and partners via Schedule K-1, democratizing the incentive for the modern business landscape.

Perhaps the most revolutionary addition to the Kansas statute is the introduction of unconditional credit Transferability. For tax year 2023 and all subsequent years, innovative taxpayers who generate the credit through qualified research but lack a current state tax liability can transfer the full, exact amount of the credit to any other person or corporate entity. This process requires the formal submission of Form K-260 to the KDOR to document the transaction. The credit may only be transferred a single time, and the receiving transferee legally assumes all the carryforward rights and utilization limitations that applied to the original earner. This provision is particularly vital for pre-revenue biotechnology and software startups operating in Shawnee, allowing them to monetize their R&D efforts immediately by selling the credits for cash to highly profitable, established Kansas entities.

Regarding Utilization and Carryforward mechanics, the state maintains a fiscal control mechanism. In any given single tax year, a taxpayer may only offset up to twenty-five percent of their total calculated state tax liability utilizing the R&D credit (this includes the current year credit plus any applicable carryforward amounts). However, the state is generous with the unused portion, which can be carried forward indefinitely in twenty-five percent annual increments until the entire value of the credit is fully exhausted. It is also critical to note that under the new KDOR Notice 23-09 guidelines, taxpayers must now proactively complete and submit Form K-204, the Research and Development Credit Application, to the state before they are permitted to formally claim the credit on their tax return using Schedule K-53.

Strategic Comparison: Federal versus Kansas R&D Tax Credit

The following table synthesizes the distinct structural mechanisms, calculation methodologies, and operational limitations of the United States federal and Kansas state R&D tax credit frameworks:

| Structural Feature |

United States Federal R&D Credit (IRC §41) |

Kansas State R&D Credit (K.S.A. §79-32,182b) |

| Statutory Credit Rate |

Varies (up to 20% of excess QREs or 14% via ASC method) |

Flat 10% on excess QREs (Effective post-2022) |

| Base Period Calculation |

Complex historical base period or simplified 3-year average (ASC) |

Average of current and prior two years’ actual QREs |

| Eligible Entity Structures |

Universally available to all entity types |

Available to all entity types (C-Corp restriction removed 2023) |

| Geographic Expenditure Limitation |

All domestic U.S. qualified expenditures |

Strictly limited to Kansas-sourced expenditures |

| Credit Transferability |

Not transferable |

Fully transferable one time for taxpayers with no current liability |

| Carryforward Provisions |

Limited to 20 years |

Indefinite duration (utilized in 25% annual increments) |

| Liability Utilization Limit |

Can offset full liability (subject strictly to AMT rules) |

Hard limit of 25% of total tax liability per single year |

| Required Filing Documentation |

IRS Form 6765 |

KDOR Form K-204 (Application) and Form K-53 |

To illustrate the mathematical application of the Kansas state credit under the post-2022 enhanced 10% rate, consider a hypothetical Shawnee-based engineering firm that has demonstrated consistent growth in their qualified research expenditures:

- Year 1 (Prior): $450,000 QREs

- Year 2 (Prior): $650,000 QREs

- Year 3 (Current): $1,300,000 QREs

The Base Amount is calculated as the average of the three years: ($450,000 + $650,000 + $1,300,000) / 3 = $800,000. The Excess QREs for the current year: $1,300,000 (Current) – $800,000 (Base) = $500,000. The Kansas State Credit Generated: $500,000 * 10% = $50,000. This $50,000 credit can then be utilized to offset up to 25% of the firm’s current state tax liability, carried forward indefinitely, or, if the firm lacks liability, transferred entirely to another Kansas taxpayer for immediate capital.

Macroeconomic Synthesis: The Multiplier Effect of Local Incentives and Federal Tax Synergy

The profound industrial success of Shawnee, Kansas, cannot be attributed to a single variable. Rather, it is the result of a highly deliberate, macroeconomic synthesis. The confluence of the restored United States federal tax code deductibility, the modernized and highly aggressive Kansas state R&D tax credit, and the hyper-targeted local infrastructural investments originating from the JCERT initiative creates an unprecedented, compounding multiplier effect for technological companies operating within the city’s borders.

The Johnson County Education Research Triangle (JCERT) stands as the most critical localized economic catalyst. Approved by voters in 2008 through a 1/8-cent county-wide sales tax, this initiative fundamentally altered the intellectual capital of the region. A comprehensive fifteen-year economic impact study conducted by the Mid-America Regional Council (MARC) revealed that while the tax generates an average of $18 million annually, it returns a staggering $105 million per year in direct economic impact to the Kansas City metropolitan region. Over two decades, JCERT is projected to increase the region’s Gross Domestic Product by over $1.5 billion and boost personal income by nearly $600 million. By continuously funding the $25 million University of Kansas Clinical Research Center in Fairway, the $28 million K-State International Animal Health and Food Safety Institute in Olathe, and the $23 million KU Edwards BEST Center, JCERT guarantees a massive, uninterrupted pipeline of highly specialized scientists, engineers, and clinical researchers directly into the Shawnee labor pool.

| Shawnee Sales Tax Breakdown (Reflecting JCERT Investment) |

Tax Rate Component |

| State of Kansas Base Rate |

6.500% |

| Johnson County Base Tax |

1.475% |

| Research Triangle (JCERT County-Wide Tax) |

0.125% |

| City of Shawnee Base Tax |

1.000% |

| Shawnee Public Safety |

0.125% |

| Shawnee Parks and Pipes |

0.125% |

When companies tap into this elite labor pool to conduct research, they are simultaneously supported by a matrix of localized business incentives. The City of Shawnee aggressively utilizes the Kansas Constitution’s provisions to offer 100% real property tax abatements for up to ten years for companies conducting research and development or storing goods in interstate commerce. Furthermore, the city heavily deploys Industrial Revenue Bonds (IRBs) to finance new facilities and Tax Increment Financing (TIF) to revitalize commercial corridors.

The true multiplier effect is realized when these local infrastructural advantages collide with the modern tax code. Historically, highly innovative companies, particularly pre-revenue startups or large subsidiaries attempting to scale experimental technologies, faced immense, often fatal, cash-flow pressures due to the inability to immediately offset the massive upfront costs of R&D. The TCJA’s draconian requirement to amortize Section 174 costs over five years exacerbated this issue exponentially, creating massive, artificial taxable income events even when cash was being actively burned on high-risk research.

The enactment of the One Big Beautiful Bill Act in 2025 radically altered this hostile paradigm. By definitively allowing the full, immediate expensing of domestic R&E under Section 174A, federal tax liabilities are aggressively minimized in the exact year the technological risk is taken. When this massive federal relief is layered seamlessly with the K.S.A. §79-32,182b credit, the economic advantages compound dramatically. The Kansas credit’s sharp increase to 10% of excess QREs provides a highly competitive, top-tier state-level incentive that directly lowers the ultimate cost of capital.

Most critically, the 2023 introduction of absolute transferability to the Kansas R&D credit mechanism serves as a direct, state-sanctioned capital infusion vehicle for pre-revenue and early-stage companies. A Shawnee-based biotechnology startup operating within the Animal Health Corridor, or a logistics software developer engineering new algorithms, may not generate actual state income tax liability for several years. Under the new regime, they can meticulously quantify their state R&D credits and immediately sell them on the open market to a highly profitable, established Kansas corporation, such as a local bank or a legacy manufacturing firm. This legal mechanism miraculously transforms what was once a highly illiquid, deferred tax asset sitting uselessly on a balance sheet into immediate, liquid working capital. This capital is then subsequently reinvested to fuel further hiring of advanced engineers and clinical scientists originating from the local JCERT-funded educational institutions, completing the economic cycle.

Final Thoughts

Shawnee’s profound evolution from a simple nineteenth-century agrarian trail junction into a twenty-first-century nucleus for global logistics, advanced animal health, and complex engineering is not merely an accident of geography or simple suburban sprawl. It is the highly deliberate result of visionary infrastructural planning, intensely targeted local educational investments through JCERT, and the strategic, masterful maximization of both state and federal tax frameworks. As complex case law continues to aggressively refine the exact boundaries of what constitutes qualified research and acceptable contract funding, technological companies situated in this precise geographical location are uniquely and powerfully equipped to mitigate the severe financial risks of innovation while simultaneously capturing the absolute maximal regulatory rewards offered by the United States government and the State of Kansas.

The information in this study is current as of the date of publication, and is provided for information purposes only. Although we do our absolute best in our attempts to avoid errors, we cannot guarantee that errors are not present in this study. Please contact a Swanson Reed member of staff, or seek independent legal advice to further understand how this information applies to your circumstances.

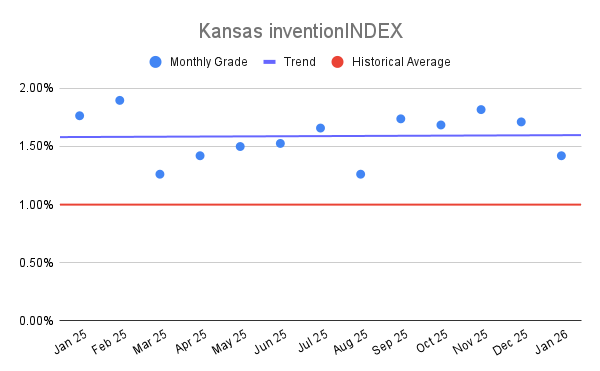

Kansas inventionINDEX January 2026:<

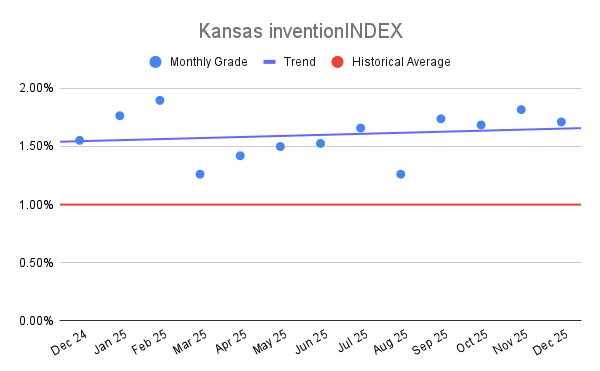

Kansas inventionINDEX January 2026:<  Kansas inventionINDEX December 2025:

Kansas inventionINDEX December 2025: