The Limited Liability Entity Tax (LLET) under KRS 141.0401 is a mandatory minimum business excise tax in Kentucky. The Kentucky Qualified Research Facility Tax Credit (QRFC) allows businesses to offset their LLET liability by claiming a nonrefundable 5% credit on qualified research and development capital expenditures. This intersection offers strategic tax minimization opportunities with a 10-year carryforward provision for excess credits.

The Limited Liability Entity Tax (LLET), codified under Kentucky Revised Statute (KRS) 141.0401, is a mandatory business excise tax levied on most limited liability entities operating in the Commonwealth. The Kentucky Qualified Research Facility Tax Credit (QRFC) is a potent state tax incentive designed to reduce the cost of constructing or equipping research facilities, explicitly allowing the credit to offset LLET liability.

The LLET functions as a minimum tax structure calculated on economic activity, ensuring all covered entities contribute a baseline amount regardless of profitability. The QRFC offers a nonrefundable 5% credit on qualified capital expenditures for R&D infrastructure, directly lowering the required LLET payment and providing a strategic 10-year carryforward for excess credit amounts. This intersection provides a significant tax minimization opportunity for businesses committed to capital investment in Kentucky-based research and development activities.

Statutory Foundation: The Limited Liability Entity Tax (LLET) Under KRS 141.0401

The Limited Liability Entity Tax (LLET) is one of the foundational corporate tax elements in Kentucky, designed to ensure that most businesses operating with limited liability protection contribute to the state’s revenue base, irrespective of net income.

Applicability and Scope: Defining Taxable Entities

The LLET is imposed universally on every corporation and limited liability pass-through entity (PTE) doing business in Kentucky. This mandate includes C corporations, S corporations, limited liability companies (LLCs), and limited partnerships (LPs). This comprehensive scope ensures wide tax capture across varying legal and financial structures.

Corporations file the LLET and Corporate Income Tax (CIT) return using Form 720 (Kentucky Corporation Income Tax and LLET Return), which must be accompanied by a complete copy of the federal Form 1120 and relevant federal schedules such as Form 1125-A (Cost of Goods Sold) and Form 4562 (Depreciation and Amortization). Pass-through entities file Form PTE.

KRS 141.0401 provides specific statutory exemptions. These include financial institutions, insurance companies, qualified investment partnerships (QIPs), and organizations exempt under IRC Section 501. Beyond these defined exemptions, the Department of Revenue (DOR) retains the authority to promulgate administrative regulations defining “qualified exempt organization,” including the critical power to exclude entities created primarily for tax avoidance purposes with no legitimate business objective.

Defining the Dual Tax Base and Minimum Liability

The “Lesser Of” Rule

- Gross Receipts Base: This is calculated at a rate of $0.095 per $100 of adjusted Kentucky gross receipts (or 0.095%). Gross receipts are broadly defined to include sales, rental income, proceeds from property sales, interest, and dividends.

- Gross Profits Base: This is calculated at a rate of 0.75% of Kentucky gross profits.

Cost of Goods Sold Restriction Nuance

The determination of “gross profits” requires a nuanced understanding of allowable deductions. KRS 141.0401(1)(d) strictly dictates that Cost of Goods Sold (COGS) can only be claimed for costs related to specific activities: manufacturing, producing, reselling, retailing, or wholesaling.

For research and development firms, this restriction holds significant financial implications. Entities engaged primarily in high-cost, non-manufacturing R&D services—where major expenses may include substantial specialized engineering payrolls or software development costs—may find that these costs are ineligible to be classified as COGS under the statute. The inability to deduct these routine operating expenses from gross receipts artificially inflates the “gross profits base,” potentially leading the entity to remit a significantly higher LLET than if it were a manufacturing company with similar gross receipts but higher statutorily eligible COGS. Tax planning must, therefore, scrutinize the nature of R&D activity to ensure maximum COGS eligibility.

The Statutory Minimum

Regardless of the calculated amount based on gross receipts or gross profits, every entity subject to LLET must pay a mandatory statutory minimum tax of one hundred seventy-five dollars ($175). This minimum establishes a non-reducible floor for the liability, meaning no tax credit, including the QRFC, can reduce the amount payable below this threshold.

LLET as a Pre-Payment of Corporate Income Tax (CIT)

The LLET is not merely an additional tax; it serves a structural role in the overall corporate tax framework. For a C-Corporation, the LLET functions as a pre-payment of the Corporate Income Tax (CIT) imposed by KRS 141.040. The corporation is allowed to reduce its CIT liability by the amount of the LLET paid, after subtracting the $175 minimum tax.

PTE Member LLET Credit Constraint

The mechanism becomes more constrained when LLET flows through a PTE to its individual members, partners, or corporate shareholders. An individual owner is allowed a credit against the income tax imposed by KRS 141.020, equal to their proportionate share of the LLET, reduced by the $175 minimum tax and any other allowed credits.

A vital constraint is placed on this flow-through credit: it can only be applied against the income tax assessed on income derived from that specific limited liability pass-through entity. Furthermore, any remaining portion of the LLET credit is explicitly disallowed and cannot be carried forward to the subsequent year. This non-carryforward restriction underscores the strategic necessity of utilizing long-lived credits, such as the QRFC, before relying on the LLET flow-through credit, as the latter has limited application life.

The Kentucky R&D Incentive: Qualified Research Facility Tax Credit

Definition and Scope: A Capital Investment Focus

Eligible Costs and Property

The definition of “construction of research facilities” is specific, covering the acts of constructing, remodeling, equipping, or expanding existing facilities located physically within Kentucky for qualified research purposes.

Crucially, the credit includes only tangible, depreciable property and expressly excludes any amounts paid or incurred for replacement property. This mandate targets new, incremental capital investments rather than maintenance or replacement cycles, distinguishing the Kentucky incentive structure from broad federal R&D credit provisions.

Calculation and The IRC Section 41 Linkage

The credit calculation is straightforward compared to its federal counterpart. The 5% rate is applied directly to the total eligible capital costs incurred during the tax year. The Kentucky statute does not require a fixed-base percentage calculation or prior-year averaging, meaning that 100% of eligible costs placed in service during the year qualify fully for the 5% credit.

The eligibility of the activity conducted within the facility is intrinsically linked to federal law. The activity must constitute “qualified research” as defined in Section 41 of the Internal Revenue Code (IRC § 41). This linkage requires the underlying R&D project to involve a process of experimentation intended to eliminate scientific or technical uncertainty, leading to a new or improved product or process. Consequently, even though the state credit is claimed on facility costs, the taxpayer must maintain federal-quality documentation to justify the research activities that utilize the facility.

Credit Utilization and Carryforward Provisions

As a nonrefundable credit, the QRFC can only offset existing tax liabilities; it cannot generate a cash refund. It is explicitly authorized for application against the LLET imposed by KRS 141.0401 and against corporate income tax (KRS 141.040) or individual income tax (KRS 141.020). The credit must be claimed on the tax return for the year during which the tangible, depreciable property is placed in service.

The longevity of the QRFC is a significant advantage: any unused credit may be carried forward and applied for up to ten (10) subsequent taxable years. This extended carryforward period provides long-term certainty for recovering large capital investments.

| Credit Percentage | Eligible Cost Type | Qualified Property | Nonrefundable Status | Carryforward Period |

|---|---|---|---|---|

| 5% | Construction, Remodeling, Expansion, Equipping of KY Facilities | Tangible, Depreciable Property (Non-Replacement) | Nonrefundable | 10 Years |

DOR Guidance: The Mechanics of the LLET and R&D Credit Offset

The Kentucky Department of Revenue (DOR) dictates the precise mechanism by which the QRFC is applied to reduce the LLET and subsequent income tax liabilities. This application is subject to a strict ordering of credits defined in KRS 141.0205.

Direct Offset Authority and Credit Ordering

The QRFC is granted explicit statutory authority to be applied against the LLET. For corporate taxpayers, the credit is applied directly against the calculated tax liability, reducing the LLET due down to the $175 minimum threshold. Any remaining portion of the QRFC is then applied against the Corporate Income Tax (CIT).

The prioritization of credit use is a critical compliance matter. Nonrefundable business credits, such as the QRFC, must be applied in the order prescribed by law to ensure proper utilization and preservation of the carryforward capability.

C Corporation Claim Process (Form 720)

A C-Corporation uses Form 720 (Kentucky Corporation Income Tax and LLET Return) to claim the credit. After calculating the gross receipts and gross profits bases and determining the LLET liability, the corporation applies the QRFC.

The utilized and carryforward credit amounts are tracked on supplemental forms. Taxpayers must enter the claimed credit amount on Schedule TCS (Tax Credit Summary Schedule) or Schedule ITC (for investment and other credits) according to the instructions for those schedules. This integrated filing process links the capital investment claim directly to the corporation’s overall tax reduction strategy.

Pass-Through Entity Flow-Through Mechanics

The tax treatment for Pass-Through Entities (PTEs) involves unique complexities due to the flow-through mechanism. The QRFC is earned at the entity level but is then passed through to the ultimate partners, members, or shareholders.

Reporting and Utilization

The PTE reports the distribution of the credit on the Kentucky Schedule K-1 for each owner. Owners then claim the passed-through credit against their personal tax liability (if an individual) or against their corporate CIT/LLET (if a corporate member).

The credit is specifically designed to flow through multiple layers of limited liability pass-through entities. In such multi-tiered structures, the owner must be the taxpayer who ultimately pays the tax on the limited liability pass-through entity’s income to claim the credit. Schedule L-C must be submitted with the applicable return (Form 720, PTE, etc.) to accurately attribute proportionate shares of sales and cost data through complex organizational hierarchies.

Essential Forms and Documentation Mandates

The integrity of the QRFC claim, particularly its long-term viability under the 10-year carryforward rule, depends entirely on precise compliance with DOR documentation requirements.

Schedule QR – The Qualified Research Facility Tax Credit

The Schedule QR (Qualified Research Facility Tax Credit) is the primary compliance document for initiating and maintaining the credit. It serves a dual purpose:

- Initial Filing: It is filed in the year the qualifying property is placed in service to determine the total credit amount earned against the income tax and LLET liability.

- Annual Tracking: A copy of the Schedule QR must be attached to the tax return each year the credit is claimed until the full credit amount is utilized or the 10-year carryforward period expires, whichever occurs first.

This continuous re-certification requirement is a critical compliance measure that allows the DOR to maintain an accurate, ongoing audit trail of the taxpayer’s credit balance over a decade, which is essential for managing a nonrefundable, long-lived credit.

Detailed Documentation and Audit Defense

Taxpayers must support the credit claim with rigorous evidence demonstrating both the financial costs and the technical qualifications of the research activity.

A mandatory supporting schedule must be included with the return. This schedule requires a line-item listing of all tangible, depreciable property used for the research facility. For each item, the taxpayer must provide the date purchased, the precise date the property was placed in service, a detailed description, and its cost. The date the property is placed in service is critical because it dictates when the credit officially becomes available for utilization.

Furthermore, linking the capital expenditure to “qualified research” (IRC § 41) requires robust technical documentation. The IRS and, by extension, the Kentucky DOR demand detailed records that prove the research activities involved overcoming genuine technological or scientific uncertainties. This documentation should include design iterations, technical reports, meeting notes, and engineering data captured in real-time. A failure to provide this technical substantiation, even for a capital cost-based credit, increases the risk of the entire claim being invalidated under audit.

Detailed Case Study: LLET Offset Example

This example illustrates the financial benefit and required sequencing for a C-Corporation making a significant capital investment in a research facility in Kentucky.

Scenario Parameters:

- Entity: Bluegrass Innovations Corp. (C-Corp)

- Tax Year: 2024

- Qualified R&D Capital Investment: $1,500,000 (new laboratory equipment, tangible, depreciable, placed in service 2024).

- Operating Financial Data:

- Kentucky Gross Receipts: $15,000,000

- Kentucky Gross Profits: $2,500,000

- Kentucky Net Income (CIT Base): $1,000,000

Step 1: Determine Calculated LLET Liability (KRS 141.0401)

The corporation must calculate the tax based on both gross receipts and gross profits and remit the lesser amount.

| LLET Basis Calculation | Formula | Amount |

|---|---|---|

| Gross Receipts Base | $15,000,000 x 0.095% | $14,250 |

| Gross Profits Base | $2,500,000 x 0.75% | $18,750 |

| Calculated LLET Due (Lesser Of) | The lesser of the two amounts is $14,250 | $14,250 |

Step 2: Determine R&D Credit Earned (QRFC)

The credit is 5% of the qualified capital costs, with no base reduction.

QRFC Earned = $1,500,000 x 0.05 = $75,000

Step 3: Application of QRFC Against LLET and Income Tax

The QRFC is applied first against the LLET, but the LLET liability cannot be reduced below the statutory minimum of $175.

- LLET Offset:

- Maximum QRFC used against LLET: $14,250 (LLET Liability) – $175 (Minimum Tax) = $14,075

- LLET Paid (Post-Credit): $175

- Corporate Income Tax (CIT) Calculation:

- CIT Pre-Credit Liability: $1,000,000 Net Income x 5% Flat Rate = $50,000.

- CIT Reduction by LLET Paid: The CIT liability is automatically reduced by the LLET component paid after the credit is applied, excluding the minimum tax.

- CIT Reduction: $50,000 – $14,075 = $35,925 (Remaining CIT Liability)

- QRFC Utilization against CIT:

- QRFC Remaining for CIT: $75,000 (Total Earned) – $14,075 (Used for LLET) = $60,925

- QRFC Used against CIT: The remaining CIT liability of $35,925 is fully offset.

- CIT Paid (Post-Credit): $0

- Carryforward Determination:

- Total QRFC Utilized in Current Year: $14,075 (LLET) + $35,925 (CIT) = $50,000

- QRFC Unused: $75,000 (Total Earned) – $50,000 (Used) = $25,000

- This $25,000 is carried forward for up to 10 subsequent taxable years.

| Financial Metric/Calculation | Value | Notes |

|---|---|---|

| LLET Pre-Credit Liability | $14,250 | Lesser of Gross Receipts/Profits |

| LLET Minimum Tax Due | $175 | Mandatory floor |

| Max QRFC Applicable to LLET | $14,075 | LLET Liability minus $175 minimum |

| QRFC Generated | $75,000 | 5% of Qualified Costs |

| Corporate Income Tax (CIT) Pre-Credit | $50,000 | 5% flat rate |

| CIT Reduction by LLET Paid | $14,075 | LLET acts as a pre-payment |

| Remaining CIT Liability | $35,925 | CIT after LLET adjustment |

| QRFC Utilized Against CIT | $35,925 | Full remaining CIT offset |

| Total QRFC Utilized in Current Year | $50,000 | LLET ($14,075) + CIT ($35,925) |

| Unused QRFC Carryforward | $25,000 | Available for 10 subsequent years |

Advanced Strategic Tax Considerations

Interacting with Federal Tax Changes: IRC Section 174

Kentucky adheres to the federal tax code’s requirement, effective for tax years beginning on or after January 1, 2023, that taxpayers capitalize and amortize Research and Experimental (R&E) expenses rather than immediately deducting them. This conformity, driven by House Bill 360 updating the IRC reference date to December 31, 2022, creates a significant tax planning dynamic.

By deferring the deduction of R&E expenses, the state taxable income (the CIT base) is inherently increased. This rise in the CIT liability, while increasing the total tax exposure before credits, significantly increases the capacity for the business to immediately utilize its nonrefundable QRFC. The strategic implication is that the effective tax increase caused by mandatory R&E capitalization actually enhances the value of the QRFC by providing a larger tax liability pool against which the credit can be fully applied in the current year, thereby minimizing the reliance on the 10-year carryforward.

Maximizing Flow-Through for Pass-Through Entities

For PTEs, the dual nature of the credits—the 10-year QRFC versus the non-carryforward LLET credit for owners—demands precise credit sequencing. The PTE must first apply the QRFC against any entity-level LLET liability (down to the $175 minimum). Any unused QRFC retains its valuable 10-year carryforward period.

The LLET credit that flows through to the owners is financially perishable, as any remaining amount unused against income derived from that PTE in the current year is permanently disallowed. Therefore, the entity must employ a strategy that prioritizes the use of the QRFC (the long-lived asset) over the LLET credit (the ephemeral asset) to maximize the overall benefit.

When dealing with complex, multi-tiered pass-through entities, the credit is designed to flow through to the ultimate taxpayer. Proper compliance necessitates the use of Schedule L-C to include the corporation’s proportionate share of sales and costs from all levels of the tiered structure when calculating the LLET.

Final Thoughts: Compliance, Opportunity, and the Kentucky Tax Landscape

KRS 141.0401 establishing the LLET is a fundamental component of Kentucky’s tax structure, enforcing a comprehensive, mandatory business privilege tax based on the lesser of gross receipts or gross profits, subject to a $175 minimum.

The Qualified Research Facility Tax Credit serves as a highly effective countermeasure and incentive. By authorizing the QRFC to directly offset the LLET, Kentucky effectively reduces the capital cost of R&D facilities by 5%. For businesses engaging in substantial capital expenditures, this credit mechanism significantly improves project economics, especially when considering the generous 10-year carryforward provision.

Optimal tax administration requires meticulous attention to two primary areas:

- Credit Sequencing: Taxpayers must strategically prioritize the utilization of the 10-year QRFC to maximize its value, especially for PTEs whose flow-through LLET credits have zero carryforward utility.

- Documentation and Compliance: The continuous filing of Schedule QR for the entire 10-year carryforward period, coupled with detailed schedules listing the “placed in service” dates and costs of tangible, depreciable property, is non-negotiable for audit defense. Furthermore, the technical linkage of the facility to qualified research activities (IRC § 41 standards) must be robustly documented to secure the claim.

By understanding the statutory requirements of the dual LLET base and strategically utilizing the QRFC, Kentucky businesses can effectively manage their mandatory tax burden while driving innovation and capital growth within the Commonwealth.

This page is provided for information purposes only and may contain errors. Please contact your local Swanson Reed representative to determine if the topics discussed in this page applies to your specific circumstances.

KRS 141.0401 (LLET) is a minimum tax based on your company’s activity volume (Gross Receipts or Profits), not just income.

While the Kentucky R&D Credit can offset this tax, specific ordering rules determine whether it shields your LLET liability or your Income Tax liability first.

Understand the “Double Tax” structure. Enter your financials to see how the LLET is calculated using the dual-method approach (Receipts vs. Gross Profits) and how the R&D Credit (KRS 141.205/141.390) applies to the final bill.

⚙ Financial Inputs

Total revenue within Kentucky.

Used to determine Gross Profits.

Subject to Corporate Income Tax (CIT).

Basis for the 5% Credit.

LLET Determination (Lower Amount Wins)

Final Liability Composition

In-Depth Analysis

KRS 141.0401, Guidance, and Application

Enacted to ensure that all limited liability entities doing business in Kentucky contribute to the tax base, the LLET functions effectively as a minimum tax. Unlike standard income tax which is based on net profitability, LLET is an assessment on the volume of business activity.

The tax is the lesser of:

- $0.095 per $100 of Gross Receipts

- $0.75 per $100 of Gross Profits (Gross Receipts minus Cost of Goods Sold)

Minimum Tax: $175

This structure is particularly aggressive towards high-volume, low-margin businesses, or startups that have significant revenue but high costs (net losses). Even if a company has a Net Loss for the year, they will owe LLET based on their receipts or gross profits.

Who We Are:

Swanson Reed is one of the largest Specialist R&D Tax Credit advisory firm in the United States. With offices nationwide, we are one of the only firms globally to exclusively provide R&D Tax Credit consulting services to our clients. We have been exclusively providing R&D Tax Credit claim preparation and audit compliance solutions for over 30 years. Swanson Reed hosts daily free webinars and provides free IRS CE and CPE credits for CPAs.

Are you eligible?

Why choose us?

Pass an Audit?

What is the R&D Tax Credit?

The Research & Experimentation Tax Credit (or R&D Tax Credit), is a general business tax credit under Internal Revenue Code section 41 for companies that incur research and development (R&D) costs in the United States. The credits are a tax incentive for performing qualified research in the United States, resulting in a credit to a tax return. For the first three years of R&D claims, 6% of the total qualified research expenses (QRE) form the gross credit. In the 4th year of claims and beyond, a base amount is calculated, and an adjusted expense line is multiplied times 14%. Click here to learn more.

Never miss a deadline again

Stay up to date on IRS processes

Discover R&D in your industry

R&D Tax Credit Preparation Services

Swanson Reed is one of the only companies in the United States to exclusively focus on R&D tax credit preparation. Swanson Reed provides state and federal R&D tax credit preparation and audit services to all 50 states.

If you have any questions or need further assistance, please call or email our CEO, Damian Smyth on (800) 986-4725.

Feel free to book a quick teleconference with one of our national R&D tax credit specialists at a time that is convenient for you.

R&D Tax Credit Audit Advisory Services

creditARMOR is a sophisticated R&D tax credit insurance and AI-driven risk management platform. It mitigates audit exposure by covering defense expenses, including CPA, tax attorney, and specialist consultant fees—delivering robust, compliant support for R&D credit claims. Click here for more information about R&D tax credit management and implementation.

Our Fees

Swanson Reed offers R&D tax credit preparation and audit services at our hourly rates of between $195 – $395 per hour. We are also able offer fixed fees and success fees in special circumstances. Learn more athttps://www.swansonreed.com/services/our-fees/

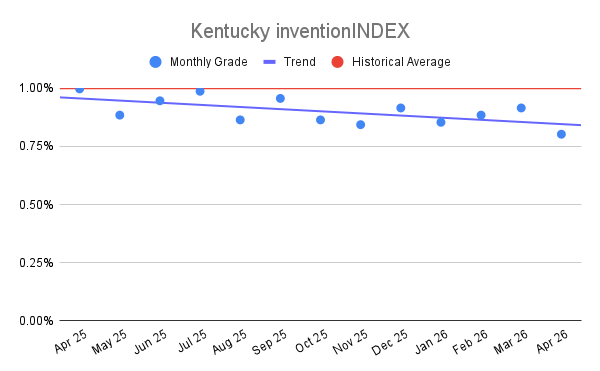

Kentucky inventionINDEX April 2026:

Kentucky inventionINDEX April 2026: