Part I: Industry Case Studies and Economic Development in Los Angeles

The Los Angeles metropolitan area represents a unique geographic and economic nexus that has historically fostered rapid industrial innovation[cite: 1]. Driven by an expansive topography, a diverse and massive labor force, and the presence of premier academic research institutions such as the California Institute of Technology (Caltech), the University of Southern California (USC), and the University of California, Los Angeles (UCLA), the region has birthed numerous global industries[cite: 1]. The following five case studies examine the historical development of critical sectors within Los Angeles and analyze how specific, hypothetical enterprises within these industries navigate the rigid federal and state Research and Development (R&D) tax credit requirements[cite: 1].

Case Study: Aerospace and Defense Manufacturing

The historical development of the aerospace and defense industry in Southern California is deeply intertwined with the region’s climatic and geographic advantages[cite: 1]. The industry’s genesis in the Los Angeles basin can be traced back to January 1910, when the city hosted the Los Angeles International Aviation Meet at Dominguez Field[cite: 1]. This event, which was the first major airshow in the United States and the second globally, drew an estimated quarter of a million spectators over ten days and jumpstarted regional interest in aviation technology[cite: 1]. Manufacturers rapidly relocated to the area, attracted by the temperate, year-round flying weather that allowed for uninterrupted testing, the expansive open landscapes ideal for constructing massive airfields, and the civic boosterism that aggressively courted industrial investments[cite: 1]. Furthermore, Los Angeles possessed “open-shop” labor rules that historically hindered the formation of unions, providing early aviation entrepreneurs with a highly competitive and flexible manufacturing cost structure[cite: 1].

By the late 1920s, following Charles Lindbergh’s transatlantic flight, commercial aviation investment skyrocketed, resulting in over twenty distinct airframe and aircraft engine manufacturers establishing operations in Southern California by 1928[cite: 1]. During World War II, the region transformed into the “Arsenal of Democracy”[cite: 1]. Massive production facilities produced tens of thousands of aircraft[cite: 1]. The onset of the Cold War transitioned the industry’s focus from mass manufacturing to advanced Research, Development, Testing, and Evaluation (RDT&E)[cite: 1]. Facilitated by billions of dollars in federal defense spending and a steady pipeline of highly educated STEM workers from local universities, Los Angeles pioneered legendary programs such as the U-2, the SR-71 Blackbird, and the B-2 Spirit stealth bomber[cite: 1]. While post-Cold War defense drawdowns caused legacy manufacturing to contract, Southern California remains a premier global hub for advanced aerospace innovation, autonomous systems, and commercial satellite manufacturing[cite: 1].

To illustrate the application of R&D tax credits within this sector, consider a hypothetical commercial aerospace firm based in El Segundo, California, that is developing a novel, lightweight carbon-fiber composite matrix for a reusable satellite launch vehicle payload fairing[cite: 1]. Under the federal framework of Internal Revenue Code (IRC) Section 41, the firm must satisfy the four-part test for qualified research[cite: 1]. The firm faces objective technological uncertainty regarding whether the new composite material can successfully withstand the extreme thermal dynamics and aerodynamic friction of atmospheric reentry while maintaining the necessary structural integrity[cite: 1]. The research fundamentally relies on the hard sciences of materials science and aerospace engineering, thereby satisfying the “technological in nature” requirement[cite: 1]. The payload fairing constitutes the new or improved business component[cite: 1]. The engineers engage in a rigorous process of experimentation by developing complex finite element analysis (FEA) computer models, conducting advanced computational fluid dynamics (CFD) simulations, and iteratively testing physical scaled prototypes[cite: 1].

The firm can claim the W-2 taxable wages of the aerospace engineers, data scientists, and the manufacturing technicians directly fabricating the experimental prototypes as Qualified Research Expenses (QREs)[cite: 1]. The cost of the raw carbon fiber, specialized bonding resins, and the time-sharing rental costs for cloud-based computing servers utilized for the CFD simulations qualify as supply and computer rental QREs[cite: 1]. However, the firm must navigate specific federal exclusions outlined in the Federal Acquisition Regulation (FAR) and the IRC[cite: 1]. If the firm produces Special Test Equipment or Special Tooling under a cost-reimbursement contract where the United States Government retains title, the costs are considered “funded” and are ineligible[cite: 1]. Furthermore, following the precedents established in the Little Sandy Coal case law, the firm must meticulously document the hours of front-line supervisors overseeing the wind tunnel tests to meet the 80% “substantially all” requirement[cite: 1].

Case Study: Entertainment Technology and Visual Effects (VFX)

The entertainment industry is the cultural and economic bedrock of Los Angeles, fundamentally shaping the city’s global identity and urban development[cite: 1]. Regular motion picture production commenced in Hollywood around 1911[cite: 1]. The initial migration of filmmakers from the East Coast to Southern California was primarily driven by a strategic imperative to escape the monopolistic control and aggressive litigation of Thomas Edison’s Motion Picture Patents Company[cite: 1]. Los Angeles offered unparalleled geographical isolation from Edison’s litigators, alongside diverse local topographies that could serve as highly varied cinematic backdrops[cite: 1]. Additionally, the region’s consistent sunlight allowed for reliable, year-round outdoor filming before the advent of high-powered artificial studio lighting systems[cite: 1].

By the 1920s, the Hollywood “studio system” had consolidated power, establishing Los Angeles as the undisputed “Entertainment Capital of the World”[cite: 1]. In the modern era, the integration of heavy computer science and digital rendering has transformed filmmaking[cite: 1]. Los Angeles is now the epicenter of digital visual effects (VFX), animation, and real-time virtual production technologies[cite: 1]. This evolution is driven by a highly specialized local workforce that uniquely blends artistic creativity with advanced software engineering and computational mathematics[cite: 1].

Consider a hypothetical visual effects studio located in Burbank, California, that is developing a proprietary, artificial intelligence-driven real-time rendering engine designed to process complex particle physics[cite: 1]. For the purposes of the R&D tax credit, the studio must cleanly separate artistic endeavors from technological innovations[cite: 1]. The uncertainty in this project lies in optimizing the algorithmic computational efficiency to render millions of polygons and complex volumetric data at a consistent sixty frames-per-second without causing hardware latency[cite: 1]. These activities fundamentally rely on the hard sciences of computer science and advanced mathematics[cite: 1]. The proprietary software rendering engine serves as the qualifying business component[cite: 1]. The software engineers engage in a systematic process of experimentation by writing custom C++ and Python code, testing various neural network architectures, and evaluating rendering latencies across different hardware configurations[cite: 1].

It is critical to demarcate the exclusions in this sector[cite: 1]. The creation of the digital art itself—the scriptwriting, the aesthetic choices of the director, the design of the character models, and the performance of the actors—is explicitly excluded from the credit, as it is not technological in nature and relates entirely to artistic style and taste[cite: 1]. However, the development of the underlying software tools, custom scripts, and rendering pipelines does qualify[cite: 1]. The wages of the software engineers and technical directors engaged in building these bespoke tools are eligible QREs[cite: 1]. From a state tax perspective, because the software engineers are physically based in Burbank, their wages qualify for the California R&D credit[cite: 1]. Furthermore, under the recently enacted California Senate Bill 711, the studio can immediately deduct these massive software development expenses for state income tax purposes[cite: 1].

Case Study: Biotechnology and Life Sciences

While the San Francisco Bay Area frequently receives historical primacy for the birth of the biotechnology industry, the Greater Los Angeles region has methodically developed a formidable, globally recognized life sciences cluster[cite: 1]. The primary catalyst for this regional ecosystem was the establishment of Amgen in Thousand Oaks, California, in 1980[cite: 1]. The geographic location was strategically chosen to bridge the massive academic research output of UCLA, Caltech, and the University of California, Santa Barbara[cite: 1].

The company achieved a historic scientific and commercial breakthrough with the development of recombinant protein therapies[cite: 1]. Amgen’s exponential growth injected massive financial capital and specialized talent into the regional economy[cite: 1]. Today, the Greater Los Angeles life science industry is a dynamic ecosystem encompassing three counties, employing over 94,000 workers, and contributing more than $60 billion in total economic output[cite: 1]. The region features highly robust sub-sectors focusing on precision medicine, synthetic biology, tissue banking, and cell therapies[cite: 1]. Amgen continues to anchor the region, recently announcing a $600 million investment to construct a state-of-the-art center for science and innovation at its Thousand Oaks global headquarters[cite: 1].

A clinical-stage biopharmaceutical startup located in Culver City, developing a novel monoclonal antibody therapy for the treatment of severe autoimmune diseases, provides a clear example of R&D tax credit eligibility[cite: 1]. The startup faces profound and objective technological uncertainty regarding the new drug’s physiological efficacy, long-term toxicity, pharmacokinetic profile, and optimal dosage parameters[cite: 1]. The investigative activities rely entirely on the biological sciences, organic chemistry, and molecular medicine[cite: 1]. The new therapeutic biological compound serves as the business component[cite: 1]. The process of experimentation is extensive, encompassing the entirety of the pharmaceutical drug discovery pipeline: developing novel assays, optimizing cellular fermentation processes, conducting pre-clinical testing, and eventually executing regulated FDA clinical trials[cite: 1].

Eligible QREs for the startup include the W-2 wages of principal investigators, microbiologists, and laboratory technicians directly involved in the research[cite: 1]. The cost of supplies consumed during the experimentation process—which can include chemical reagents, laboratory glassware, and biological cell samples—are also fully eligible[cite: 1]. Furthermore, the startup can claim up to 65% of the costs paid to third-party Clinical Research Organizations (CROs) for managing human clinical trials as Contract Research Expenses[cite: 1]. As an early-stage biopharmaceutical firm, the company likely operates at a significant net financial loss[cite: 1]. However, under federal law, a “qualified small business” can elect to apply up to $500,000 of its earned federal R&D credit directly against its employer portion of the OASDI (Social Security) payroll tax liability[cite: 1].

Case Study: Advanced Transportation and Electric Vehicles (EV)

The economic and infrastructural history of Los Angeles is inextricably linked to the automobile[cite: 1]. During the 1920s, automobile registration in the Los Angeles region quadrupled within an eight-year span[cite: 1]. This rapid adoption occurred concurrently with the gradual decline of the Pacific Electric railway system[cite: 1]. However, decades of heavily car-centric infrastructure led to severe environmental consequences, culminating in historic smog and air quality crises[cite: 1].

In direct response to this ecological challenge, California established the California Air Resources Board (CARB) and enacted the strictest environmental and vehicle emissions standards in the nation[cite: 1]. This regulatory environment effectively forced the automotive industry to pursue rapid technological innovation[cite: 1]. The region’s modern pivot toward advanced transportation and electrification is heavily driven by the presence of the Ports of Los Angeles and Long Beach[cite: 1]. Consequently, Southern California has evolved into a globally dominant cluster for the electric vehicle industry[cite: 1]. The region currently employs nearly 120,000 workers directly within the EV sector[cite: 1].

Consider a mechanical engineering firm based in Long Beach, California, that is designing an advanced, liquid-cooled battery thermal management system (BTMS) intended for retrofitting Class-8 heavy-duty electric drayage trucks[cite: 1]. The technical uncertainty in this endeavor relates to the challenge of maintaining optimal battery cell temperatures during high-torque load cycles[cite: 1]. The developmental work relies strictly on the principles of mechanical engineering, thermodynamics, and electrical engineering[cite: 1]. The BTMS hardware apparatus and its integrated controlling software algorithms constitute the new business component[cite: 1]. The process of experimentation involves designing iterative CAD models, prototyping heat sinks, and conducting stress testing under extreme simulated port loads[cite: 1].

It is crucial for the firm to understand the distinction between qualified supplies and capitalized equipment[cite: 1]. If the engineering firm purchases a $500,000 highly specialized CNC milling machine to mass-produce the final heat sinks, the cost of that depreciable machinery is strictly excluded from QREs[cite: 1]. However, the cost of raw aluminum, dielectric fluids, and electronic sensors consumed during the iterative testing and validation phases of the prototypes fully qualify[cite: 1].

Case Study: Apparel Manufacturing and Fashion Technology

Los Angeles boasts a deep, century-old legacy in apparel manufacturing, currently representing a seventeen-billion-dollar annual economic impact[cite: 1]. The industry’s foundational roots were planted in the late nineteenth century[cite: 1]. By the 1920s, the formation of the Associated Apparel Manufacturers of Los Angeles in 1921 organized the sector into a cohesive economic bloc[cite: 1]. Today, the downtown Los Angeles (DTLA) Fashion District remains the bustling hub of American garment production[cite: 1]. Facing pressure from low-cost overseas labor markets, the Los Angeles apparel industry has strategically pivoted toward high-tech, ethical, and sustainable manufacturing processes[cite: 1].

The apparel industry faces the highest level of regulatory scrutiny regarding R&D tax credit claims due to statutory exclusions[cite: 1]. Consider a textile manufacturer located in the DTLA Fashion District developing a novel, completely biodegradable synthetic fiber engineered from agricultural waste byproducts[cite: 1]. This manufacturer faces a significant legal hurdle known as the Swat-Fame / Leon Max obstacle[cite: 1]. Under IRC Section 41(d)(3)(B), research related to “style, taste, cosmetic, or seasonal design factors” is expressly and statutorily excluded from the credit[cite: 1]. Simply designing a new seasonal garment silhouette or selecting fabric colors does not meet the “technological in nature” test[cite: 1].

To qualify for the credit, the hypothetical DTLA manufacturer must demonstrate that they are not researching fashion; rather, they are researching polymer chemistry and materials science[cite: 1]. The objective technological uncertainty involves engineering the precise tensile strength, thermal elasticity, and chemical biodegradability metrics of the new synthetic fiber[cite: 1]. This investigative process fundamentally relies on the hard sciences of materials science and chemical engineering[cite: 1]. The novel synthetic fiber material and the modified mechanical extrusion machinery process serve as the business components[cite: 1]. The W-2 wages of the chemical engineers and materials scientists driving this innovation fully qualify as QREs[cite: 1]. Conversely, the wages of fashion designers sketching seasonal dress patterns absolutely do not qualify[cite: 1]. This precise, documented bifurcation is mandatory to survive subsequent FTB and IRS audits[cite: 1].

Part II: Detailed Analysis of United States Federal R&D Tax Credit Requirements

The United States federal Research and Development tax credit, codified under Internal Revenue Code (IRC) Section 41, provides a direct, dollar-for-dollar reduction in a taxpayer’s federal income tax liability for qualified research expenses (QREs) paid or incurred in the active conduct of a trade or business[cite: 1]. The fundamental formula for the regular credit calculates the benefit as generally equal to 20% of the amount by which the taxpayer’s current-year qualified research expenses exceed a historically calculated base amount[cite: 1].

The Statutory Four-Part Test

The foundation of the federal R&D tax credit is the rigid, statutory four-part test delineated in IRC Section 41(d)[cite: 1]. To be deemed eligible, the research activities must strictly satisfy all four criteria cumulatively[cite: 1].

| Statutory Requirement | Legal Basis & Description | Detailed Analysis & Application Standards |

|---|---|---|

| 1. The Section 174 Test | IRC § 41(d)(1)(A) | Expenditures must be legally eligible for treatment as research and experimental expenditures under IRC § 174. This necessitates that the activities be intentionally undertaken to discover information that would eliminate objective uncertainty concerning the capability, methodology, or appropriate design[cite: 1]. |

| 2. The Technological in Nature Test | IRC § 41(d)(1)(B)(i) | The process of experimentation utilized to discover the requisite information must fundamentally rely on principles of the “hard sciences” (physical, biological, engineering, or computer science)[cite: 1]. |

| 3. The Business Component Test | IRC § 41(d)(1)(B)(ii) | The research activities must be undertaken for the primary purpose of discovering information intended to be useful in the development of a new or improved business component (product, process, software, technique, formula, or invention)[cite: 1]. |

| 4. The Process of Experimentation Test | IRC § 41(d)(1)(C) | Substantially all (80% or more) of the research activities must constitute elements of a rigorous process of experimentation for a qualified purpose[cite: 1]. |

When analyzing eligibility, if the overall business component as a whole fails the four-part test, Treasury Regulations provide for a “Shrink-Back Rule”[cite: 1]. This rule permits the taxpayer to systematically apply the four-part test to the next most significant subset[cite: 1]. Furthermore, Internal Use Software (IUS) must meet a stringent three-part “High Threshold of Innovation Test”[cite: 1].

Classification of Qualified Research Expenses (QREs)

Under the provisions of IRC Section 41(b), taxpayers are restricted to claiming specific financial expenditures directly linked to performing qualified research activities[cite: 1]. The code categorizes these expenditures strictly into In-House Research Expenses and Contract Research Expenses[cite: 1].

In-House Research Expenses include W-2 taxable wages paid to employees for performing qualified services (directly engaging in, directly supervising, or directly supporting), cost of supplies (tangible property used or consumed), and computer rental/cloud computing costs[cite: 1]. Contract Research Expenses generally allow the taxpayer to claim exactly 65% of any expense paid to a third-party domestic contractor[cite: 1]. If the contractor is a “qualified research consortium,” the percentage increases to 75%[cite: 1].

Federal Case Law and Regulatory Enforcement Standards

The interpretation of the statutory four-part test has been the subject of extensive litigation[cite: 1]. A highly consequential recent development is the 2023 ruling in Little Sandy Coal Company, Inc. v. Commissioner of Internal Revenue, which established a rigorous evidentiary standard for the “substantially all” rule[cite: 1]. The appellate court provided a taxpayer-favorable clarification that costs associated with “direct support” and “direct supervision” do legally qualify for the calculation, provided they qualify as deductible research expenses under IRC Section 174[cite: 1].

This ruling underscores the necessity for contemporaneous documentation in defending R&D credit claims[cite: 1]. Taxpayers must implement recordkeeping systems that capture detailed time-tracking, laboratory notes, and evidence of technological uncertainty[cite: 1]. To alleviate auditing burdens, the IRS LB&I division provides the ASC 730 Directive as an administrative safe harbor for certain R&D costs[cite: 1].

Part III: Detailed Analysis of California State R&D Tax Credit Laws

The State of California, under Revenue and Taxation Code (RTC) Sections 17052.12 and 23609, offers a robust state-level incentive for innovation[cite: 1]. While it heavily conforms to federal definitions, it contains distinct geographic and calculative nuances[cite: 1].

Geographic Constraints and Standard Calculations

The most fundamental deviation is the strict geographic constraint: qualified research expenses must be physically incurred for activities conducted strictly within the borders of the State of California[cite: 1]. Under the Regular Method, California provides a 15% credit rate applied to qualified expenses that exceed a calculated base amount[cite: 1]. Unused California R&D credits may be carried forward indefinitely[cite: 1].

The Senate Bill 711 Overhaul (Effective January 1, 2025)

In October 2025, the California legislature enacted Senate Bill 711 (SB 711), representing a profound modernization of the state’s R&D tax credit infrastructure[cite: 1]. This legislation officially repealed the Alternative Incremental Credit (AIC) and formally adopted a modified version of the Alternative Simplified Credit (ASC) for taxable years beginning on or after January 1, 2025[cite: 1].

California also executed a strategic decoupling from the federal changes to IRC Section 174[cite: 1]. Unlike the federal requirement to capitalize and amortize R&D expenses, California, through SB 711, explicitly allows for full immediate expensing[cite: 1].

| Tax Code Feature | Federal Treatment (IRC § 174) | California Treatment (SB 711) | Economic Impact & Strategy |

|---|---|---|---|

| Domestic R&D Expense Timing | Must be capitalized and amortized over a 5-year period[cite: 1]. | Full immediate expensing is allowed in the year costs are incurred[cite: 1]. | California provides superior immediate cash flow[cite: 1]. |

| Foreign R&D Expense Timing | Must be capitalized and amortized over a 15-year period[cite: 1]. | Fully deductible in the current year[cite: 1]. | Encourages global operations without a severe state tax drag[cite: 1]. |

California Case Law and FTB Enforcement Rigor

The California Franchise Tax Board (FTB) and the California Office of Tax Appeals (OTA) maintain an aggressively strict interpretation of requirements[cite: 1]. In the Appeal of First Solar, Inc. (2023), the OTA ruled that high-level financial statements and patent lists are legally insufficient; taxpayers must provide granular, nexus-driven documentation[cite: 1]. Similarly, in the Appeal of Swat-Fame, Inc. (2020), the OTA established a severe interpretation of the “process of experimentation” test, mandate that creative sectors must prove research involves systematic resolution of objective technological uncertainty[cite: 1].

Part IV: The Los Angeles City Business Tax Exemption

Businesses operating within the municipality of Los Angeles must navigate the Los Angeles City Business Tax (LACBT), a gross receipts tax[cite: 1]. However, the City provides a critical lifeline through the Small Business Exemption (SBE), codified under LAMC Section 21.29[cite: 1]. A small business whose total worldwide gross receipts do not exceed $100,000 annually is fully exempt[cite: 1]. A parallel Creative Artist Exemption exists with a higher threshold of $300,000[cite: 1].

To qualify, a business must formally register for a Business Tax Registration Certificate (BTRC) and submit a timely annual renewal statement, typically due by the end of February[cite: 1]. Failure to file timely results in revocation of the exemption and liability for the tax plus penalties[cite: 1]. For businesses that have inadvertently established nexus without registering, the City offers a Voluntary Disclosure Agreement (VDA) program[cite: 1].

Final Thoughts

The Research and Development tax credit remains one of the most potent, yet highly scrutinized and fiercely litigated, economic incentives available to United States taxpayers[cite: 1]. For businesses operating within the vast economic engine of Los Angeles, the interplay between the rigid federal IRC Section 41 framework and the distinct California state provisions presents formidable compliance challenges[cite: 1]. Taxpayers must navigate the exacting documentation standards established by recent federal and state case law, such as Little Sandy Coal and Swat-Fame, which demand unprecedented granularity in tracking experimental activities and substantiating technological uncertainty[cite: 1].

However, the recent enactment of California Senate Bill 711 introduces an unprecedented era of strategic tax planning opportunity[cite: 1]. By adopting the Alternative Simplified Credit and, most critically, executing a deliberate legislative break from the restrictive federal Section 174 capitalization requirements, California has radically enhanced the immediate cash-flow benefits of conducting domestic R&D[cite: 1]. Los Angeles enterprises that systematically align their daily engineering workflows with these rigorous tax substantiation protocols can significantly reduce their long-term tax liabilities, ensuring the region continues its century-long legacy as a global epicenter of industrial innovation[cite: 1].

The information in this study is current as of the date of publication, and is provided for information purposes only[cite: 1]. Although we do our absolute best in our attempts to avoid errors, we cannot guarantee that errors are not present in this study[cite: 1]. Please contact a Swanson Reed member of staff, or seek independent legal advice to further understand how this information applies to your circumstances[cite: 1].

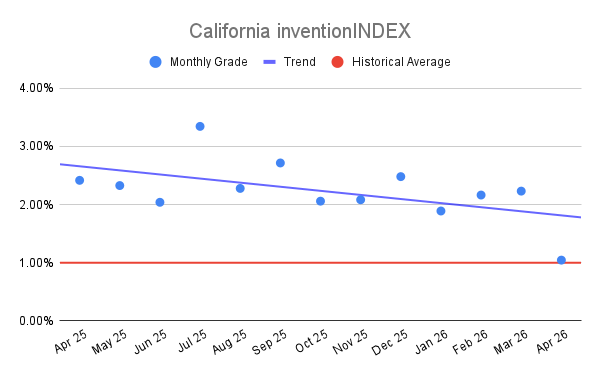

California inventionINDEX April 2026:[...]

California inventionINDEX April 2026:[...]