The United States federal and Utah State Research and Development (R&D) Tax Credits require businesses to satisfy a strict four-part test for their innovation activities: the research must have a permitted purpose, seek to eliminate technical uncertainty, involve a process of experimentation, and be fundamentally technological in nature. Specifically for Utah, eligible research expenses must be physically localized within the state to capture its unique three-tiered incentive structure (Incremental, Basic Research, and Volume Credits). Recent legislative overhauls permanently restored immediate expensing for domestic R&D, making localized innovation in hubs like Salt Lake City highly beneficial for corporate tax strategy.

This comprehensive study analyzes the United States federal and Utah state Research and Development (R&D) tax credit frameworks, exploring their statutory requirements, recent legislative changes, and governing case law. Through five detailed case studies, the analysis illustrates how specific industries developed in Salt Lake City, Utah, and how their localized innovation activities satisfy the stringent eligibility criteria for these lucrative tax incentives.

Industry Case Studies: The Historical Development and R&D Landscape of Salt Lake City

Salt Lake City, Utah, has undergone a profound economic transformation over the past century. Historically reliant on agriculture, mining, and unique local enterprises such as brine shrimp harvesting, the region has deliberately evolved into a highly diversified, technologically advanced innovation hub. In the mid-1980s, Utah suffered from the third-lowest gross domestic product per capita in the United States, prompting state leaders to actively pivot toward high-technology industries to foster wealth and raise average wages. This strategic shift, combined with the state’s geographic advantages, low operational costs, and highly educated workforce, birthed several prominent industries. The following five case studies detail the historical development of these sectors within Salt Lake City and demonstrate how their modern activities align with federal and state R&D tax credit requirements.

Case Study: The Software and Technology Sector (Silicon Slopes)

The emergence of the “Silicon Slopes”—a colloquialism for the technology corridor stretching across the Wasatch Front, including Salt Lake City and Provo—is deeply rooted in early governmental and academic technological infrastructure. The foundational framework for this industry was laid in the late 1960s when the University of Utah became the fourth node of the ARPANET, the military-funded precursor to the modern internet. This early, federally subsidized involvement in computer science fostered an academic culture that birthed pioneer technology companies in the subsequent decades. While early innovation in the state dates back to the 1950s, the modern software industry truly began to coalesce in the 1980s and 1990s with the rise of legacy firms such as WordPerfect and Novell, alongside the foundational work of University of Utah graduates who contributed to the creation of Atari and Pixar.

As the internet evolved into a commercial business platform, a second wave of Utah companies emerged, laying the groundwork for a highly skilled, internet-savvy local workforce. Companies such as Omniture, which eventually sold to Adobe for $1.8 billion, served as anchor institutions that attracted significant venture capital to the region. Today, Salt Lake City is frequently characterized as the “Cloud Capital,” driven by a confluence of economic and demographic factors. The state offers a flat 5 percent corporate tax rate, a cost of living substantially lower than coastal tech hubs like Seattle or the San Francisco Bay Area, and an efficient commuter rail system connecting the metropolitan area. Furthermore, local universities produce a steady stream of graduates in engineering and computer science, fueling an industry that now employs approximately one in seven Utahns and accounts for a massive share of the state’s private-sector wage growth.

For a Salt Lake City-based cloud computing firm developing a novel big data analytics platform, the activities undertaken by its software engineers present a classic example of qualifying research under both federal and state tax credit laws. The development process must satisfy the four-part test established under Internal Revenue Code (IRC) Section 41. The project exhibits a permitted purpose by seeking to create a novel algorithm designed to increase the processing speed and reduce the latency of unstructured data arrays, thereby improving the performance and function of the business component. At the project’s inception, technical uncertainty exists regarding whether the proposed cloud architecture can handle the specific load-balancing requirements without resulting in unacceptable system degradation.

To eliminate this uncertainty, the software engineers must engage in a systematic process of experimentation. This involves an iterative cycle of writing code, running load simulations, identifying architectural bottlenecks, and refactoring the codebase until the latency parameters are successfully achieved. Finally, the activities fundamentally rely on the principles of computer science, satisfying the technological in nature requirement. The wages paid to the software developers operating within the Salt Lake City headquarters qualify as in-house research expenses for the federal credit. Furthermore, because the research is conducted physically within the state, the company can claim the Utah state R&D tax credit, potentially capturing the 7.5 percent volume credit on these localized wages, provided the expenditures exceed the calculated base amounts required by the state statutes.

Case Study: The Life Sciences and Medical Device Sector (BioHive)

The life sciences and healthcare innovation sector in Salt Lake City has experienced robust, exponential growth, recently formalizing its identity under the branding initiative known as the “BioHive”. According to comprehensive economic impact studies conducted by the Kem C. Gardner Policy Institute at the University of Utah, the life sciences industry generated an estimated $5.8 billion in Gross Domestic Product (GDP) in 2023, representing 5.1 percent of Salt Lake County’s total GDP. The sector is a powerful engine of economic growth, adding jobs at an average annual rate of 4.5 percent from 2018 to 2023, far exceeding the 2.1 percent growth rate of other industries in the county, and now boasting over 41,000 localized jobs.

The historical development of this industry is tied directly to the pioneering medical research conducted at local academic institutions, which fostered early global innovations in artificial organs, genetics, and personalized medicine. Over time, these academic breakthroughs spun off into commercial enterprises, creating a dense ecosystem of research and testing laboratories, medical device and diagnostics manufacturers, and pharmaceutical distributors. Today, Salt Lake City hosts major manufacturing facilities for global healthcare leaders, including Edwards Lifesciences, Merit Medical Systems, Fresenius USA Manufacturing, and Becton Dickinson. The BioHive initiative itself originated as a grassroots, public-private partnership driven by private industry CEOs and supported by entities such as the Governor’s Office of Economic Opportunity (GOED) and BioUtah, with the explicit mission of elevating the state’s profile to garner investment and attract specialized talent.

A medical device manufacturer located in Salt Lake City that is engaged in the development of a novel disposable catheter for interventional pediatric cardiology exemplifies the type of entity eligible for substantial R&D tax credits. The creation of a new catheter designed with improved flexibility, a narrower profile, and enhanced biocompatibility strictly meets the permitted purpose requirement of developing a new or improved product. Technical uncertainty is inherently present at the outset, as it is unknown whether a newly synthesized polymer blend can withstand the required tensile strength without fracturing or causing vascular trauma during insertion.

The engineering and material science teams must undergo a rigorous process of experimentation to resolve this uncertainty. This process involves formulating multiple prototype batches utilizing varying polymer ratios, subjecting them to simulated vascular pathway testing and extreme tensile stress evaluations, and iteratively altering the chemical formula based on the empirical failure rates observed during testing. This systematic evaluation of alternatives relies fundamentally on the principles of biology, material science, and mechanical engineering. The expenditures associated with the clinical trial testing, the raw materials consumed during the iterative prototyping phases, and the wages of the research staff located in Salt Lake County all constitute qualified research expenses. If the manufacturer contracts with a local institution, such as the University of Utah, to perform highly specialized basic structural testing, those payments could additionally qualify for the Utah state 5 percent basic research credit, further compounding the financial benefit of localizing the R&D operations.

Case Study: Aerospace and Advanced Materials Manufacturing

Utah’s national prominence in the aerospace and advanced materials manufacturing sector is a direct legacy of the Cold War and the mid-century space race, fundamentally altering the industrial landscape of the Salt Lake City metropolitan area. The historical trajectory of this industry originates with explosive manufacturing companies, specifically the Hercules Powder Company. Formed originally as a result of a court-ordered breakup of the DuPont monopoly, Hercules established the Bacchus Works in Magna, Utah, situated just outside of Salt Lake City. As the military and industrial demand for dynamite and TNT shifted toward a requirement for solid rocket propellants, Hercules diversified its operations in 1959 into rocket propulsion systems.

This strategic pivot necessitated the development of products that were significantly lighter and stronger than traditional metals to construct strategic missile motors and spacecraft components. Consequently, Hercules became a pioneer in the development of carbon fiber, composite structures, and filament windings. Over the ensuing decades, this expertise compounded. Hercules’ aerospace division eventually merged with Thiokol to form Orbital ATK, which was later acquired by Northrop Grumman, solidifying a massive defense contracting presence in the state. Today, Utah is considered an epicenter for composite manufacturing, supported by organizations like the Utah Advanced Materials and Manufacturing Initiative (UAMMI), which fosters public-private partnerships to advance 3D printing and additive manufacturing technologies. The region now hosts critical fabrication facilities for industry giants such as Boeing, which manufactures composite structures for the 787 Dreamliner, and Hexcel, a producer of carbon fiber prepregs.

An aerospace defense contractor operating in Salt Lake City that collaborates with UAMMI to develop 3D-printed carbon fiber replacement parts for military aircraft engages in highly specialized, credit-eligible research. For example, the utilization of Composite-Based Additive Manufacturing (CBAM) technology to print an aircraft instrumentation bracket meets the permitted purpose of developing a new manufacturing process. Uncertainty exists regarding whether a thermoplastic carbon fiber matrix, printed layer-by-layer, can meet the precise thermal tolerance, fire retardancy, and load-bearing requirements of the legacy metal part it is intended to replace.

To eliminate this uncertainty, the engineering team must conduct a series of additive manufacturing print runs, systematically altering the microstructural orientation and stereolithography parameters of the material. The resulting prototypes are then subjected to rigorous evaluations, such as the Fire, Smoke, and Toxicity tests required by aviation research laboratories. The engineers evaluate the empirical data from these tests and adjust the digital print parameters accordingly to mitigate structural weaknesses. This iterative process fundamentally relies on the hard sciences of material science, chemical engineering, and advanced physics. The costs of the carbon fiber resins consumed and destroyed during the failed print runs, alongside the wages of the engineers overseeing the testing, qualify as R&D supplies and in-house labor under both the IRC Section 41 federal statutes and the localized Utah Code § 59-7-612 state statutes.

Case Study: The Outdoor Products Manufacturing Industry

The geographic positioning of Salt Lake City, situated at the foothills of the rugged Wasatch Mountain Range, has cultivated a unique and highly specialized industrial cluster: outdoor products manufacturing. The historical roots of this sector are intimately tied to the military operations of World War II, specifically the 10th Mountain Division. This U.S. Army light infantry unit was trained extensively in mountain warfare and winter survival tactics at Camp Hale, utilizing cumbersome 90-pound packs and seven-foot-long wooden skis equipped with thick cable bindings. Following the conclusion of the war, veterans of this specialized division returned to the Rocky Mountains, pouring their distinct expertise into the evolving civilian ski industry and heavily influencing the initial innovation of alpine equipment.

Decades later, Utah proactively capitalized on its geographic and historical advantages. In 2013, the state government became the first in the nation to create an official Office of Outdoor Recreation, a codified legislative body dedicated to coordinating outdoor recreation policy and promoting the associated manufacturing industry. The state’s four-season climate and immediate access to diverse, extreme terrains provide an ideal, localized proving ground for product research and development. Today, the region is home to hundreds of outdoor product brands, including specialized equipment manufacturers like Black Diamond Equipment, socially conscious Benefit Corporations like Cotopaxi, innovative board makers like Niche Snowboards, and massive fitness equipment developers like ICON Health & Fitness (iFIT). These companies leverage the state’s skilled workforce, pro-business environment, and low regulatory burdens to design, manufacture, and empirically field-test innovative gear.

An outdoor equipment manufacturer based in Salt Lake City that is designing a new, environmentally sustainable, high-altitude mountaineering tent can claim the R&D tax credit for its rigorous design and testing phases. The permitted purpose is established by the intent to develop a new product featuring improved aerodynamic wind resistance and reduced overall weight, utilizing novel, recycled, non-toxic polymer resins. Substantial technical uncertainty exists regarding the structural integrity of this newly formulated recycled fabric, specifically whether it will tear or fail when exposed to extreme shear winds and sub-zero temperatures prevalent in alpine environments.

The process of experimentation involves the company designing multiple aerodynamic profiles utilizing computer-aided design (CAD) modeling, constructing physical pilot models of the tents, and testing them systematically in controlled wind tunnels and field environments within the Wasatch range. The engineers observe the structural failure points, document the stress tolerances, and iteratively alter the geometric configuration of the support poles and the tension dynamics of the fabric based on the resulting data. Because this design process relies on the physical sciences, aerodynamics, and mechanical engineering, it satisfies the technological in nature requirement. Following judicial precedents that mandate the evaluation of alternative designs, the creation of these physical pilot models for structural testing qualifies the associated material and labor costs for the federal and state tax credits, provided the testing is systematically documented to resolve technical uncertainty rather than merely relying on aesthetic, cosmetic, or seasonal design choices.

Case Study: Industrial Engineering and Custom Manufacturing

The industrial engineering and custom manufacturing sector in Salt Lake City evolved initially to support the heavy infrastructure requirements of the state’s vast natural resource extraction, mining, and agricultural industries. As environmental regulations became increasingly stringent over the decades, and as resource extraction required more sophisticated, automated infrastructure, local machine shops and metal fabricators were forced to transition into highly specialized engineering and advanced manufacturing firms. The state facilitated this transition through educational alignments, supported by organizations such as the Utah Manufacturers Association (UMA) and the MEP Utah Chapter housed at the University of Utah, which assist manufacturers with technology deployment and skill development.

Today, Salt Lake City boasts exceptionally high employment concentrations of machinery maintenance workers, operations managers, and computer numerically controlled (CNC) tool operators. Companies operating within this space, ranging from automated wastewater treatment providers to complex structural steel fabricators, routinely undertake massive, multi-stage developmental projects to solve highly specific, unprecedented environmental and infrastructural challenges.

Consider a prominent Salt Lake City environmental engineering firm tasked with designing a novel, automated wastewater soil treatment system for a local industrial plant. This project entails highly qualified research activities, provided the contractual frameworks are structured correctly. The permitted purpose is the development of a custom, improved water treatment process designed to drastically increase heavy metal filtration efficiency. Technical uncertainty is present regarding the correct sequence of filtration media and the specific fluid flow rates required to prevent system clogging while processing a unique, highly viscous industrial sludge composition.

To eliminate this uncertainty, the firm’s engineers must conduct iterative fluid dynamics modeling and construct a scaled-down pilot system to empirically test various filtration sequences. They continuously evaluate the chemical effluent output levels and refine the mechanical pump designs based on the gathered data, relying entirely on the hard sciences of fluid dynamics, chemistry, and mechanical engineering. To successfully claim the federal and state R&D credits for this project, the firm must carefully navigate the “funding exception” inherent in contract research. The contract with the industrial plant must strictly stipulate that the engineering firm bears the financial risk of failure—typically achieved through a fixed-price contract rather than a time-and-materials arrangement without a performance guarantee—and that the firm retains substantial rights to the underlying technology, methodologies, or designs developed during the project. If these legal criteria are met, the extensive employee time allocated to researching, developing, and testing the innovative methods qualifies for lucrative tax credits.

The Federal Research and Development Tax Credit Framework

The United States federal Research and Development tax credit, codified under IRC Section 41, is a premier legislative tool designed to incentivize businesses to maintain and expand their investments in domestic innovation and technological advancement. For corporate entities and pass-through businesses operating in Salt Lake City, navigating the intricate intersection of these federal requirements, recent legislative overhauls, and local economic drivers is absolutely paramount for optimizing long-term tax positions.

The Four-Part Test for Qualified Research Activities

To legally qualify for the federal R&D tax credit, a taxpayer bears the burden of establishing that the specific research activities being performed meet all four criteria of the statutory test outlined in IRC Section 41(d). Crucially, these tests must be applied separately to each individual “business component”—which the tax code defines comprehensively as any product, process, computer software, technique, formula, or invention that is held for sale, lease, or license, or used by the taxpayer in their trade or business.

| Test Component | Statutory Requirement | Evidentiary Standard and Application |

|---|---|---|

| Permitted Purpose | The research must relate to a new or improved function, performance, reliability, or quality of a business component. | The taxpayer must maintain documentation demonstrating the intended improvement. Research related solely to style, taste, cosmetic, or seasonal design factors is explicitly excluded by statute. |

| Elimination of Uncertainty | The research must be undertaken to discover information that would eliminate uncertainty concerning the capability, method, or appropriate design of the business component. | The taxpayer must provide evidence showing that genuine technical uncertainty existed at the project’s inception. The performance of routine data collection or standard calculations based on historical data does not qualify as uncertainty. |

| Process of Experimentation | Substantially all of the activities must constitute elements of a process of experimentation relating to a new or improved function, performance, reliability, or quality. | The taxpayer must demonstrate an iterative process, such as systemic modeling, simulation, systematic trial and error, or the formulation and evaluation of multiple alternatives to resolve the established uncertainty. |

| Technological in Nature | The process of experimentation must fundamentally rely on principles of the physical or biological sciences, engineering, or computer science. | The research methodology must align strictly with hard science principles, as opposed to economics, humanities, psychological concepts, or social sciences. |

Qualified Research Expenses (QREs) and Base Amount Calculations

Under the provisions of IRC Section 41(b), the financial value of the credit is calculated based on “qualified research expenses” (QREs). These expenses primarily consist of in-house research expenses, which include the taxable wages paid to employees directly conducting, supporting, or supervising the research, as well as the tangible supplies consumed or destroyed during the experimental process. Additionally, the code permits the inclusion of contract research expenses, though these are typically statutorily limited to 65 percent of the amounts paid to third-party contractors, or 75 percent if the amounts are paid to a qualified research consortium (defined as a tax-exempt organization organized primarily to conduct scientific research).

The calculation of the final credit amount relies heavily on a taxpayer’s historical R&D spending patterns and their gross receipts. The standard credit amount is generally equal to 20 percent of the excess of the qualified research expenses for the current taxable year over a calculated “base amount”. Under Section 41(c), the base amount is defined as the product of the taxpayer’s historical “fixed-base percentage” and the average annual gross receipts of the taxpayer for the four taxable years immediately preceding the credit year. Recognizing the complexity of tracking historical data dating back to the 1980s for the fixed-base percentage, Congress allows taxpayers to elect the Alternative Simplified Credit (ASC) method. The ASC method simplifies the calculation, determining the credit as 14 percent of the QREs that exceed 50 percent of the average QREs for the three preceding taxable years.

The Impact of IRC Section 174 and the 2025 Legislative Overhaul

The treatment of R&D expenses under IRC Section 174 is inextricably linked to the utilization of the Section 41 tax credit. The Tax Cuts and Jobs Act (TCJA) of 2017 enacted a deeply controversial provision mandating that, for tax years beginning after December 31, 2021, all domestic specified research or experimental (SRE) expenditures must be capitalized and amortized over a five-year period, rather than being deducted immediately in the year incurred. This capitalization requirement fundamentally altered corporate financial planning across the country, creating immense complexities regarding book-tax differences, deferred tax assets, and effective corporate tax rates.

However, the legislative and financial landscape was dramatically reshaped by the passage of the “One Big Beautiful Bill Act” (OBBBA) in 2025 (P.L. 119-21). This sweeping tax reform legislation enacted a new IRC Section 174A, which permanently restores the ability of taxpayers to fully expense domestic research or experimental expenditures in the year they are incurred, effective for taxable years beginning after December 31, 2024. Notably, the legislation maintained a distinct geographic disparity: foreign R&E expenditures must still be capitalized and amortized over a 15-year period.

The 2025 legislation, alongside the procedural guidance released by the IRS in Revenue Procedure 2025-28, introduced critical transition rules and retroactive opportunities that demand immediate strategic attention. Small business taxpayers—statutorily defined under Section 448(c) as non-tax shelter entities with average annual gross receipts of $31 million or less over the prior three years—are granted the exceptional permission to apply this change retroactively to taxable years beginning after December 31, 2021. This retroactive application presents massive opportunities for filing amended returns or administrative adjustment requests to secure potential cash refunds for taxes paid during the amortization period.

Alternatively, taxpayers who properly capitalized domestic SRE expenditures between 2022 and 2024 may elect to accelerate the remaining unamortized deductions for such expenditures over a one-year or two-year period beginning in 2025, providing vital flexibility in managing taxable income and optimizing cash flow. The differing tax treatments of domestic versus foreign R&E expenditures under this current framework are expected to prompt multinational taxpayers to fundamentally reassess their research locations as part of broader tax planning strategies, potentially driving more centralized R&D operations back into domestic innovation hubs like Salt Lake City to capitalize on immediate expensing.

Utah State Research and Development Tax Credit Mechanics

To aggressively complement the federal incentive and attract high-technology firms, the State of Utah offers a permanent, non-expiring Research and Development Tax Credit designed explicitly to promote localized innovation. Administered under Utah Code § 59-7-612 for corporate franchise taxes and § 59-10-1012 for pass-through entities, estates, and individuals, the state credit aligns almost identically with the federal IRC Section 41 definition of qualifying research expenditures. However, it contains one critical, defining caveat: only expenses incurred for research physically conducted within the geographical boundaries of Utah are eligible to be captured toward the credit. Furthermore, for the purpose of calculating the base amount necessary for the credit formula, the gross receipts utilized in the calculation are strictly limited to those gross receipts attributable to sources within Utah, rather than global or national receipts.

The Three-Tiered State Credit Structure

The Utah R&D tax credit is distinctively and generously structured into three separate, stackable components, allowing innovative taxpayers to aggregate their state-level benefits:

| Credit Component | Statutory Calculation | Description and Application |

|---|---|---|

| Incremental Credit | 5 Percent | A credit equal to 5 percent of the taxpayer’s qualified research expenses incurred specifically within Utah that exceed the calculated base amount for the taxable year. |

| Basic Research Credit | 5 Percent | A credit equal to 5 percent of payments made to qualified organizations (such as Utah-based universities or scientific research institutes) for basic research conducted in Utah that exceed the base amount. |

| Volume Credit | 7.5 Percent | A credit equal to 7.5 percent of the taxpayer’s total qualified research expenses incurred in Utah for the current taxable year, functioning independently of the base amount excess. |

Carryforward Provisions and Strategic Prioritization

While the Utah R&D tax credit is inherently nonrefundable, the state statutes provide specific, complex carryforward rules that necessitate highly strategic tax planning on the part of corporate controllers and CPAs. Credits calculated under the 5 percent incremental and 5 percent basic research provisions that exceed a taxpayer’s current-year corporate franchise or income tax liability may be carried forward for a period not to exceed the next 14 taxable years. Conversely, the statutes explicitly dictate that these credits may not be carried back to preceding taxable years under any circumstances.

Crucially, the 7.5 percent volume credit does not possess any carryforward provision whatsoever; it acts entirely as a “use it or lose it” benefit strictly confined to the current taxable year. This statutory nuance dictates a very specific, mandatory ordering rule for tax professionals managing liabilities in Salt Lake City. Taxpayers must ensure their internal accounting software and external tax preparers prioritize the consumption of the 7.5 percent volume credit against their current Utah tax liability before applying any of the 14-year carryforward credits generated by the incremental or basic research components, thereby maximizing the total economic benefit of the state credits over time.

Administrative Guidance and Apportionment Rule R865-6F

The Utah State Tax Commission (USTC) provides comprehensive administrative guidance regarding the application of these credits through Administrative Rule R865-6F. For multi-state or multinational entities operating as part of a unitary business group, Rule R865-6F-32 strictly dictates that the apportionment data of all members of the unitary group must be included in calculating a single apportionment fraction for the group. The numerators and denominators of the property, payroll, and receipts factors of all integrated institutions must be mathematically combined. This complex accounting requirement ensures that massive corporations accurately and legally allocate their Utah-sourced gross receipts when establishing the baseline base amount for the state R&D credit, preventing the dilution of the credit through out-of-state revenue.

An additional, significant administrative nuance of the Utah system is the complete lack of an official standalone form or worksheet provided by the USTC for calculating the research credit. Unlike the federal system, which relies on the standardized Form 6765, the USTC instructions for the corporate franchise tax return (TC-20) and individual income tax return (TC-40) simply state that the taxpayer must independently “keep all related documents with your records” to substantiate the claimed credit figure entered on the return. This administrative approach places a substantially heightened burden of proof directly on the taxpayer, making granular, contemporaneous documentation an absolute legal necessity in the event of a state audit.

Pertinent Case Law and Tax Administration Rulings

The interpretation and application of both federal and state R&D tax credit statutes rely heavily on evolving judicial precedent. Recent appellate and tax court cases have established incredibly strict boundaries regarding the substantiation of research activities, the definition of experimental processes, and the nature of contractual research agreements.

The Substantially All Test and the Process of Experimentation: Little Sandy Coal Co. v. Commissioner

The 2023 decision issued by the U.S. Court of Appeals for the Seventh Circuit in Little Sandy Coal Co. v. Commissioner represents a landmark judicial interpretation of the IRC Section 41 “substantially all” test. To legally qualify for the research credit, Section 41(d)(1)(C) mandates that “substantially all”—which is explicitly defined by Treasury Regulations as 80 percent or more—of the taxpayer’s research activities must constitute elements of a process of experimentation.

In the Little Sandy Coal case, the taxpayer, an industrial shipbuilding company, claimed massive R&D credits for the design and construction of custom vessels. The IRS audited the firm and denied the credits entirely, arguing the taxpayer failed to definitively prove that 80 percent of the labor activities were experimental in nature. The appellate court affirmed the IRS denial, noting critically that the taxpayer relied on an “all or nothing” strategy at the macro-project level. The court emphasized that the taxpayer failed to utilize the established “shrink-back rule” to identify specific, modular subcomponents of the ships that might have legally qualified, choosing instead to claim the entire vessel construction process. Furthermore, the appellate court firmly rejected the taxpayer’s argument that the sheer novelty of a business component is an acceptable heuristic for satisfying the substantially all test, ruling that the test must be applied strictly in reference to specific employee activities, not the physical elements or uniqueness of the final project.

However, the appellate court’s lengthy opinion contained a highly favorable and transformative element for corporate taxpayers: it explicitly rejected the lower Tax Court’s previous, restrictive assertion that the direct support and direct supervision of research could not be counted as elements of a process of experimentation. The higher court ruled definitively that wage costs associated with the direct support and direct supervision of research activities absolutely qualify for inclusion in both the numerator and the denominator of the 80 percent calculation fraction, provided that the costs in question qualify broadly as “research expenses” deductible under IRC Section 174. The core, actionable takeaway from Little Sandy Coal for Salt Lake City businesses is that taxpayers must maintain granular, contemporaneous time-tracking data at the subcomponent level, as relying on the general novelty of a project is a guaranteed path to audit failure.

The Funding Exception and Engineering Design Boundaries: Phoenix Design Group

In the case of Phoenix Design Group, Inc. v. Commissioner (PDG), the Tax Court directly addressed the credit eligibility of mechanical, electrical, and plumbing (MEP) engineering design activities. The court ruled entirely against the taxpayer, highlighting several critical, systemic failures in meeting the statutory four-part test.

Firstly, PDG attempted to rely on its standard, commercial six-stage development process as automatic evidence of a “process of experimentation.” The court firmly rejected this, determining that the firm’s process was strictly linear, routine, and did not involve the iterative testing, hypothesis formation, or evaluation of alternatives designed specifically to resolve technical uncertainty. The court held that performing routine engineering calculations based on widely available historical data does not constitute experimentation because the necessary information to complete the design was already known to the profession.

Secondly, the IRS frequently and aggressively utilizes the “funding exception” in engineering and contract research cases. This statutory exception excludes research from credit eligibility if the client’s payment to the taxpayer is not strictly contingent on the success of the research activities, or if the taxpayer does not retain substantial, exploitable rights to the research. While a separate case, Smith v. Commissioner, allowed an architectural firm to survive an IRS motion for summary judgment on the funding issue based on highly specific contractual terms, the PDG ruling serves as a stark warning. Salt Lake City engineering firms must carefully draft their client contracts to ensure they bear the financial risk of technical failure to preserve their eligibility for the credit.

Utah-Specific Tax Disputes and Private Letter Rulings

Within the specific jurisdiction of the District of Utah, cases such as Intermountain Electronics, Inc. v. United States highlight localized, ongoing disputes over federal tax refunds based on R&D credit claims. Adjudicated in Salt Lake City, these local district court cases underscore the absolute necessity for Utah-based manufacturers to rigorously apply the stringent documentation principles established in broader appellate rulings like Little Sandy Coal to survive IRS scrutiny.

Furthermore, the Utah State Tax Commission frequently issues Private Letter Rulings (PLRs) to clarify local taxability and regulatory boundaries for businesses. For instance, the USTC recently published proposed amendments to Rule R865-19S-92, officially clarifying that the sale, rental, or lease of custom computer software constitutes a sale of personal services and is definitively not subject to state sales and use tax, regardless of the form in which the software is purchased. Such rulings are profoundly critical for the massive software industry operating within the Silicon Slopes of Salt Lake City. These rulings delineate the precise boundaries between taxable tangible products and non-taxable custom development services, directly impacting the classification of gross receipts that must be utilized in the complex base amount calculation for the state R&D credit. Taxpayers may request these PLRs directly from the Commission to secure binding guidance on their specific, highly technical factual circumstances prior to claiming millions in credits.

The information in this study is current as of the date of publication, and is provided for information purposes only. Although we do our absolute best in our attempts to avoid errors, we cannot guarantee that errors are not present in this study. Please contact a Swanson Reed member of staff, or seek independent legal advice to further understand how this information applies to your circumstances.

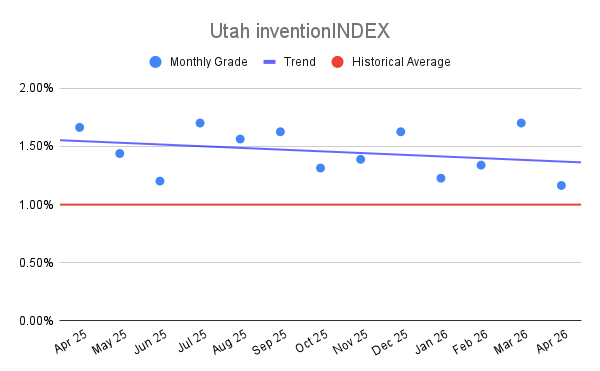

Utah inventionINDEX April 2026:

Utah inventionINDEX April 2026: