This study exhaustively analyzes the United States federal and Utah state Research and Development (R&D) tax credit frameworks, focusing on their strategic application within the industrial ecosystem of Taylorsville, Utah. Through detailed case studies, statutory analysis, and an examination of recent tax administration guidance and case law, it demonstrates how local enterprises navigate these complex legal requirements to subsidize innovation.

Industry Case Studies and Economic Development in Taylorsville, Utah

The economic and industrial landscape of Taylorsville, Utah, is the result of a unique convergence of geographic positioning, visionary private entrepreneurship, and strategic governmental policy. Incorporated on July 1, 1996, from the historic Taylorsville and Bennion communities, the municipality occupies a highly advantageous central location within the Salt Lake Valley, bordered by Interstate 215 and the Bangerter Highway. Historically characterized by its agricultural roots and subsequent mid-century suburban residential growth, Taylorsville has systematically transformed over the last half-century into a highly specialized hub for medical devices, life sciences, information technology, and financial services.

The transition from a bedroom community to a commercial powerhouse was heavily catalyzed by the establishment of the Sorenson Research Park. This high-technology business park was heavily influenced by the legacy of James LeVoy Sorenson, a prolific inventor who held over 50 patents for critical medical devices, including the disposable surgical mask and the single-use intravenous catheter. Sorenson utilized his vast capital and vision to foster a localized ecosystem of biomedical and technological innovation, which fundamentally altered the trajectory of Taylorsville’s commercial real estate and labor markets. Today, the Sorenson Research Park and the adjacent commercial corridors host major corporate entities, including Concentrix, ICU Medical, ALS Laboratories, Sorenson Communications, and Nelson Laboratories.

Furthermore, the recent consolidation of state government facilities—such as the massive $56 million relocation of hundreds of state employees to the former American Express campus in Taylorsville—has created a dense employment core that continues to attract ancillary technology, laboratory, and service providers. As these diverse industries expand within the city, their reliance on continuous technological advancement makes the United States federal Research and Development (R&D) tax credit, coupled with the State of Utah’s aggressive R&D tax incentives, a critical mechanism for subsidizing the high costs of innovation.

The following five case studies illustrate how specific industrial clusters developed in Taylorsville, Utah, and how these enterprises can strategically leverage both the federal and Utah state R&D tax credits.

Medical Device Testing and Regulatory Sciences

Industry Context and Historical Development: The medical device sector in Taylorsville traces its origins directly to the foundational work of James LeVoy Sorenson, who founded Sorenson Research Company in the region in 1972 to manufacture and market innovative medical instruments. His pioneering work in disposable medical devices birthed an entire ecosystem of ancillary manufacturing and laboratory testing within the Salt Lake Valley. As companies like Deseret Pharmaceutical (founded in 1956) grew, the necessity for independent, highly technical validation of biocompatibility and sterility created a massive demand for microbiological and analytical chemistry testing facilities. A prime example of this legacy in Taylorsville is Nelson Laboratories. Established in 1985 in a modest University of Utah lab, the company subsequently expanded into a massive global headquarters located in the heart of Taylorsville. Today, Nelson Laboratories employs hundreds of scientists locally, providing essential microbiology testing and consulting services for MedTech companies worldwide, solidifying Taylorsville’s reputation as a global regulatory science hub.

Hypothetical R&D Activity: A Taylorsville-based medical device testing laboratory embarks on a multi-year project to develop a novel mass spectrometry testing methodology. The goal is to isolate and quantify previously undetectable extractable and leachable (E&L) chemical compounds in a new class of bio-absorbable cardiovascular stents, which current testing protocols destroy during the solvent extraction phase.

Federal R&D Tax Credit Eligibility Analysis: To qualify for the federal R&D tax credit under IRC § 41, the laboratory’s activities must satisfy the four-part test:

- Permitted Purpose: The research aims to develop a new, highly sensitive analytical testing process (a qualifying business component under the statute) that improves the performance, reliability, and accuracy of cardiovascular device safety profiling.

- Elimination of Uncertainty: At the project’s outset, the laboratory faces technical uncertainty regarding the optimal solvent extraction methods, temperature gradients, and ionization techniques required to detect trace polymers without simultaneously destroying the bio-absorbable matrix of the stent.

- Process of Experimentation: The chemists systematically evaluate multiple solvent combinations, iterate thermal cycling parameters, and vary mass spectrometer calibration settings. They record structured data on degradation rates and signal-to-noise ratios, discarding failed protocols until the optimal, non-destructive testing methodology is established.

- Technological in Nature: The activity fundamentally relies on the hard sciences, specifically the principles of analytical chemistry and molecular biology.

The laboratory must carefully navigate the IRC § 41(d)(4)(D) exclusion for “routine testing or inspection for quality control.” While performing the finalized E&L test for a third-party client is a routine excluded activity, the extensive engineering and chemical research effort expended to develop the novel testing methodology itself is fully eligible for the credit.

Utah State R&D Tax Credit Application: To capture the Utah R&D tax credits under Utah Code Ann. § 59-7-612, the laboratory must geographically source its Qualified Research Expenses (QREs). The laboratory can isolate the W-2 box 1 wages of the analytical chemists performing the research in the Taylorsville facility, the cost of specialized reagent supplies consumed during the experimentation, and any contract research expenses paid to local universities. By doing so, the firm generates a high volume of Utah-specific QREs, allowing it to leverage the state’s nonrefundable 7.5% volume credit to offset current corporate franchise tax liabilities, while carrying forward any excess 5% incremental credits for up to 14 years.

Financial Technology (Fintech) and Data Architecture

Industry Context and Historical Development: Utah’s emergence as a dominant force in the Financial Technology (Fintech) sector is directly attributable to its unique regulatory environment, specifically its historical allowance of Industrial Loan Company (ILC) charters. The ILC charter, exempt from the federal Bank Holding Company Act of 1956, allowed non-traditional commercial entities to offer banking services. This regulatory framework drew massive corporate operations to the Salt Lake Valley. American Express established a major historic presence in the state, operating a massive customer service and financial back-office campus on a 31-acre parcel in Taylorsville. Although the state government recently purchased the physical American Express building, the decades of financial operations fostered a deeply entrenched, localized workforce highly skilled in financial systems, cryptography, secure data architecture, and payment processing. Financial transaction processors, such as InComm, continue to maintain a strong presence in the Taylorsville ecosystem.

Hypothetical R&D Activity: A Taylorsville-based financial transactions processing company develops a decentralized, blockchain-inspired ledger software system. The objective is to integrate legacy merchant transaction databases with real-time, cross-border currency exchange Application Programming Interfaces (APIs), aiming to securely reduce international settlement times from three days to under five seconds.

Federal R&D Tax Credit Eligibility Analysis:

- Permitted Purpose: The design and implementation of a new internal software architecture process to improve the speed, functionality, and reliability of global financial settlements.

- Elimination of Uncertainty: The software engineers face deep technological uncertainty regarding how to securely map disparate legacy data schemas into a unified, high-speed encrypted ledger without inducing data corruption or exposing cryptographic vulnerabilities during the API handshake process.

- Process of Experimentation: The engineering team creates isolated sandboxed testing environments, writing continuous integration scripts, executing millions of simulated high-volume transactions, and evaluating the database architecture against automated stress tests and penetration attempts, iterating the code to resolve integration failures.

- Technological in Nature: The project relies entirely on computer science, cryptographic principles, and network engineering.

Because this software primarily facilitates the company’s internal financial operations, it must be evaluated under the strict Internal Use Software (IUS) rules. To qualify under IUS regulations, the software must meet a high threshold of innovation, entail significant economic risk, and not be commercially available. Furthermore, as highlighted by federal case law regarding funded research (e.g., Meyer, Borgman & Johnson), if the Taylorsville entity is performing this research under contract for a third-party merchant network, the contracts must be meticulously structured to ensure the Taylorsville entity bears the financial risk of failure and retains substantial rights to the underlying intellectual property.

Utah State R&D Tax Credit Application: Assuming the IUS thresholds are met, the company can claim the wages of the Taylorsville-based data scientists and software architects under Utah Code Ann. § 59-7-612. Fintech companies heavily utilize cloud computing environments (e.g., AWS, Azure) to compile code and run simulations. While amounts paid for the right to use computers in the conduct of qualified research are eligible QREs federally, the company must ensure that the researchers initiating and directing those cloud-based experiments are physically located in Utah to maintain the state-level geographic nexus required for the 7.5% volume and 5% incremental credits.

Advanced Software and Business Process Outsourcing (BPO) Technology

Industry Context and Historical Development: Taylorsville’s demographic profile—characterized by a young, highly educated workforce, a high percentage of bilingual residents, and access to robust fiber-optic infrastructure—made it a prime location for the Business Process Outsourcing (BPO) and customer management industries. Companies like Convergys anchored massive operations in the area. Following the 2018 acquisition of Convergys by SYNNEX and its subsequent integration into Concentrix, the industry paradigm in Taylorsville shifted dramatically from human-capital-intensive call centers to technology-powered, AI-fueled customer experience (CX) platforms. Concentrix, a global leader in business transformation services with a significant footprint in the Sorenson Research Park, exemplifies this evolution, driving a localized engineering micro-economy focused on natural language processing, predictive analytics, and digital omnichannel integrations.

Hypothetical R&D Activity: A CX technology firm in Taylorsville engineers a proprietary Natural Language Processing (NLP) generative AI routing engine. This software is designed to intercept incoming customer audio streams in real-time, dynamically translate complex regional dialects, analyze customer sentiment, and automatically query internal technical databases to generate live, contextual text prompts for human agents.

Federal R&D Tax Credit Eligibility Analysis:

- Permitted Purpose: The development of a new software product to enhance the functionality and performance of omnichannel customer service routing.

- Elimination of Uncertainty: At the outset, data scientists are uncertain of the optimal machine learning parameters required to achieve sub-second latency in audio-to-text translation while maintaining high accuracy in sentiment analysis across heavily accented regional dialects.

- Process of Experimentation: The data science team trains the AI models on vast proprietary datasets, systematically adjusting algorithmic weights, modifying the neural network layers, and conducting automated A/B testing against human baselines to iteratively reduce the error rate of the sentiment routing.

- Technological in Nature: The activity fundamentally relies upon computer science and data engineering.

Unlike the fintech example, if this software is embedded into a platform that is licensed or sold to third-party clients, it avoids the heightened scrutiny of the Internal Use Software (IUS) exclusions. The firm can aggregate the W-2 wages of the software developers, UX/UI designers, and quality assurance testers engaged directly in the iterative coding process.

Utah State R&D Tax Credit Application: This software development activity represents a prime candidate for the Utah R&D tax credit. The wages paid to the Taylorsville-based engineering teams qualify as in-house research expenses incurred in the state. By utilizing the Utah ASC (Alternative Simplified Credit) equivalent or the standard incremental calculation, the firm can offset its Utah corporate franchise tax liability. This capital retention is vital for BPO firms transitioning into pure technology plays, as it allows them to reinvest tax savings directly into acquiring highly competitive AI engineering talent within the Salt Lake Valley market.

Telecommunications and Accessibility Engineering

Industry Context and Historical Development: Following the dot-com bubble burst in the early 2000s, local technology firms in the Taylorsville area were forced to pivot their vast digital infrastructure capabilities toward more sustainable, specialized markets. James Sorenson’s media company, heavily invested in video compression technology, recognized a profound, unmet need in serving the deaf and hard-of-hearing community. Leveraging the strong technological infrastructure of the Sorenson Research Park, the company evolved into Sorenson Communications, pioneering functionally equivalent Video Relay Services (VRS) and IP captioned telephone technologies. The presence of nearby educational anchors like Salt Lake Community College and the University of Utah provided a steady pipeline of software developers and telecommunications engineers, allowing this highly specialized accessibility tech sector to thrive uniquely in Taylorsville.

Hypothetical R&D Activity: A Taylorsville telecommunications hardware firm initiates an engineering project to design a new, proprietary IP-captioned telephone device. The objective is to develop a custom hardware-software interface that utilizes edge computing to process real-time speech-to-text algorithms locally on the device, rather than relying on cloud servers, to eliminate latency for hearing-impaired users in low-bandwidth rural environments.

Federal R&D Tax Credit Eligibility Analysis:

- Permitted Purpose: The development of a new physical hardware device and embedded software (business components) to improve the performance, speed, and reliability of accessibility communications.

- Elimination of Uncertainty: The hardware engineers face technical uncertainty regarding the thermal management of the edge-computing processors within the small form factor of a desktop telephone, as well as uncertainty regarding the optimization of the embedded C++ code to run on a low-power chipset without dropping frames.

- Process of Experimentation: The engineering team builds multiple physical prototypes using varying heat sink materials and processor architectures. They conduct thermal load testing, evaluate power draw, and iteratively rewrite the firmware to balance processing speed against thermal throttling, recording the failure points of each design iteration.

- Technological in Nature: The project relies on the principles of electrical engineering, thermodynamics, and computer science.

Utah State R&D Tax Credit Application: The development of physical hardware presents distinct advantages for generating QREs. In addition to the wages of the electrical and software engineers based in Taylorsville, the firm can claim the cost of the tangible supplies consumed during the prototyping phase. This includes custom printed circuit boards (PCBs), microprocessors, 3D printing resins, and testing materials that are consumed or destroyed during the experimental thermal testing. Because these supplies are physically utilized and exhausted within the Taylorsville facility, they contribute heavily to the Utah state QRE base, maximizing the 7.5% volume credit available under Utah Code Ann. § 59-7-612.

Advanced Life Sciences and Bio-Tissue Engineering

Industry Context and Historical Development: Taylorsville’s proximity to the University of Utah’s robust medical research ecosystem has organically expanded the city’s life science footprint. The legacy of James LeVoy Sorenson continues to permeate the region, notably through the Sorenson Molecular Biotechnology Building and the forthcoming James LeVoy Sorenson Center for Medical Innovation. These state-of-the-art facilities act as incubators, resulting in a proliferation of private life science spin-offs and enterprises settling within the Sorenson Research Park and adjacent Taylorsville industrial zones. The consolidation of state scientific resources, specifically the Unified State Laboratories located near the former American Express building, further anchors a highly specialized scientific talent pool in the immediate Taylorsville vicinity. This geographic clustering of public research and private capital has made Taylorsville a premier destination for bio-tissue engineering and therapeutic research.

Hypothetical R&D Activity: A privately funded biotechnology firm, spun out of a local university and headquartered in the Sorenson Research Park, conducts research to engineer a synthetic, bio-compatible hydrogel scaffolding intended to promote accelerated cellular vascularization and tissue regeneration in severe burn victims.

Federal R&D Tax Credit Eligibility Analysis:

- Permitted Purpose: Developing a new biological product and chemical formula intended to improve the performance and quality of clinical tissue healing.

- Elimination of Uncertainty: The bio-engineers face deep scientific uncertainty regarding the exact stoichiometric ratios of the polymer chains required to maintain structural integrity while allowing for cellular vascularization, as well as uncertainty regarding the degradation rate of the hydrogel in vivo.

- Process of Experimentation: The research team creates multiple chemical formulations of the hydrogel. They conduct systematic in vitro stress testing for tensile strength, followed by rigorous biological assays to measure cellular adhesion and proliferation rates. Formulations that fail to support vascularization or degrade too rapidly are discarded, and the chemical composition is systematically altered in successive experimental iterations.

- Technological in Nature: The research fundamentally relies on the principles of biology, organic chemistry, and materials engineering.

Utah State R&D Tax Credit Application: This scenario is the archetypal application of the R&D tax credit. The firm can claim the W-2 wages of the lead researchers, biological technicians, and lab assistants. Furthermore, the substantial costs of the tangible supplies consumed during the experimentation process—such as chemical reagents, biological media, disposable petri dishes, and synthetic polymer stock—are highly lucrative QREs. Because the firm is heavily investing in physical materials consumed within the Taylorsville laboratory, they generate a high volume of Utah-specific QREs. This allows them to fully exploit the nonrefundable 7.5% volume credit to offset current corporate franchise tax liabilities, while carrying forward the 5% incremental credits for up to 14 years to protect future revenues once the hydrogel achieves FDA approval and commercialization. If the firm contracts a portion of the cellular assay testing to the nearby University of Utah, 75% of those payments to a qualified research consortium can be included as QREs under federal and state law, further maximizing the tax benefit.

Detailed Analysis of the United States Federal R&D Tax Credit Framework

To fully contextualize the case studies presented above, a rigorous examination of the statutory, regulatory, and judicial frameworks governing the R&D tax credit is required. The federal Credit for Increasing Research Activities is codified under Section 41 of the Internal Revenue Code (IRC § 41). Originally enacted in 1981 to stimulate domestic economic growth, incentivize technological innovation, and prevent the offshoring of highly technical jobs, the credit was made permanent by the Protecting Americans from Tax Hikes (PATH) Act of 2015.

The credit operates as a dollar-for-dollar reduction of a taxpayer’s federal income tax liability, calculated as a percentage of the taxpayer’s Qualified Research Expenses (QREs) that exceed a statutorily defined base amount. The structural foundation of IRC § 41 is intrinsically linked to IRC § 174, which governs the accounting treatment and amortization of research and experimental (R&E) expenditures.

The Stringent Four-Part Test for Qualified Research

The IRS does not grant the R&D tax credit simply because a company employs engineers or operates in a high-technology sector. Taxpayers must rigorously demonstrate that the specific underlying activities meet the statutory definition of “qualified research.” Under IRC § 41(d) and the accompanying Treasury Regulations, an activity must satisfy all four elements of a stringent, cumulative test. Crucially, this test must be applied separately to each “business component”—defined as any product, process, computer software, technique, formula, or invention to be held for sale, lease, or license, or used by the taxpayer in a trade or business.

The Section 174 Test (Permitted Purpose) The foundational requirement is that the expenditures associated with the research must be eligible for treatment as R&E expenditures under IRC § 174. This means the research must be undertaken for the purpose of discovering information intended to eliminate uncertainty concerning the development or improvement of a product. Furthermore, the research must be undertaken for a “qualified purpose.” It must relate to a new or improved function, performance, reliability, or quality of the business component. The statute explicitly excludes research related to style, taste, cosmetic, or seasonal design factors.

The Discovering Technological Information Test The research must be undertaken for the purpose of discovering information that is “technological in nature”. The taxpayer must demonstrate that the process of experimentation fundamentally relies on principles of the hard sciences. The acceptable fields of science are strictly limited to physical sciences, biological sciences, computer science, or engineering. Reliance on economic principles, social sciences, humanities, or business management strategies will immediately disqualify the activity.

The Business Component Test The application of the discovered technological information must be intended to be useful in the development of a new or improved business component of the taxpayer. The IRS requires a direct nexus between the experimental activities and the specific business component being developed. If the overall project fails to meet the requirements, the regulations provide a “shrinking-back” rule, allowing the taxpayer to apply the four-part test to the next most significant subset of elements of the business component until a qualifying subset is identified.

The Process of Experimentation Test The final, and most heavily scrutinized, element requires that “substantially all” (defined by regulations as 80 percent or more) of the research activities must constitute elements of a process of experimentation. Treasury regulations articulate that a qualifying process of experimentation requires the taxpayer to:

- Identify the specific technological uncertainty regarding the business component;

- Identify one or more alternatives intended to eliminate that uncertainty; and

- Identify and conduct a structured process of evaluating the alternatives (e.g., through modeling, simulation, or systematic trial and error).

Identifying Qualified Research Expenses (QREs)

Once a taxpayer establishes that an activity satisfies the four-part test for a specific business component, they may aggregate the expenses directly associated with that activity. IRC § 41(b) strictly limits QREs to four distinct categories; any expense not explicitly set forth in this section cannot be claimed.

- Wages: This category includes taxable wages (as defined in IRC § 3401(a), generally W-2 Box 1 wages) paid or incurred to an employee for performing “qualified services.” Qualified services are not limited to the scientists conducting the actual experiments; they also include the direct supervision of the research (e.g., an engineering manager overseeing the project) and the direct support of the research (e.g., a laboratory technician cleaning equipment or a machinist fabricating a prototype). Fringe benefits and non-taxed income are excluded.

- Supplies: Amounts paid or incurred for tangible property used in the conduct of qualified research. This typically includes raw materials, chemical reagents, biological media, and prototype components that are consumed, destroyed, or heavily degraded during the testing process. The statute explicitly excludes land, improvements to land, and property subject to the allowance for depreciation.

- Contract Research Expenses: Recognizing that many firms outsource highly specialized testing, IRC § 41(b)(3) allows taxpayers to claim 65 percent of any amount paid or incurred to a third party (other than an employee) for the performance of qualified research on the taxpayer’s behalf. If the payment is made to a “qualified research consortium” (such as a tax-exempt university or scientific research organization), the allowable capture rate increases to 75 percent.

- Computer Rental/Cloud Hosting: Amounts paid to another person for the right to use computers in the conduct of qualified research. In the modern era, this frequently applies to cloud computing and server hosting costs (e.g., AWS, Azure) directly tied to software development, staging, and testing environments, provided the costs are strictly bifurcated from general administrative hosting.

Statutory Exclusions and “Funded Research”

IRC § 41(d)(4) enumerates specific activities that are categorically excluded from the definition of qualified research, regardless of whether they otherwise meet the four-part test. Notable exclusions include:

- Research after commercial production: Any research conducted after the business component has met its basic design specifications and is ready for commercial sale or use.

- Adaptation and Duplication: Activities related to adapting an existing product to a specific customer’s requirement, or reverse-engineering/duplicating an existing product.

- Surveys and Studies: Market research, efficiency surveys, management studies, and routine data collection.

- Foreign Research: Any research conducted outside the United States, the Commonwealth of Puerto Rico, or any possession of the United States.

The Funded Research Exclusion: The “funded research” exclusion is particularly critical, especially for engineering firms, defense contractors, and custom software developers in Taylorsville. Under Treasury Regulation § 1.41-4A(d), research is considered “funded”—and therefore entirely ineligible for the credit—if the taxpayer’s right to payment is not contingent on the success of the research, or if the taxpayer does not retain substantial rights in the results of the research. If a firm is paid an hourly rate (time and materials) regardless of whether the engineering project succeeds or fails, the IRS deems the client to bear the economic risk, meaning the performing firm cannot claim the R&D credit. Conversely, fixed-price contracts generally preserve the economic risk for the performing firm.

Administrative Enhancements: The New Form 6765

The IRS has significantly escalated its substantiation requirements for claiming the credit. Historically, taxpayers reported aggregated numerical data on Form 6765 (Credit for Increasing Research Activities). However, prompted by a high volume of unmeritorious claims, the IRS released a revised Form 6765, introducing Sections E, F, and G.

Effective voluntarily for tax year 2024 and strictly mandated for tax years beginning in 2025, taxpayers must provide extensive quantitative and qualitative information on a business-component basis. Taxpayers must identify the specific business components generating the QREs, explicitly state the technological uncertainties faced, detail the alternatives evaluated during the process of experimentation, and provide the exact breakdown of wages, supplies, and contract expenses tied to each individual component. This structural shift effectively forces taxpayers to present an audit-ready, highly granular defense narrative at the time of filing, significantly increasing the compliance burden for high-tech firms in Taylorsville.

Detailed Analysis of the Utah State R&D Tax Credit Laws

Recognizing the economic imperative of fostering an intra-state innovation economy, the Utah Legislature codified a highly competitive, permanent tax credit for increasing research activities within the state. The statutory authority is located in Utah Code Ann. § 59-7-612 for corporate franchise and income taxes, and § 59-10-1012 for individual and pass-through entity income taxes.

Alignment with Federal Definitions and the Geographic Nexus

Utah’s statutory framework is intentionally symbiotic with the federal tax code. Utah Code mandates that the definitions of “qualified research” and “qualified research expenses” are adopted directly from IRC § 41(d) and § 41(b). Consequently, an activity must satisfy the federal four-part test, and expenses must fall within the federal QRE categories, to be eligible at the state level.

However, Utah imposes a strict, uncompromising geographic limitation. Under Utah law, “qualified research” includes only qualified research conducted physically within the borders of the state, and “qualified research expenses” include only in-house and contract research expenses incurred within Utah. Furthermore, for the purposes of calculating base amounts, a taxpayer’s gross receipts include only those gross receipts attributable to sources within Utah. For a firm headquartered in Taylorsville with satellite offices in California, only the W-2 wages of the engineers physically working in the Taylorsville office, and the supplies physically consumed in Utah laboratories, may be included in the state calculation.

The Three-Component Calculation Structure

The Utah R&D tax credit is distinguished by its unique, multi-tiered structure, which combines both incremental and volume-based incentives to maximize taxpayer benefit. As outlined in Utah Code Ann. § 59-7-612(1)(a), the total nonrefundable credit is the sum of three distinct components:

| Component Type | Statutory Rate | Calculation Mechanism | Carryforward Provision |

|---|---|---|---|

| Incremental QREs | 5.0% | 5% of the taxpayer’s Utah-based QREs for the current taxable year that exceed the calculated Utah base amount. | Up to 14 consecutive taxable years. |

| Basic Research Payments | 5.0% | 5% of payments made to qualified organizations (e.g., Utah universities) for basic research conducted in Utah that exceed the base amount. | Up to 14 consecutive taxable years. |

| Current-Year Volume | 7.5% | 7.5% of the taxpayer’s total Utah-based QREs for the current taxable year (no base amount subtraction is required). | No carryforward; must be utilized in the current tax year. |

Calculating the Base Amount and Start-Up Elections: The calculation of the “base amount” for the 5% incremental component generally follows the federal guidelines in IRC § 41(c). The base amount is the product of a “fixed-base percentage” and the average annual Utah gross receipts for the four preceding taxable years. The base amount can never be less than 50 percent of the current year’s QREs.

A critical divergence from federal law exists regarding start-up companies. Federally, a complex set of rules dictates whether a company qualifies as a start-up (generally, having both gross receipts and QREs in a taxable year beginning after 1983). However, Utah Code Ann. § 59-10-1012(3)(a)(iii) and § 59-7-612 explicitly state that for purposes of calculating the Utah base amount, a taxpayer “may elect to be treated as a start-up company regardless of whether the taxpayer meets the requirements”. This allows a mature Taylorsville manufacturing firm to irrevocably elect start-up status for its Utah calculation, utilizing a favorable 3 percent fixed-base percentage for its first five years of claiming the credit, dramatically lowering the base amount hurdle and increasing the incremental credit yield.

Methodology Exclusions: Utah statute explicitly prohibits the use of the federal Alternative Incremental Credit (AIC) method provided in IRC § 41(c)(4). However, subsequent administrative interpretations by the Utah State Tax Commission have clarified that the federal Alternative Simplified Credit (ASC) method is not excluded, providing taxpayers with multiple mathematical avenues to optimize their claims.

While the credit is strictly nonrefundable, the aggressive 7.5 percent volume component provides an immediate, powerful dollar-for-dollar reduction of current-year tax liabilities based on total eligible spend. Simultaneously, the 14-year carryforward provision on the 5% incremental components provides long-term strategic tax shielding for Taylorsville life science and fintech enterprises that may endure prolonged, pre-revenue development cycles.

Government Tax Administration Guidance and Case Law

The substantiation, defense, and ultimate realization of R&D tax credit claims require rigorous contemporaneous documentation and an acute awareness of recent judicial interpretations. Both the IRS and the Utah State Tax Commission maintain high evidentiary standards, and recent federal case law has significantly narrowed taxpayer leniency.

Federal Judicial Developments

The federal judiciary has recently issued several landmark rulings that refine the boundaries of IRC § 41, creating vital precedents for Taylorsville taxpayers.

The “Substantially All” Rule and Process of Experimentation: In Little Sandy Coal Co., Inc. v. Commissioner (T.C. Memo 2021-15, aff’d 7th Cir. 2023), the courts delivered a critical, taxpayer-unfavorable analysis of the process of experimentation test. The taxpayer, a shipbuilding company designing first-in-class vessels, was denied the credit because it failed to provide a “principled way” to determine that at least 80 percent of its employee activities for each specific vessel constituted elements of a process of experimentation. The taxpayer relied on arbitrary percentage estimates and the general “newness” of the vessels. The Seventh Circuit affirmed the Tax Court’s rejection of these estimates, cementing the IRS’s expectation for detailed, real-time documentation showing exactly how companies conduct structured experiments, track iterations, and resolve specific scientific uncertainties. Taylorsville manufacturing and technology firms must heed this warning by maintaining project tracking systems that explicitly capture hypothesis testing and iteration failure rates.

The Funded Research Exclusion: The issue of “funded research” is highly litigated, particularly for engineering and architectural firms performing client-driven work. In Meyer, Borgman & Johnson, Inc. v. Commissioner (8th Cir. 2024), the court upheld the denial of credits to a structural engineering firm, ruling the research was “funded” under IRC § 41(d)(4)(H). The court found that despite the taxpayer’s claim that payment was contingent on meeting specific building codes and regulations, the standard hourly and fixed-fee contracts did not sufficiently shift the ultimate financial risk of the research failing to the taxpayer.

Conversely, taxpayers have found recent success when contracts are meticulously drafted. In Smith v. Commissioner (T.C. Order 2024) and System Technologies, Inc. v. Commissioner (T.C. Order 2024), the Tax Court denied the IRS’s motions for summary judgment regarding funded research. In System Technologies, an industrial finishing system manufacturer successfully argued that its fixed-price contracts, governed by specific state choice-of-law provisions, placed the economic risk squarely on the taxpayer, as they were required to bear the costs of redesigning and remanufacturing systems that failed to meet performance specifications. These cases underscore the necessity for Taylorsville BPO and custom software developers to integrate tax strategy into their legal contract drafting, ensuring they retain substantial rights to developed IP and structure payments to reflect true economic risk.

Specificity of Uncertainty: In Phoenix Design Group, Inc. v. Commissioner (2024), the Tax Court ruled against an engineering firm because it failed to identify specific technological uncertainties at the outset of the research, relying instead on generalized assertions of design challenges. This reinforces the IRS’s stance that general engineering problem-solving does not equate to a qualifying process of experimentation; the uncertainty must be specifically identified and documented before the research commences.

Utah State Tax Commission Jurisprudence and Administration

The Utah State Tax Commission has demonstrated a localized enforcement philosophy that heavily relies on federal definitions while strictly enforcing the geographic boundaries of the state credit.

Utah Tax Commission Decision 16-1707: In a vital Guiding Decision, Utah State Tax Commission Decision 16-1707, the Commission evaluated an appeal by an S-corporation (a construction and design-build firm headquartered in Utah) claiming the Utah research tax credit. The Auditing Division denied the claim, asserting the wages did not qualify as QREs and failed the base amount calculations. The Administrative Law Judge sustained the audit assessment entirely.

The Commission explicitly ruled that the burden of proof rests firmly on the taxpayer to demonstrate that the specific employee activities performed in Utah satisfied all elements of the federal four-part test. The decision underscored that general assertions of pre-construction design work do not suffice; the taxpayer must provide technical documentation proving a true technological process of experimentation. The Commission noted unfavorably that the taxpayer could not produce federal case law showing the IRS approved similar construction activities. Furthermore, the Commission addressed the base amount, emphasizing that even if QREs are established, the taxpayer must maintain historical accounting records to accurately compute the base amount. The Commission warned against arbitrary start-up fixed-base percentage elections without substantive proof of the company’s historical QRE-to-gross-receipts ratio.

State Administrative Reporting Mechanics: Unlike the federal government’s highly detailed Form 6765, the Utah State Tax Commission does not provide a specific, standalone calculation worksheet for the R&D tax credit. Instead, the Utah credit is a “self-reporting” mechanism. Individual and pass-through entities report the final calculated credit amount on Utah Form TC-40A (Income Tax Supplemental Schedule, Part 4) using code 12. C-Corporations claim it on Form TC-20.

This absence of an official state calculation form places a heavier administrative burden on the taxpayer to maintain immaculate, federally compliant worksheets and nexus-apportionment schedules in their private records. In the event of a Utah Tax Commission audit, the taxpayer must be prepared to immediately produce the mathematical justification for the 5% incremental and 7.5% volume components, alongside the qualitative documentation satisfying the four-part test.

Final Thoughts

The strategic utilization of the United States federal and Utah state Research and Development tax credits provides a profound, non-dilutive capital advantage to businesses operating within Taylorsville, Utah. The city’s historical evolution—catalyzed by visionary entrepreneurs like James LeVoy Sorenson, supported by localized legislative tools like the ILC charter, and anchored by infrastructure such as the Sorenson Research Park—has created an ideal, dense ecosystem for high-technology, medical device, financial technology, and life science industries.

By meticulously applying the federal four-part test under IRC § 41 and strictly adhering to the geographic and evidentiary requirements mandated by Utah Code Ann. § 59-7-612, Taylorsville enterprises can convert their inherent technological uncertainties and iterative experimental processes into highly lucrative tax capital. However, as demonstrated by recent federal appellate rulings (such as Little Sandy Coal and Meyer, Borgman & Johnson) and Utah State Tax Commission decisions, the realization of these economic benefits demands rigorous, real-time documentation of the scientific process and careful structural execution of commercial contracts to avoid “funded research” exclusions. When executed correctly, these dual tax mechanisms not only subsidize the high cost of continuous innovation but secure Taylorsville’s ongoing position as a vital node in the Intermountain West’s technology and life sciences corridor.

The information in this study is current as of the date of publication, and is provided for information purposes only. Although we do our absolute best in our attempts to avoid errors, we cannot guarantee that errors are not present in this study. Please contact a Swanson Reed member of staff, or seek independent legal advice to further understand how this information applies to your circumstances.

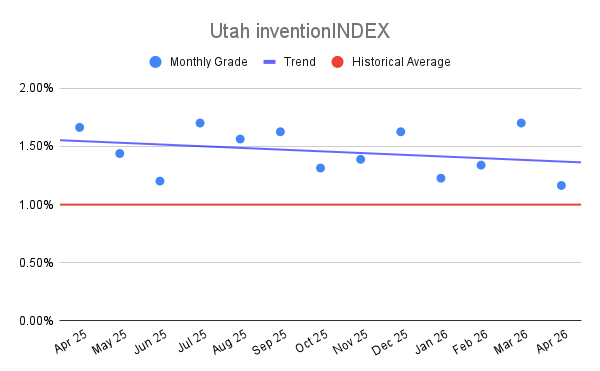

Utah inventionINDEX April 2026:

Utah inventionINDEX April 2026: