Industry Case Studies: The Intersection of Regional History and Innovation in West Jordan

To understand the application of federal and state tax laws, one must first understand the economic theater in which these technological advancements occur. The city of West Jordan, Utah, provides a profound case study in regional economic transformation. Situated between the Wasatch Mountains to the east and the Oquirrh Mountains to the west, West Jordan began in the mid-19th century as a pioneer agricultural settlement defined by its proximity to the Jordan River and Bingham Creek. Early settlers overcame significant geographic challenges by constructing cooperative irrigation networks, such as the South Jordan Canal in 1869, which catalyzed an agricultural and milling boom. Simultaneously, the discovery of ore in the Oquirrh Mountains in 1863 established a heavy industrial and mining legacy that would shape the region for a century.

Today, West Jordan is Utah’s third-largest city, possessing a population exceeding 104,000, a labor force of nearly 700,000 within a forty-mile radius, and over 6,000 acres of land zoned for commercial and industrial expansion. The municipal government, through its Redevelopment Agency (RDA), actively utilizes Tax Increment Financing (TIF) and Community Development Areas (CDAs) to attract high-technology enterprises. The following five industry case studies detail how specific sectors took root in West Jordan and how their operations qualify under the strict parameters of the United States and Utah State R&D tax credit laws.

Advanced Aerospace Composites and Manufacturing

The aerospace manufacturing sector in West Jordan is anchored by major corporate investments, most notably by The Boeing Company and Hexcel Corporation. The historical development of this industry in the municipality is directly tied to the presence of the South Valley Regional Airport (U42). Originally constructed as a military training base during World War II, the airport evolved into a primary general aviation reliever facility for Salt Lake City International Airport and a critical base for the Utah Army National Guard. Recognizing the logistical advantages of this aviation infrastructure, combined with the city’s available industrial acreage and a highly educated workforce generated by the forty universities located within a forty-mile radius, aerospace conglomerates identified West Jordan as an optimal expansion site. In 2013, Boeing purchased a massive 850,000-square-foot facility in West Jordan, transforming a vacant warehouse into a state-of-the-art composite fabrication center dedicated to manufacturing the horizontal stabilizers for the 787-9 Dreamliner. Concurrently, Hexcel Corporation established a Center of Research and Technology (R&T) Excellence in the immediate vicinity to support next-generation carbon fiber matrix operations for defense and commercial aerospace applications.

From a tax administration perspective, the research conducted by these aerospace entities is subject to intense scrutiny under the Internal Revenue Service (IRS) Audit Techniques Guide (ATG) for the Aerospace Industry. Aerospace engineering involves inherent technical uncertainties regarding the thermodynamics, shear strength, and aerodynamic stress limits of novel composite materials. To qualify for the federal R&D tax credit under Internal Revenue Code (IRC) Section 41, the development of composite horizontal stabilizers must be undertaken to improve the strength-to-weight ratio and fuel efficiency of the aircraft, thereby satisfying the permitted purpose requirement. The process of experimentation involves constructing prototype layup molds, performing finite element analysis computational modeling, and subjecting carbon fiber components to destructive stress testing inside the West Jordan facility to ensure strict compliance with Federal Aviation Administration tolerances. Under the law of the United States, the wages paid to aerospace engineers and metallurgists in West Jordan, alongside the raw carbon fiber completely consumed during destructive testing, constitute highly eligible Qualified Research Expenses (QREs). Furthermore, because these experimental iterations occur entirely within the borders of Utah, these expenditures generate significant eligibility for the Utah State R&D Credit, specifically the volume-based tier, provided the entity has sufficient state tax liability.

Structural Steel Fabrication and Advanced Civil Engineering

The heavy manufacturing and structural engineering sector in West Jordan is prominently represented by SME Steel Contractors. The historical rationale for the development of the structural steel industry in this specific municipality is deeply intertwined with the region’s legacy of mining and heavy equipment staging. Founded in 1992, SME Steel required massive tracts of appropriately zoned industrial land to accommodate a 400,000-square-foot fabrication facility and a one-hundred-acre laydown yard for structural steel inventory. West Jordan’s geography, offering expansive flatlands adjacent to major transportation arteries like Interstate 15 and the Union Pacific rail corridors, provided the necessary logistical framework. SME Steel has since fabricated critical, highly complex structural components for projects across the western United States, including the seismic-resistant elements of the Bellagio Resort, the 320,000-pound sky bridge at City Creek Center, and the unique structural exoskeleton of the (W)rapper Tower in Los Angeles.

Eligibility for R&D tax credits in the structural engineering sector is heavily regulated by both federal statute and precise judicial precedent. The engineering efforts undertaken by SME Steel to design automated welding processes, seismic-dampening connections, and novel erection sequencing methods rely fundamentally on the physical sciences and mechanical engineering. Designing an exoskeleton building where structural steel bands eliminate the need for traditional internal gravity columns presents profound geometric and load-bearing uncertainties. The experimentation process involves advanced three-dimensional Building Information Modeling, iterative computational stress simulations regarding wind load distribution, and the physical metallurgical testing of novel weld joints prior to full-scale shop fabrication. However, structural engineers must navigate the stringent “funded research” exclusion under IRC Section 41(d)(4)(H). As established in the United States Tax Court and affirmed by the Eighth Circuit in Meyer, Borgman & Johnson, Inc. v. Commissioner, engineering firms cannot claim R&D credits if they are compensated on a strict time-and-materials basis without retaining economic risk or substantial rights to the underlying design. To claim the federal and Utah state credits, West Jordan-based engineering firms must structure their contracts utilizing fixed-price or lump-sum models, thereby assuming the financial risk of failure during the fabrication design phase. Upon satisfying this contractual threshold, the localized wages of computer-aided design modelers, weld engineers, and fabrication supervisors operate as premium inputs for both the federal credit and the Utah state incremental and volume credits.

Underground Mining Technology and Geotechnical Ground Control

The geotechnical engineering and mining technology sector in West Jordan is epitomized by the presence of DSI Underground, a global leader in subterranean ground control solutions. The development of this industry in West Jordan is a direct geographical consequence of the city’s adjacency to the Bingham Canyon Mine, recognized as one of the largest open-pit and underground copper mining operations in the world. This proximity created a natural epicenter for geotechnical innovation, allowing DSI Underground to establish its United States headquarters and specialized research facilities in West Jordan. Operating mere miles from the active extraction zones, DSI’s engineers collaborate with local mining operators to develop and iteratively test ground support solutions capable of withstanding extreme subterranean environments, thereby embedding the industry deeply into the local economic fabric.

The technological demands of modern mining require continuous research into materials science and chemical engineering, presenting robust opportunities for R&D tax credit utilization. DSI Underground conducts research to formulate novel resin roof bolts, Glass-Fiber Reinforced Polymer tendons, and Polymer Rock Dust Systems aimed at mitigating coal dust explosions and stabilizing collapsing geological strata. Technical uncertainty arises when ground support systems must be deployed in highly acidic, corrosive mine water exhibiting pH levels of three, combined with extreme underground thermal conditions where standard steel supports undergo rapid chemical degradation. The process of experimentation entails the chemical formulation of distinct silicate and polyurethane injection resins, the fabrication of prototype glass-fiber hollow bars, and the execution of iterative load-bearing and chemical bath tests within their West Jordan laboratories. The expenditures dedicated to formulating and destructively testing these polymer resins are highly eligible QREs under federal law. Furthermore, by executing the chemical testing and mechanical stress modeling entirely within their West Jordan facility, the salaries of their resident geotechnical engineers directly qualify for the Utah State R&D calculation. In instances where these entities engage in collaborative basic research payments with local academic institutions, such as the University of Utah’s mining engineering department, they may additionally trigger the highly specific five percent basic research credit provided under Utah Code Section 59-7-612.

Food Science, Biological Engineering, and Nutritional Optimization

The food science and advanced nutritional manufacturing sector is a massive economic driver in West Jordan, dominated by the operations of Danone North America (formerly The Dannon Company). The historical justification for a massive dairy processing presence in West Jordan traces back to the city’s pioneer origins. The early diversion of the Jordan River established a lush agricultural and dairy farming ecosystem in the Salt Lake Valley. Capitalizing on this legacy, combined with modern municipal water infrastructure capable of supporting immense industrial consumption, Danone opened a colossal yogurt processing facility in West Jordan in 1997. Operating thirteen highly automated production lines and processing over 125,000 gallons of raw milk daily through 50,000-gallon silos, the 160,000-square-foot plant operates as a critical hub for biological and food engineering.

While the standard, repetitive production of food products is statutorily excluded from the federal R&D tax credit, the formulation of novel food matrices and the biological manipulation of bacterial cultures represent highly sophisticated, qualifying research. Danone continually undertakes research to develop functional foods, adhering to corporate commitments to improve nutrient density, increase trace vitamins, and drastically reduce total sugar content to less than twenty-three grams per serving, while simultaneously eliminating lipid content without degrading the physical emulsion or organoleptic properties of the product. This research relies fundamentally on the biological sciences and chemistry. Removing sugar and fat from dairy products severely disrupts the osmotic pressure and bacterial fermentation rates of standard yogurt cultures, such as Lactobacillus bulgaricus. The technical uncertainty revolves around achieving the targeted viscosity, shelf-life stability, and taste profile using alternative natural sweeteners or genetically modified bacterial strains. The experimentation process involves systematic pilot batching, varying pasteurization thermodynamics, adjusting fermentation holding times, and conducting accelerated bacterial decay studies. The wages of food scientists, microbiologists, and process engineers operating the pilot scale-up laboratories within the West Jordan plant qualify for the federal R&D credit. Because the ingredients utilized during the pilot batch testing are completely consumed and destroyed, they constitute qualified supply QREs under IRC Section 41(b). Under Utah tax administration guidance, the sheer magnitude of these physical trials occurring inside the state allows the corporate entity to heavily leverage the 7.5 percent volume credit to offset its Utah corporate franchise tax liability.

Data Center Infrastructure and Enterprise Software Development

The transition of West Jordan into a hub for digital infrastructure and enterprise software engineering is a testament to proactive municipal economic engineering. The prime example is the arrival of PayPal Inc. and Aligned Energy Data Centers. In a strategic maneuver to revitalize a defunct Fairchild semiconductor manufacturing plant, the West Jordan Redevelopment Agency established Economic Development Area Number Four (EDA #4). Data centers and the software engineers who operate them require massive, uninterrupted electrical consumption and advanced thermodynamic cooling systems. West Jordan leveraged its naturally cool high-desert climate, robust electrical grids, and aggressively negotiated a multimillion-dollar municipal energy tax rebate via Tax Increment Financing to attract Aligned Energy. PayPal emerged as the anchor tenant, proposing a massive 663-million-dollar capital investment, thereby securing the city’s position on the map for Fortune 500 technology firms.

Software engineering, particularly regarding financial technology, data virtualization, and high-frequency transaction routing, is heavily regulated under the IRS internal-use software provisions. PayPal’s operations require the continuous, iterative development of network management software, transaction load-balancing algorithms, and automated cryptographic security protocols capable of processing billions of global payments seamlessly. The engineering effort relies strictly on the principles of computer science. Technical uncertainty is omnipresent when attempting to achieve microsecond latency across distributed global servers while defending against synchronized cyber threats. The United States Treasury Regulations explicitly state that simply selecting a separate server or utilizing commercially available software configurations is excluded from the credit. Therefore, software engineers in West Jordan must conduct a rigorous process of evaluating different load distribution alternatives, utilizing agile development environments, and executing code virtualization testing to resolve unique scalability bottlenecks. If the software is developed primarily for internal use, it must additionally pass the High Threshold of Innovation Test, requiring the taxpayer to prove that the software is highly innovative, involves significant economic risk in its development, and is not commercially available for purchase. From the perspective of the Utah State Tax Commission, enterprise software development represents a highly efficient mechanism for credit generation; it requires minimal municipal infrastructure utilization while generating massive intellectual capital. The localized QREs generated by data scientists and software architects in West Jordan seamlessly translate into significant five percent incremental and 7.5 percent volume R&D credits under Utah Code Section 59-7-612.

The United States Federal Research and Development Tax Credit Framework

The stimulation of domestic innovation through tax policy remains a permanent fixture of United States economic strategy. The federal Research and Development tax credit, governed by Internal Revenue Code Section 41, provides a critical financial mechanism to offset the inherently high costs and risks associated with technological advancement. Following the enactment of the Protecting Americans from Tax Hikes Act of 2015, the credit was made a permanent provision of the tax code, solidifying its role in corporate financial planning. To claim this credit, a taxpayer operating in West Jordan must meticulously demonstrate that their activities meet the rigid statutory definition of “qualified research.”

The Statutory Four-Part Test

Under IRC Section 41(d), an activity must satisfy a rigorous four-part test to qualify as research. The Internal Revenue Service applies this test at the business component level, and failure to meet any single criterion completely disqualifies the associated expenditures from the credit calculation.

| Statutory Requirement | Legal Definition and Mechanism | IRS Audit Focus and Case Law Implications |

|---|---|---|

| The Section 174 Test (Permitted Purpose) | Expenditures must be eligible for treatment as research and experimental expenditures under IRC Section 174. The research must be undertaken for the purpose of discovering information to develop a new or improved “business component” (defined as a product, process, computer software, technique, formula, or invention) focusing strictly on functionality, performance, reliability, or quality. | The IRS ensures the research relates to the taxpayer’s active trade or business. Modifications based solely on aesthetic, cosmetic, or stylistic improvements are strictly excluded. |

| Technological in Nature | The research activity must fundamentally rely on the principles of the hard sciences, explicitly defined as physical sciences, biological sciences, computer science, or engineering. | IRS examiners rigorously differentiate between hard science and excluded soft sciences. Activities relying on economics, market research, sociology, or humanities are automatically disqualified. |

| Elimination of Technical Uncertainty | At the outset of the research project, there must exist a definitive technical uncertainty regarding the capability to develop the business component, the method to develop it, or the appropriate design of the component itself. | Taxpayers must demonstrate through contemporaneous documentation that the knowledge required to achieve the desired outcome was not readily available within their baseline knowledge or the public domain. |

| The Process of Experimentation | Substantially all (legally defined as eighty percent or more) of the research activities must constitute a process of experimentation. This involves a systematic process of identifying the uncertainty, formulating hypotheses, evaluating multiple alternatives through modeling, simulation, or systematic trial and error, and refining the component based on those empirical results. | The IRS heavily polices this requirement, leaning on the Little Sandy Coal judicial precedent. Taxpayers must provide granular proof of structured hypothesis testing and the tracking of failed iterations, rather than relying on generalized trial and error. |

Statutory Exclusions and the “Shrinking Back” Doctrine

The Internal Revenue Code outlines specific activities that are expressly excluded from the definition of qualified research, regardless of their technological sophistication. These exclusions are heavily audited by the IRS. Research conducted outside the United States, the Commonwealth of Puerto Rico, or any United States possession is entirely ineligible for the federal credit, ensuring the incentive remains a driver of domestic labor. Furthermore, the adaptation of an existing business component to a particular customer’s requirement, or the reproduction of an existing business component through reverse engineering, is statutorily excluded. Research conducted after the commercial production of the business component has begun is also disqualified, requiring a strict delineation between the experimental design phase and standard manufacturing operations.

Perhaps the most heavily litigated exclusion is “funded research.” Under IRC Section 41(d)(4)(H), research funded by any grant, contract, or another person or governmental entity is ineligible. If a taxpayer in West Jordan does not retain substantial rights to the research results, or if their payment is guaranteed regardless of the research’s success, the research is deemed funded by the client. This is particularly relevant for custom fabrication and engineering firms.

When facing an IRS examination, taxpayers must adhere to the “Shrinking Back Rule”. As federal courts have repeatedly affirmed, if a broader business component—such as an entire data center facility or a massive commercial building—fails any part of the four-part test, the taxpayer cannot claim the entire project. Instead, the taxpayer must apply the test to a subset of the product, systematically shrinking the analysis back until it reaches the specific sub-component (such as a unique seismic weld or a specific load-balancing software algorithm) that definitively involves a process of experimentation.

Financial Mechanics: Section 41 Offset and Section 174 Amortization

The mechanics of the federal R&D tax credit have been profoundly impacted by recent legislative overhauls. The credit is generally calculated based on QREs that exceed a historically calculated base amount. QREs are strictly limited to wages paid for direct research, direct supervision, or direct support of research; the cost of physical supplies completely consumed or destroyed in the research process; and sixty-five percent of the expenses paid to domestic third-party contractors conducting research on the taxpayer’s behalf.

Crucially, under changes enacted by the Tax Cuts and Jobs Act, taxpayers are no longer permitted to immediately deduct their Section 174 research and experimental expenditures in the year they are incurred. Instead, taxpayers must capitalize and amortize all Section 174 expenses over a mandatory five-year period for domestic research, or a fifteen-year period for foreign research. This shift fundamentally alters the cash-flow dynamics of corporate capital investments. However, taxpayers may continue to utilize the Section 41 credit to offset their tax burden, subject to the rules of Section 280C, which require that any deduction under Section 174 be reduced by the amount of the R&D credit taken, unless the taxpayer explicitly elects a reduced credit calculation.

The Utah State Research and Development Tax Credit Architecture

While the federal government sets the baseline parameters for innovation incentives, the Utah State Legislature has constructed a highly localized, aggressively structured R&D tax credit system. This system is designed to seamlessly integrate with the federal definitions under IRC Section 41, while applying strict geographical limitations and unique volume-based incentives to stimulate capital investment specifically within Utah’s borders.

Statutory Governance and the “Incurred in Utah” Doctrine

The Utah Research and Development Tax Credit is a permanent fixture of the state’s tax code, possessing no sunset provision, and is codified under two primary statutory paths. For corporate entities subject to the state franchise tax, the governing law is Utah Code Section 59-7-612. For individual taxpayers, estates, and trusts—including those receiving pass-through income allocations from S-corporations, partnerships, or limited liability companies—the identical substantive requirements are codified in Utah Code Section 59-10-1012.

Utah tax law explicitly adopts the federal definitions of “qualified research” and “qualified research expenses” as detailed in IRC Sections 41(b) and 41(d). However, the state introduces a critical, non-negotiable geographic limitation: only qualified research activities physically conducted within the borders of the State of Utah are eligible for the state credit. The Utah State Tax Commission vigorously audits the apportionment of wages and supplies to enforce this “Incurred in Utah” doctrine. A West Jordan-based corporation that subcontracts metallurgical testing to a laboratory in California may legitimately claim those contractor expenses for the federal IRC Section 41 credit, but those identical costs must be entirely excluded from the Utah calculation. Furthermore, for the purpose of calculating historical base amounts, only gross receipts attributable to sources within Utah are considered.

The Tripartite Credit Structure and Carryforward Mechanics

The Utah R&D tax credit is distinctively multifaceted, utilizing a three-tiered structure that rewards both the incremental growth of research intensity and the sheer absolute volume of research investment occurring in the state. This framework provides maximum benefit to companies scaling operations in municipalities like West Jordan.

| Credit Component | Statutory Calculation Methodology | Carryforward Provisions and Legislative Restrictions |

|---|---|---|

| The Incremental Credit | Calculated as 5.0 percent of the taxpayer’s current-year Utah-based QREs that exceed a historical base amount. The base amount is calculated utilizing the framework of IRC Section 41(c), applying a historical fixed-base percentage to the average Utah gross receipts for the prior four taxable years. | If the calculated incremental credit exceeds the taxpayer’s current tax liability, the unused portion may be carried forward for a period of up to fourteen consecutive taxable years. It may not be carried back. |

| The Basic Research Credit | Calculated as 5.0 percent of payments made to qualified organizations (such as Utah-based universities, hospitals, or scientific tax-exempt entities) for basic research conducted physically in Utah that exceed a specific base amount. | Similar to the incremental tier, unused credits generated from basic research payments may be carried forward for a period of up to fourteen consecutive taxable years. |

| The Volume Credit | A highly lucrative tier calculated as a flat 7.5 percent of the taxpayer’s total, gross qualified research expenses for the current taxable year, regardless of historical base amounts. | Strictly prohibited from being carried forward. Utah Code explicitly states that any portion of the 7.5 percent volume credit not utilized to offset tax liability in the exact year it is generated is permanently forfeited. |

The carryforward prohibition attached to the 7.5 percent volume credit requires sophisticated tax planning by corporate controllers in West Jordan. A massive manufacturing facility that generates immense QREs during a prototyping phase must possess adequate and immediate Utah franchise or income tax liability to absorb the credit. If the operational tax liability is insufficient in that specific fiscal year, the immense value of the volume credit evaporates entirely.

Administrative Rulings and Judicial Precedent of the Utah State Tax Commission

The administration of these tax laws falls under the jurisdiction of the Utah State Tax Commission. The Commission provides critical guidance to taxpayers through the issuance of Private Letter Rulings (PLRs) under Utah Administrative Code R861-1A-34. A PLR is a written, informational statement detailing the Commission’s interpretation of statutes and their application to a specific taxpayer’s unique technological facts and circumstances. Taxpayers in West Jordan seeking clarity on complex software virtualization or untested metallurgical processes frequently request PLRs to mitigate audit risk before filing their corporate returns.

Furthermore, decisions generated through the Commission’s formal appeals process establish binding precedent on how R&D credits are administered. In cases such as Appeal No. 16-1707, the Commission has demonstrated a rigid adherence to federal case law when evaluating state credit claims. Taxpayers operating in the construction or standard software development sectors who appeal denied credits face severe burdens of proof. The Commission requires taxpayers to present established federal case law demonstrating that the IRS has previously approved QREs under identical technological circumstances. Without corresponding federal validation that the activities satisfy the stringent four-part test and the process of experimentation, the Utah State Tax Commission will systematically uphold the denial of the state-level credits.

Final Thoughts

The city of West Jordan, Utah, serves as a masterclass in the convergence of municipal economic development, state-level tax architecture, and federal innovation policy. By intelligently leveraging its geographic advantages, pioneer infrastructure roots, and aggressive municipal redevelopment tools such as Tax Increment Financing, the city has successfully transitioned its legacy economy into a diversified powerhouse of advanced research.

Corporations anchoring themselves in West Jordan—whether engineering advanced aerospace composites, forging seismic-resistant structural steel, formulating deep-earth polymer resins, bio-engineering nutritional profiles, or architecting global financial software—operate within an immensely favorable tax environment. By meticulously documenting their technological uncertainties and maintaining rigorous records of their experimental processes, these entities can secure the permanent federal R&D tax credit to offset the massive capitalization costs newly mandated by Section 174. Simultaneously, by executing these research activities physically within the city limits, they trigger the aggressive, localized Utah State R&D tax credit, capturing up to a 12.5 percent combined state incentive on their research expenditures. However, capitalizing on this dual-layered environment requires extreme vigilance. Taxpayers must navigate the relentless scrutiny of the IRS’s four-part test, strictly avoid the contractual traps of funded research, and utilize precise financial forecasting to circumvent Utah’s unique carryforward prohibitions. Through careful statutory alignment and relentless innovation, the industries of West Jordan will continue to subsidize their technological risk profiles, ensuring sustained regional economic growth and national industrial supremacy.

The information in this study is current as of the date of publication, and is provided for information purposes only. Although we do our absolute best in our attempts to avoid errors, we cannot guarantee that errors are not present in this study. Please contact a Swanson Reed member of staff, or seek independent legal advice to further understand how this information applies to your circumstances.

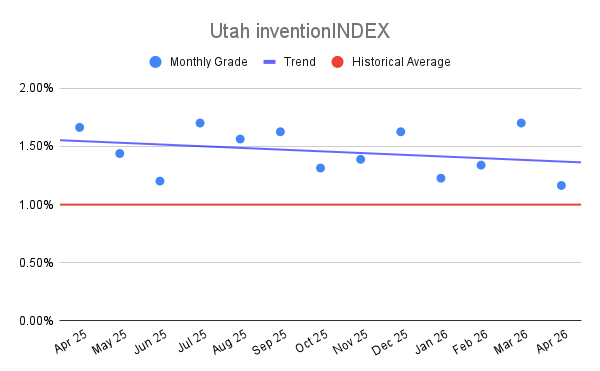

Utah inventionINDEX April 2026:

Utah inventionINDEX April 2026: