The Kenosha, Wisconsin region has successfully leveraged both the United States Federal and Wisconsin State Research and Development (R&D) tax credits to transition from legacy automotive manufacturing into a diverse hub for advanced logistics, biotechnology, food science, and precision tooling. Qualifying businesses can offset innovation costs through the federal incremental credit and the Wisconsin general 5.75% credit. Crucially, Wisconsin offers a 25% refundability provision for startups and a targeted 11.5% enhanced credit rate for internal combustion engine and energy-efficient product development, strongly incentivizing the nearshoring of complex mechanical operations.

This study analyzes the United States federal and Wisconsin state Research and Development (R&D) tax credit frameworks, specifically evaluating their application within the evolving industrial landscape of Kenosha, Wisconsin. It provides five industry-specific case studies demonstrating regional economic development, followed immediately by a detailed analysis of statutory requirements, tax administration guidance, and relevant case law.

Industrial Evolution and R&D Tax Credit Application in Kenosha, Wisconsin

The economic landscape of Kenosha, Wisconsin, is a testament to industrial resilience and strategic regional planning. Situated strategically within the Interstate 94 corridor between Chicago, Illinois, and Milwaukee, Wisconsin, Kenosha possesses a deep manufacturing heritage that has fundamentally influenced its modern capacity for advanced research and development. Historically, the local economy was monopolized by heavy automotive manufacturing, tracing its roots back to 1902 when the Thomas B. Jeffery Company opened one of the nation’s first automobile plants. This facility eventually evolved into the American Motors Corporation (AMC) and subsequently the Chrysler Kenosha Engine Plant, a massive 107-acre complex encompassing 1.87 million square feet of industrial space that employed thousands of local residents. The permanent closure and subsequent demolition of this plant between 2010 and 2013 catalyzed a severe economic displacement, forcing regional leadership to orchestrate a massive economic pivot.

Through the coordinated efforts of the Kenosha Area Business Alliance (KABA) and local government entities, the region utilized Tax Incremental Financing (TIF) and revolving loan funds to rehabilitate vacant industrial tracts and attract diversified, knowledge-based industries. A cornerstone of this revitalization is the Kenosha Innovation Neighborhood (KIN), a project managed by an independent nonprofit organization that transforms the former Chrysler site into a mixed-use innovation district focusing on entrepreneurship, workforce upskilling, and leading-edge startup incubation. A comprehensive ecosystem study conducted by the Waymaker Group in 2021 identified that Kenosha is situated within a one-hundred-mile radius of over two billion dollars in annual life sciences and technology research, possessing a highly skilled STEM workforce that previously commuted out of state. Capitalizing on this human capital and geographic superiority, Kenosha successfully attracted over 4.8 billion dollars in capital investment and nearly five million square feet of new development from 2023 onward. The region transitioned from legacy automotive assembly into a diverse hub for advanced logistics, biotechnology, food science, precision tooling, and high-technology manufacturing. The following five case studies detail how specific industries developed within this rejuvenated economic environment and analyze how their highly technical operations satisfy the stringent requirements of the United States federal and Wisconsin state R&D tax credit laws.

Case Study 1: Supply Chain, Logistics, and Packaging Innovation at Uline

The logistics and distribution industry developed rapidly in Kenosha due to the county’s immediate proximity to the Interstate 94 corridor, providing frictionless access to the massive consumer markets of the American Midwest. Uline, North America’s premier distributor of shipping, industrial, and packaging materials, recognized this geographic advantage and established its headquarters and primary distribution network within the county. Celebrating over forty-five years of continuous business operations, Uline has expanded its corporate footprint to encompass over twenty-eight million square feet across North America. Within Kenosha County specifically, Uline recently constructed a 1.44 million-square-foot warehouse, representing the largest distribution facility in the state of Wisconsin, designed to support the company’s commitment to same-day shipping across a catalog exceeding 43,000 distinct products.

While supply chain distribution is traditionally categorized as an operational rather than a scientific endeavor, the unprecedented scale of Uline’s operations necessitates continuous, highly complex technological innovation that qualifies for federal and state R&D tax credits. The company engages in extensive research and development related to packaging design engineering and software-driven warehouse automation. To satisfy the federal requirement of a permitted purpose, Uline’s engineering teams continuously develop new automated material handling systems and high-speed sorting mechanisms designed to improve the performance and reliability of warehouse transit times. The technological uncertainty inherent in these projects stems from the immense difficulty of integrating proprietary robotic picking systems with legacy warehouse management software without causing catastrophic disruptions to continuous operational uptime.

To eliminate these uncertainties, Uline software developers and mechanical engineers engage in a rigorous process of experimentation based on the hard sciences of computer science and mechanical engineering. This involves iteratively testing dynamic routing algorithms under simulated peak-load conditions, prototyping varied automated conveyor geometries, and utilizing finite element analysis to simulate the structural integrity of novel corrugated packaging materials under extreme environmental and mechanical stresses. Under the United States federal tax code, the wages paid to the software developers and process engineers conducting these simulations constitute Qualified Research Expenses (QREs). Because this research is conducted physically within Kenosha, the expenses also qualify for the Wisconsin state R&D credit. Specifically, these activities fall under the general research category, allowing Uline to claim a credit equal to 5.75 percent of the amount by which their current-year qualified research expenses exceed their historical base amount.

Case Study 2: Pharmaceuticals and Biotechnology Manufacturing at Eli Lilly and Company

The emergence of the biotechnology and pharmaceutical sector in Kenosha is a direct result of targeted regional economic planning that sought to capture the spillover of life sciences investment from neighboring Chicago and Milwaukee. In 2024, Eli Lilly and Company, a multinational pharmaceutical corporation, acquired a state-of-the-art parenteral manufacturing facility in the Prairie Highlands Corporate Park of Pleasant Prairie, a municipality within Kenosha County, from Nexus Pharmaceuticals. Shortly after the acquisition, Eli Lilly announced an unprecedented three-billion-dollar expansion of the site, marking the company’s single largest domestic manufacturing investment outside its home state of Indiana. This massive capitalization is fundamentally driven by the exponential global demand for Eli Lilly’s advanced diabetes and obesity medications, specifically its dual-agonist peptide therapeutics. The expansion is projected to integrate an additional 750 highly skilled engineers, scientists, and advanced manufacturing personnel into the local economy, establishing Kenosha as a critical nexus in the global pharmaceutical supply chain.

The transition of complex therapeutic formulations from laboratory-scale discovery into mass-produced sterile injectables is fraught with biological, chemical, and engineering challenges that perfectly align with the legislative intent of the R&D tax credit. The federal permitted purpose of this research is the development of improved manufacturing processes that guarantee absolute sterility, optimal viscosity, and active ingredient stability during high-speed compounding and packaging. Significant technological uncertainty exists regarding the thermal degradation rates of sensitive peptide formulations when subjected to the sheer stress of industrial pumping mechanisms, as well as the integration of advanced robotics and guided vehicles required for automated device assembly in cleanroom environments.

To overcome these biological and engineering hurdles, Eli Lilly’s process engineers and microbiologists must execute systematic trial batches and validation protocols. This process of experimentation involves adjusting fluid dynamic parameters, calibrating automated filling machinery, and conducting accelerated stability testing on the resulting parenteral barriers. The costs associated with producing these trial batches, including the raw chemical inputs destroyed during testing and the salaries of the scientific personnel overseeing the trials, meet the strict federal definition of in-house research expenses. In Wisconsin, this qualifies for the 5.75 percent general credit rate, generating massive tax offsets that subsidize the immense capital requirements of pharmaceutical scale-up. Furthermore, the State of Wisconsin provides a concurrent sales and use tax exemption specifically targeted at biotechnology firms, allowing Eli Lilly to purchase complex testing machinery and cleanroom equipment utilized exclusively in these research activities without incurring state sales tax.

Case Study 3: Food Science and Confectionery Processing at Haribo and Fair Oaks Foods

Kenosha County has cultivated a dense concentration of advanced food and beverage manufacturing operations, leveraging its proximity to Midwestern agricultural inputs and its unparalleled distribution access. Fair Oaks Foods, a premier supplier of custom meat products for global restaurant chains, exemplifies this legacy, having operated within the LakeView Corporate Park since 1992 after transitioning from its predecessor, Brooks Sausage Company. In a parallel development highlighting the region’s global appeal, the German-based confectionery giant Haribo selected Pleasant Prairie as the location for its first-ever North American manufacturing facility to address surging domestic demand. Haribo’s state-of-the-art 500,000-square-foot facility opened in 2023 following a 148.5 million dollar initial investment, currently producing over one hundred million Goldbears daily, with phased expansions designed to eventually scale the campus to two million square feet.

In the highly competitive food processing sector, R&D tax credits are frequently generated through the systematic application of food science to develop novel formulations, extend shelf life, and engineer advanced thermal processing techniques. For Haribo, the development of new gummy variations tailored to American consumer preferences—such as wild berry variants or formulations requiring integration with distinct regional water chemistries and domestic agricultural sugars—presents significant technical uncertainties. These uncertainties involve predicting the thermodynamic behavior of gelling agents, managing moisture migration to prevent crystallization over time, and ensuring homogeneous flavor dispersion. Similarly, Fair Oaks Foods must continuously scale proprietary custom meat recipes, facing uncertainties regarding the thermal dynamics of industrial convection ovens, the optimization of fat rendering rates, and the efficacy of natural preservative alternatives under variable storage conditions.

The process of experimentation in food science requires deep reliance on chemistry and microbiology. Food scientists at these facilities engage in iterative trial and error by systematically adjusting variables such as potential hydrogen (pH) levels, extrusion pressures, holding temperatures, and organic ingredient substitutions. The resulting trial batches undergo rigorous accelerated stability tests, organoleptic evaluations, and rheological analyses to ensure the final product maintains specific textural and safety profiles. Both federal and Wisconsin tax frameworks recognize biological sciences and food chemistry as valid hard sciences under the IRC Section 41 four-part test. Consequently, the wages of the food scientists, the costs of the raw ingredients consumed or destroyed in both successful and failed trial batches, and the specialized supplies used in the test kitchens constitute eligible QREs. By claiming the Wisconsin 5.75 percent general research credit, these food processing entities significantly lower their effective cost of innovation, allowing them to remain price-competitive in global consumer markets.

Case Study 4: Advanced Manufacturing and Precision Tooling at Snap-on and XTEN Industries

The precision tooling and advanced manufacturing sectors in Kenosha trace their lineage directly back to the skilled engineering labor pool established by the legacy automotive assembly plants of the twentieth century. Snap-on Incorporated, a globally recognized leader in professional tools and diagnostic software, relocated its manufacturing operations and corporate headquarters from Chicago to Kenosha in 1930. Over the decades, Snap-on has pioneered critical mechanical innovations, including the Torqometer for precision aerospace clamping and the Red Brick handheld diagnostic scanner, amassing a portfolio of over 4,060 active and pending patents. Operating in tandem within the local manufacturing ecosystem, XTEN Industries established a massive presence in Kenosha specializing in highly automated, computer-controlled custom plastic injection molding, utilizing presses ranging from 80 to 900 tons to perform complex subassembly and what the company terms Multifacturing.

Precision tool manufacturing and industrial injection molding require relentless research and development to address the escalating complexities of modern advanced materials, proprietary automotive electronics, and strict aerodynamic tolerances. To satisfy the federal requirement of a permitted purpose, Snap-on continuously seeks to develop proprietary metallurgical alloys that simultaneously increase the tensile strength and reduce the physical weight of handheld tools, alongside updating incredibly complex diagnostic software required to interface with encrypted modern vehicle control modules. XTEN Industries faces profound technical uncertainty regarding polymer rheology and mold flow dynamics when attempting to inject highly engineered thermoplastic resins into exceedingly complex geometric molds without inducing sink marks, structural voids, or thermal warping.

The process of experimentation required to resolve these uncertainties is heavily grounded in physics, computer science, and mechanical engineering. Snap-on software engineers write, compile, and systematically debug custom code to establish new communication protocols with continuously evolving automotive hardware, while their resident metallurgists conduct destructive testing on dozens of heat-treatment variations. XTEN utilizes sophisticated computer-aided engineering (CAE) applications to simulate thermal cooling rates and fluid dynamics within theoretical injection molds, systematically adjusting physical injection pressure, barrel temperature, and hold times on the factory floor until dimensional stability is empirically proven. The systematic testing of alloys, the coding of diagnostic software, and the empirical mold-flow experimentation clearly satisfy the federal four-part test. Snap-on’s software development personnel wages and XTEN’s experimental resin consumed during test runs qualify as QREs under IRC Section 41(b). Because Kenosha retains these high-value engineering headquarters, both firms effectively leverage the Wisconsin 5.75 percent credit against their corporate franchise tax liabilities, securing their positions as technological leaders in the manufacturing sector.

Case Study 5: Power Equipment and Internal Combustion Engines at FNA Group

The development of the power equipment industry in Kenosha highlights a critical macroeconomic shift toward the nearshoring of complex industrial manufacturing. In recent years, global supply chain delays severely hindered North American product manufacturing and distribution, exposing the vulnerabilities of relying entirely on offshore production for critical mechanical components. In response, the FNA Group, a highly vertically integrated manufacturer of high-pressure cleaning equipment, pressure washers, and water pumps, executed a strategic decision to relocate parts of its OEM Industries Division from Arkansas to Pleasant Prairie in Kenosha County. To shorten lead times and exert absolute control over quality, FNA Group initiated the nearshoring of critical component manufacturing, most notably gasoline internal combustion engines. By situating its robust research and development team in immediate proximity to its newly established North American manufacturing base in Kenosha, the company aims to radically optimize engine design and domestic production efficiency.

The design, optimization, and domestic production of small gasoline engines and high-pressure thermoplastic hoses represent incredibly intense fields of mechanical engineering and fluid dynamics. Bringing internal combustion engine manufacturing onshore addresses a permitted purpose but requires fundamentally re-engineering legacy components to comply with the exceptionally stringent emissions standards and manufacturing tolerances mandated by North American regulatory bodies. Immense technological uncertainties exist in optimizing combustion chamber geometries for maximum fuel efficiency, developing lightweight crankcases that maintain structural integrity under thermal stress, and engineering proprietary thermoplastic hoses capable of withstanding massive hydrostatic pressures without catastrophic bursting.

To eliminate these uncertainties, FNA Group engineers must utilize advanced computational fluid dynamics (CFD) software to model theoretical air-fuel mixtures and exhaust flow trajectories, followed by the physical machining and construction of engine prototypes. These prototypes are subjected to rigorous, systematic experimentation, including destructive stress testing, extended dynamometer runs, and thermal fatigue cycles, with the empirical results dictating iterative adjustments to ignition timing, valve clearances, and alloy compositions. The FNA Group’s activities are a quintessential example of the specialized Wisconsin enhanced credit for internal combustion engines. Because their research is directly related to designing internal combustion engines and improving the physical production processes for such engines, the QREs generated by their engineering team in Pleasant Prairie qualify for the elevated 11.5 percent Wisconsin R&D credit rate. This enhanced rate effectively doubles the state subsidy compared to general manufacturing, providing a massive financial incentive that directly supports the economics of nearshoring complex mechanical operations from overseas to the state of Wisconsin.

| Industry Case Study | Kenosha Location | Core R&D Focus Area | Principal Scientific Disciplines | Applicable WI Statutory Credit Rate |

|---|---|---|---|---|

| Uline | Kenosha | Packaging algorithms, automated material handling, logistics software | Computer Science, Mechanical Engineering | General 5.75% |

| Eli Lilly | Pleasant Prairie | Injectable therapeutics scale-up, biologic stability, sterile automation | Biology, Chemistry, Process Engineering | General 5.75% |

| Haribo / Fair Oaks | Pleasant Prairie | Rheology, preservative testing, extrusion optimization, formulation | Food Science, Chemistry, Thermodynamics | General 5.75% |

| Snap-on / XTEN | Kenosha | Metallurgy, diagnostic software code, injection mold flow dynamics | Physics, Computer Science, Materials Science | General 5.75% |

| FNA Group | Pleasant Prairie | Internal combustion engine geometry, emissions control, nearshoring | Mechanical Engineering, Fluid Dynamics | Enhanced 11.5% |

Detailed Analysis of the United States Federal R&D Tax Credit

The federal Research and Development tax credit, formally established under Internal Revenue Code (IRC) Section 41 as the Credit for Increasing Research Activities, is a foundational economic mechanism designed to incentivize businesses to maintain and aggressively expand their investments in domestic innovation. The statutory intent of the federal government is to assist United States enterprises in remaining highly competitive within a rapidly advancing global market by subsidizing the exorbitant costs and inherent financial risks associated with complex technological development and scientific experimentation. The credit is structurally designed to be incremental, generally calculated as a percentage of qualified research expenditures that exceed a historically calculated base amount, thereby ensuring that the federal incentive explicitly rewards active increases in research efforts rather than subsidizing baseline, stagnant operational spending.

The Stringent IRS Four-Part Test for Qualified Research

For a business activity to be formally deemed qualified research under the strict definitions of IRC Section 41, it must independently and simultaneously satisfy a rigorous four-part test codified by the Internal Revenue Service (IRS). If a taxpayer fails to adequately document and prove that an activity meets any single criterion of this test, all associated expenses are entirely disqualified from the credit computation.

The first requirement, Permitted Purpose, mandates that the research activity must be undertaken with the explicit intention to develop a newly created or fundamentally improved business component. The tax code defines a business component comprehensively as any product, manufacturing process, computer software, technique, formula, or invention that is to be held for sale, lease, or license, or alternatively, used internally by the taxpayer in their own trade or business. Furthermore, the improvement must objectively relate to an enhancement in the component’s functionality, performance, reliability, or quality. The IRS explicitly states that routine aesthetic changes, seasonal design variations, or minor cosmetic modifications unequivocally fail to satisfy this requirement, as they do not constitute functional improvements.

The second requirement demands that the development process must be Technological in Nature. This means the activity must fundamentally rely upon the established principles of the hard sciences, specifically limited to engineering, physics, chemistry, biology, or computer science. The research activity must be deeply grounded in systematic, scientific methodologies to achieve the intended purpose. The tax code specifically excludes activities based on the social sciences, economics, behavioral psychology, humanities, or general market research from qualifying for the credit.

The third requirement, the Elimination of Uncertainty, dictates that at the precise outset of the project, the taxpayer must face demonstrable technological uncertainty regarding either the fundamental capability to develop the business component, the exact methodology required to achieve the desired outcome, or the appropriate final design of the product. If the capability to create the product is known, and the methodology is routine and easily predictable by competent professionals in the field, the activity does not qualify as it is merely the application of established knowledge. Taxpayers must prove they are venturing beyond standard operational procedures to address unknowns or limitations in current technology.

The fourth and most scrutinized requirement is the Process of Experimentation. To overcome the identified technical uncertainty, the taxpayer must engage in a systematic, evaluative process designed to test one or more alternatives. This process typically involves the utilization of computational modeling, physical simulation, systematic trial and error, or the formal formulation and rigorous testing of scientific hypotheses. The process must be inherently iterative, wherein the empirical results of initial tests directly dictate subsequent design modifications and further testing cycles until the uncertainty is resolved or the project is abandoned.

Classification of Qualified Research Expenses (QREs)

Under the strict provisions of IRC Section 41(b), taxpayers are not permitted to claim all costs loosely associated with an R&D department; rather, they may only claim specific, tightly defined categories of costs directly associated with the execution of qualified research activities. These Qualified Research Expenses (QREs) are statutorily limited to four primary categories.

The most substantial category is Wages. Section 41(b)(2) defines eligible in-house research expenses to include any taxable wages paid or incurred to an employee for qualified services performed by that employee. For the purposes of the credit, wages are defined identically to IRC Section 3401(a), encompassing all taxable wages reported on Form W-2, Box 1, including performance bonuses and stock option redemptions that are subject to federal withholding. It critically does not include amounts that are not subject to withholding, such as certain untaxed fringe benefits or retirement contributions, even if those benefits are provided to high-level scientific personnel performing research. Qualified services encompass not only the direct performance of the research but also the direct, first-line supervision of the researchers and the direct technical support of the research activities.

The second category is Supplies, defined as any amount paid or incurred for tangible property that is consumed or destroyed during the direct conduct of qualified research. This typically includes items such as physical prototypes, raw manufacturing materials, testing chemicals, and trial batch ingredients. The definition of supplies explicitly excludes the purchase of land, improvements to land, and any property subject to an allowance for depreciation. Therefore, the capital purchase of a highly advanced microscope or CNC milling machine cannot be claimed as a supply QRE, though the material destroyed by the milling machine during a test run can.

The third category allows for Contract Research Expenses. Section 41(b)(3) dictates that taxpayers may claim exactly sixty-five percent of any amount paid or incurred to another person or entity (other than an employee of the taxpayer) for the performance of qualified research on the taxpayer’s behalf. This statutory haircut accounts for the assumed overhead and profit margins embedded in third-party contracting rates.

The final category is Computer Rental Costs, encompassing amounts paid or incurred to another person for the right to use computers in the conduct of qualified research. In the modern digital economy, this often applies to costs associated with renting cloud computing environments or supercomputing mainframes specifically utilized to run complex computational modeling, finite element analysis, or massive software development compilations.

Taxpayers claiming the federal credit must adhere to incredibly rigorous substantiation and contemporary recordkeeping requirements. The IRS mandates detailed documentation to meticulously segregate qualified activities and their associated expenses from routine, non-qualified business operations. Recognizing historical abuses of the credit, the IRS has implemented severe regulatory shifts, including the introduction of newly expansive and granular reporting requirements on Form 6765, effective for tax year 2024. These changes demand highly detailed project-level accounting and technical narrative disclosures to preemptively validate claims before refunds are issued, deliberately increasing the administrative burden on taxpayers to minimize fraudulent submissions.

Detailed Analysis of the Wisconsin State R&D Tax Credit

The State of Wisconsin provides a formidable, comprehensive R&D tax credit framework designed to parallel the federal statutes while simultaneously deploying enhanced, localized incentive structures intended to aggressively drive in-state economic growth and retain highly skilled labor. Administered entirely by the Wisconsin Department of Revenue (DOR) under the authority of Wisconsin Statutes Section 71.28(4) for corporate franchise taxpayers and Section 71.47(4) for other eligible entities (such as individuals, partners, or LLC members), the state credit imposes a strict geographic limitation: the qualified research activities and the associated qualified research expenses must be incurred physically and entirely within the borders of Wisconsin.

Wisconsin statutes deliberately conform to the federal definition of qualified research established under IRC Section 41, adopting the IRS four-part test as the foundational threshold for determining state eligibility. However, while the definition of an eligible activity is synchronized, the Wisconsin legislature departs significantly from the federal framework regarding its base calculation methods, targeted industry rate enhancements, and highly progressive refundability provisions.

Incremental Calculation Methods and the Tiered Statutory Rate Structure

The Wisconsin R&D credit is inherently an incremental incentive, carefully calculated to financially reward businesses that consistently expand their research footprint within the state rather than maintaining a stagnant level of investment. The standard calculation requires the taxpayer to first establish a base amount, which is statutorily defined as fifty percent of the taxpayer’s average Wisconsin-apportioned QREs for the three taxable years immediately preceding the current claim year. The applicable statutory credit rate is then multiplied exclusively by the excess of the current-year QREs over this historically established base amount.

To maximize the economic impact of the incentive, Wisconsin utilizes a highly specific tiered rate system designed to target and accelerate specific industrial sectors deemed critical to the state’s future.

| Wisconsin Statutory Credit Tier | Applicable Credit Rate | Calculation Methodology and Specific Statutory Conditions |

|---|---|---|

| General Research Rate | 5.75% | Multiplied by the excess of current QREs over the base amount. Applies to standard qualified research activities across general industries operating in Wisconsin. |

| Startups / No Historical Base | 2.875% | Multiplied directly against current QREs. Applies exclusively when a claimant had zero QREs in any of the three preceding taxable years. |

| Internal Combustion & Energy Enhanced | 11.5% | Multiplied by the excess of current QREs over the base amount. Applies specifically to research related to internal combustion engines, substitute drives, and designated energy-efficient products. |

| Enhanced Rate Startups | 5.75% | Multiplied directly against current QREs. Applies to startups or entities with no historical base conducting enhanced internal combustion or energy-efficient research. |

The 11.5 Percent Enhanced Credit for Internal Combustion Engines and Energy-Efficient Products

A distinct, highly strategic feature of the Wisconsin statutory framework is its targeted financial support for the legacy automotive, heavy power equipment, and advanced energy manufacturing sectors. Wisconsin Statutes Section 71.28(4)(ab) and Section 71.47(4)(ab) grant a massively elevated 11.5 percent credit rate—effectively double the general rate—for research specifically related to designing internal combustion engines and engineering the vehicles that are powered by such engines. This enhanced rate extends to expenses related to improving the physical production processes for such engines and vehicles.

Crucially, the Wisconsin statutory definition of an internal combustion engine is aggressively modernized to ensure the state remains competitive during the global transition away from fossil fuels. The statutes explicitly state that the term internal combustion engine includes “substitute products such as fuel cell, electric, and hybrid drives”. Furthermore, the statutory definition of a vehicle under these provisions is expansively written to encompass much more than standard automobiles; it legally includes any truck, tractor, motorcycle, boat, personal watercraft, power generator, construction equipment, and lawn and garden maintenance equipment. This precise legislative phrasing demonstrates a clear strategic intent to heavily subsidize legacy mechanical engine manufacturers as they endure the capital-intensive transition into electrification, advanced battery technology, and alternative fuel systems.

Similarly, an identical 11.5 percent enhanced credit rate applies to research activities related to specific energy-efficient products. As defined historically under Wisconsin Statutes Section 71.28(4)(ad)6, this includes research related to the design and manufacturing of energy-efficient lighting systems and sophisticated building automation and control systems that demonstrably reduce the aggregate demand for natural gas or electricity or improve the overall efficiency of its use.

Progression of Refundability and Long-Term Carryforward Provisions

To actively stimulate early-stage innovation and attract venture capital—recognizing that startup enterprises often generate substantial QREs during prolonged development cycles but frequently possess zero immediate income tax liability against which to apply a credit—the Wisconsin legislature introduced highly progressive refundability mechanisms.

The state steadily increased the maximum refundable threshold over a six-year period to maximize cash flow for innovating firms. For tax years 2018 through 2020, ten percent of the generated credit was refundable. For tax years 2021 through 2023, this was increased to fifteen percent. Most recently, under 2023 Wisconsin Act 19, for tax years beginning after December 31, 2023, up to twenty-five percent of the calculated Wisconsin R&D tax credit is completely refundable as a direct cash payment to the taxpayer. The Department of Revenue clarifies that the actual cash refund dispersed is determined as the lesser of twenty-five percent of the total generated credit, or the total credit remaining after it has first been utilized to offset the taxpayer’s current-year state income or franchise tax liability.

Any remaining nonrefundable portion of the research credit is not lost; it may be carried forward for up to fifteen years to offset future state tax liabilities. This generous carryforward provision ensures that heavily capital-intensive developmental phases yield long-term tax mitigation strategies once the enterprise achieves sustained commercial profitability.

Wisconsin Tax Administration Guidance, Audit Procedures, and Relevant Case Law

Because the Wisconsin statutes formally incorporate IRC Section 41 by direct reference, the Wisconsin Department of Revenue (DOR) frequently aligns its auditing procedures and technical interpretations with published IRS audit guidelines. The DOR occasionally works jointly with the IRS during major corporate examinations. However, the DOR explicitly reserves the right to conduct fully independent audits, particularly to enforce distinct state-level geographic nexus requirements to definitively ensure that the claimed QREs were incurred entirely and exclusively within Wisconsin’s physical borders. When the DOR issues a formal notice of deficiency or denies a taxpayer’s refund claim regarding these research credits, the taxpayer’s primary legal recourse is to petition the Wisconsin Tax Appeals Commission (TAC) for a comprehensive redetermination.

Department of Revenue Publication 131 and Concurrent Exemptions

The Wisconsin DOR issues Publication 131 as its primary, comprehensive administrative guidance document for state R&D incentives, which is regularly updated to reflect new legislative acts. Beyond detailing the income and franchise tax credits, Publication 131 clarifies the critical intersection between the research credit and the highly lucrative, concurrent sales and use tax exemptions available to manufacturers and biotechnology firms operating in the state.

Wisconsin statutes provide an absolute sales and use tax exemption for the purchase of complex machinery and equipment that is used exclusively and directly in qualified research. Furthermore, it exempts from sales and use tax the purchase of tangible personal property, explicitly including industrial fuel and electricity, that is consumed or destroyed while being used exclusively in qualified research. Publication 131 emphasizes that highly accurate, contemporaneous recordkeeping is mandatory for taxpayers attempting to claim this exemption, as they must definitively segregate general operational and manufacturing costs from exclusive R&D expenses. If a machine is used for R&D forty percent of the time and general manufacturing sixty percent of the time, it fails the exclusivity test and the purchase is fully subject to state sales tax.

Adjudications by the Wisconsin Tax Appeals Commission and Appellate Courts

The interpretation of what precisely constitutes qualified activities, the strict sourcing of expenses, and the tax treatment of associated experimental equipment have generated significant legal precedent in Wisconsin through decisions by the TAC and higher appellate courts. The TAC organizes its incredibly broad docket alphabetically and by subject matter, utilizing the designation ‘I’ for Income/Franchise Tax cases involving R&D credits, and ‘M’ for Manufacturing Assessment disputes.

The distinction between active manufacturing machinery and experimental R&D equipment was heavily scrutinized in the appellate case Wisconsin Department of Revenue v. Master’s Gallery Foods, Inc. (2022AP1909). The courts analyzed the classification of machinery located at a massive food production facility under Wisconsin Statutes Section 70.111(27)(b), which exempts machinery, tools, and patterns from certain taxation, provided they are not utilized in any way within a manufacturer’s commercial production process. The TAC initially ruled that the equipment was exempt if completely separated from production, leading the circuit court to conduct a deep examination of the legislative history to determine ambiguity regarding the integration of property in food production facilities. This judicial distinction heavily influences how advanced manufacturers in Kenosha must physically and operationally segregate their production machinery from their dedicated R&D trial equipment on the factory floor to maintain tax-exempt status.

Furthermore, the TAC aggressively polices the apportionment and sourcing of R&D expenses and royalty streams across state lines, particularly concerning massive multi-state corporations. In complex cases involving entities such as General Mills, Inc. (20I157) and Hormel Foods LLC (07-I-17), the TAC has meticulously scrutinized intercompany transactions, the geographic sourcing of software use, and the strategic transfer of R&D division expenses. In the Hormel Foods litigation, the TAC examined evidence demonstrating that the taxpayer attempted to shift over ten million dollars of R&D division expenses and massive royalty streams to a newly created Limited Liability Company with the explicit, documented effect of lowering taxable income in non-unitary states, including an estimated tax savings of hundreds of thousands of dollars in Wisconsin alone. Similarly, the TAC explicitly rejected another taxpayer’s attempt to execute a look-through sourcing position via an intermediary to source massive receipts to the ultimate location of software use. These rulings establish a strict, unforgiving interpretation of apportionment, demanding that corporations operating R&D facilities in Kenosha maintain impeccable documentation proving the exact geographic location where the economic benefit and the research activities physically occurred.

Currently, a critical dispute regarding the eligibility of internal-use software expenses is pending before the Wisconsin Supreme Court in the case involving Epic Systems Corporation (2023AP125). Epic Systems, a massive Wisconsin-based healthcare software developer, created highly complex database management system software intended to be used internally by its own software developers. The Wisconsin Department of Revenue aggressively denied the research credits for these internal-use software projects. The taxpayer is actively challenging this denial before the Supreme Court, arguing that the database systems meet the statutory definition of qualified research. The final outcome of this highly anticipated case will set a permanent, binding precedent on the application of the stringent high threshold of innovation test, which federal and state laws require internal-use software to pass to be considered eligible for the R&D credit, directly impacting every firm in Kenosha engaging in internal software automation.

Final Thoughts

The intersection of federal and state tax policies creates a highly compelling, financially optimized economic environment for innovation in Kenosha, Wisconsin. The United States federal R&D tax credit under IRC Section 41 establishes a broad, mathematically rigorous baseline designed to subsidize the immense risks of technological innovation across all scientific disciplines by offsetting a percentage of qualified wages, supplies, and contract research. The State of Wisconsin, through Statutes Section 71.28(4) and Section 71.47(4), completely adopts this federal framework but intelligently layers upon it localized, strategic incentives designed to capture specific, high-value industries.

The introduction of the twenty-five percent refundability provision in Wisconsin fundamentally alters the economic reality for capital-intensive startups, allowing them to monetize R&D losses immediately to fund ongoing operations rather than waiting years for commercial profitability. Furthermore, the targeted 11.5 percent enhanced credit for internal combustion engines and modern substitute drives directly incentivizes companies to nearshore their production and conduct advanced mechanical engineering physically within state borders. Kenosha’s successful transition from a monolithic automotive manufacturing hub anchored by the legacy Chrysler plant into a highly diversified, high-technology cluster is heavily supported by these tax mechanisms. The presence of global entities heavily engaged in food science, biotechnology, advanced precision tools, and automated logistics demonstrates that the region possesses both the deep human capital and the aggressive legislative environment necessary to sustain complex research ecosystems. By rigorously documenting technological uncertainties and maintaining strict experimental methodologies, businesses operating in Kenosha can leverage these federal and state tax frameworks to substantially offset the costs of maintaining global market leadership.

The information in this study is current as of the date of publication, and is provided for information purposes only. Although we do our absolute best in our attempts to avoid errors, we cannot guarantee that errors are not present in this study. Please contact a Swanson Reed member of staff, or seek independent legal advice to further understand how this information applies to your circumstances.

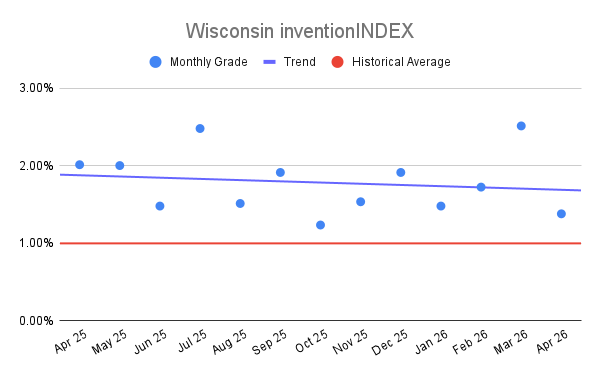

Wisconsin inventionINDEX April 2026:[...]

Wisconsin inventionINDEX April 2026:[...]