Racine Industry Case Studies and Technical Tax Credit Analyses

The application of the United States federal and Wisconsin state research and development tax credits is highly fact-intensive, requiring a meticulous alignment of specific engineering activities with complex statutory definitions. The following six case studies examine prominent industries that developed in Racine, elucidating their historical roots in the region and providing a technical analysis of how their modern innovation processes qualify for federal and state tax incentives.

Case Study: Agricultural Machinery and Heavy Manufacturing – Case IH

The presence of the agricultural machinery industry in Racine is inextricably linked to the arrival of Jerome Increase Case in 1842. Case initially brought hand-powered threshing machines to the Wisconsin territory but quickly recognized the severe limitations of existing agricultural technology in processing the massive wheat yields generated by local Yankee settlers. To address this, he chose to establish the Racine Threshing Machine Works directly at the Root River. This location was a strategic calculation designed to harness reliable water power for manufacturing while simultaneously utilizing the Lake Michigan port for shipping heavy iron components and distributing finished machinery across the expanding American frontier. Throughout the late nineteenth and early twentieth centuries, the J.I. Case Company pioneered the integration of steam power into agricultural implements, producing the first steam engine tractor in 1869. The company’s massive footprint anchored Racine’s heavy industrial sector, driving concurrent regional developments in metallurgy, hydraulics, and internal combustion mechanics as the company eventually merged operations to become Case IH, a division of CNH Industrial.

Modern agricultural machinery development, such as the engineering of autonomous tractors and precision farming equipment currently produced at the Racine manufacturing facility, presents a classic application of the research and development tax credit. Under the federal framework codified in Internal Revenue Code (IRC) Section 41, the development of new tractor chassis, advanced hydraulic lift systems, or global positioning system (GPS) guided automated steering mechanisms clearly meets the permitted purpose of improving the functionality, performance, and reliability of a business component. The engineering processes rely heavily on the hard sciences—specifically mechanical engineering, fluid dynamics, and computer science—satisfying the technological in nature statutory requirement. When engineers at the Racine facility design a new continuously variable transmission for a high-horsepower tractor, they face immense technological uncertainty regarding heat dissipation, torque transfer efficiency, and metallurgical endurance. To eliminate this uncertainty, they must engage in a rigorous process of experimentation, involving computational fluid dynamics modeling, the creation of physical prototypes, and extensive field testing under heavy agricultural loads.

Furthermore, recent federal tax court jurisprudence specifically validates agricultural research methodologies. In the landmark case George v. Commissioner, the court affirmed that the development of pilot models in an agricultural setting constitutes qualified research under federal law. For an agricultural equipment manufacturer, the physical materials utilized to construct a prototype tractor, as well as the specialized fuel and equipment consumed during the iterative field-testing phases, are fully eligible as qualified supply expenses under the federal credit.

Under Wisconsin state law, the company stands to benefit from significantly enhanced credit rates. While general research activities qualify for a standard credit against the state franchise tax, Wisconsin Statute Section 71.28(4)(ad)5 provides a highly lucrative 11.5 percent enhanced credit rate for research related to the design of internal combustion engines and the vehicles powered by such engines. Because a tractor is explicitly defined as a “vehicle” under Wisconsin Statute Section 71.28(4)(ab)3, the mechanical engineering wages, prototyping supplies, and testing costs associated with integrating a new internal combustion engine into an agricultural tractor in Racine categorically qualify for the enhanced 11.5 percent Wisconsin tax credit.

Case Study: Chemical and Consumer Goods Manufacturing – SC Johnson

SC Johnson & Son was founded in Racine in 1886, initially functioning as a parquet flooring company before the founding family rapidly pivoted to the formulation of specialized floor waxes to support their primary product. The company’s profound connection to the Racine municipality is unique in American corporate history; as the corporation expanded into a global conglomerate manufacturing chemical specialty products, pest control solutions, and household cleaners, the founding family actively chose to retain its headquarters in the relatively small midwestern city rather than relocating to a traditional coastal financial hub. This commitment to the region was monumentalized in 1936 when third-generation leader H.F. Johnson, Jr. commissioned the legendary architect Frank Lloyd Wright to design the company’s Administration Building and subsequent Research Tower. Opened in 1950, the fifteen-story cantilevered Research Tower, featuring more than 5,000 Pyrex glass tubes, became the physical epicenter of chemical innovation, housing the laboratories where ubiquitous household brands such as Raid, Glade, OFF!, and Pledge were invented and refined for global distribution.

The formulation of specialty chemicals and consumer goods represents a paradigm of qualified research under Internal Revenue Code Section 41. The development of a new aerosol insect repellent or a sustained-release environmental fragrance is fundamentally rooted in the hard science of chemistry, satisfying the strict requirements of the federal four-part test. When a chemical manufacturer attempts to formulate a new pest control spray that requires a specific microscopic droplet size, an exact atmospheric evaporation rate, and a strict adherence to shifting Environmental Protection Agency toxicity regulations, the scientific team faces substantial technological uncertainty. The company does not know prior to testing the exact mathematical ratio of active ingredients, solvents, and propellants necessary to achieve the desired lethal efficacy against insects while remaining completely safe for residential human use. To resolve this, analytical chemists in Racine must conduct an exhaustive process of experimentation involving iterative batch testing, titration, stability testing under varying extreme thermal conditions, and complex toxicological modeling.

The wages of the formulation chemists, the chemical raw materials consumed during the creation of unmarketable test batches, and the costs associated with operating specialized laboratory equipment all qualify as Research and Experimental (R&E) expenditures under Internal Revenue Code Section 174. Under the Wisconsin state tax framework, the chemical formulation activities conducted at the Racine headquarters qualify for the general 5.75 percent state research and development credit. Crucially, because the research is conducted exclusively within the physical boundaries of Wisconsin, the company complies with the strict geographic nexus requirements mandated by the Wisconsin Department of Revenue and enforced by the Wisconsin Tax Appeals Commission. In addition to the direct tax credit, Wisconsin provides a distinct statutory advantage for chemical and biological researchers by exempting the sales and use tax for machinery and tangible property, including fuel and electricity, consumed exclusively in qualified research.

Case Study: Thermal Management and Internal Combustion Engineering – Modine Manufacturing

Modine Manufacturing Company was established in Racine in 1916 by Arthur B. Modine, an engineering graduate from the University of Michigan who identified a critical mechanical vulnerability in the rapidly mechanizing agricultural sector: the inefficient thermal management of early farm tractors. Modine realized that traditional automotive radiators were prone to catastrophic overheating under the immense strain of continuous field operations. He founded his company in Racine precisely because it placed him geographically adjacent to massive tractor manufacturers like J.I. Case and the Wallis Tractor Company, integrating his startup directly into the regional supply chain. He revolutionized the industry by inventing the Spirex radiator, which utilized a novel spiral fin design to dramatically improve heat transfer efficiency by focusing on the optimal heating of the air passing through the unit rather than merely cooling the internal water. This invention became the standardized equipment for World War I artillery tractors and the ubiquitous Ford Model T. Modine’s commitment to Racine engineering was further solidified in 1940 when the company constructed the largest vehicular wind tunnel in the United States at its Racine facility to test thermal transfer dynamics under simulated operational extremes, enabling the company to develop the supercharger aftercooler for the P-51 Mustang fighter plane during World War II.

Modine’s continuous modern innovation in advanced thermal management systems, vehicular HVAC systems, and heavy-duty powertrain cooling provides a robust foundation for claiming both federal and state research and development tax credits. Developing a new, lightweight aluminum heat exchanger for a commercial trucking application requires resolving intense technological uncertainty regarding metallurgical fatigue, optimal coolant flow rates, and aerodynamic drag resistance. The federal process of experimentation is heavily documented through Modine’s utilization of its Racine-based climate chambers and wind tunnels. The systematic testing of multiple geometric configurations of radiator fins to optimize airflow while minimizing material weight demonstrates the formal evaluation of alternatives required by Internal Revenue Code Section 41.

For Wisconsin state tax purposes, Modine is exceptionally well-positioned to leverage the state’s statutorily enhanced credit tiers. As delineated in Wisconsin Statute Section 71.28(4)(ad)5, the state offers an 11.5 percent enhanced credit for research related to the design of internal combustion engines. Crucially, the Wisconsin Department of Revenue explicitly includes component technologies and accessories that are mounted on or integrate with internal combustion engines within the scope of this definition. Therefore, the complex engineering wages and specialized testing supplies dedicated to developing advanced cooling systems for diesel engines, hybrid-electric drives, or hydrogen fuel cells unequivocally qualify for the 11.5 percent Wisconsin rate, effectively doubling the standard financial incentive for these targeted mechanical activities.

Case Study: Power Transmission and Marine Engineering – Twin Disc

The genesis of the Twin Disc Company in 1918 serves as a premier example of the synergistic industrial ecosystem that defined Racine during the early twentieth century. The company was founded through a strategic collaboration between Percy Haight Batten, the thermal engineer Arthur B. Modine, and the inventor Thomas Fawick. Fawick had engineered a revolutionary twin-disc clutch mechanism designed specifically to withstand the brutal torque demands of heavy farm equipment, particularly the Wallis tractors being produced in the immediate geographic vicinity. By pooling their engineering and manufacturing expertise in Racine, the founders established a global powerhouse in heavy-duty power transmission. During the 1930s, the company expanded its research into marine transmissions, a strategic pivot that culminated in Twin Disc supplying the specialized marine gears for the ubiquitous Higgins landing craft utilized by the Allied forces during the amphibious assaults of World War II, producing components for over 40,000 such vessels.

The modern engineering of industrial gearboxes, highly advanced marine transmissions, and heavy-duty power take-offs inherently involves the discovery of technological information to eliminate uncertainty regarding mechanical endurance, fluid dynamics in hydraulic systems, and acoustic vibration dampening. When Twin Disc engineers develop a new marine transmission system designed to handle the variable torque of a modern hybrid-electric maritime vessel, they must mathematically model gear tooth stress, design custom internal lubrication flow paths, and construct physical prototypes to run on dynamometers until catastrophic failure. This constitutes a highly structured federal process of experimentation.

However, as a manufacturer that often designs bespoke transmission systems for specific original equipment manufacturers or defense contractors, Twin Disc must carefully navigate the complex federal funded research exclusion under Internal Revenue Code Section 41(d)(4)(H). As demonstrated in the federal tax court case Meyer, Borgman & Johnson, Inc. v. Commissioner, if research expenses are financially guaranteed by a third-party client regardless of the engineering outcome, or if the manufacturer does not retain substantial economic rights to the developed intellectual property, the research is legally considered funded and is wholly ineligible for the tax credit. To ensure tax credit eligibility, the commercial contracts governing the development of these customized power transmission systems must be strictly structured as fixed-price agreements where payment is entirely contingent upon the successful meeting of rigorous engineering specifications, thereby ensuring the economic risk of failure remains squarely with the manufacturer in Racine.

Case Study: Advanced LED and Energy-Efficient Lighting – Cree Lighting

While Racine is historically renowned for heavy machinery and metal bending, it has also evolved into a premier center for advanced electronics and solid-state engineering. The roots of this specific sector in the city can be traced back to the founding of Ruud Lighting in 1982. Ruud Lighting rapidly expanded its manufacturing capabilities in Racine, pioneering exterior and interior commercial lighting fixtures. In 2011, recognizing the immense manufacturing infrastructure, supply chain logistics, and highly skilled workforce available in Racine, Cree, Inc. acquired Ruud Lighting. The acquisition merged Cree’s advanced semiconductor technology with Ruud’s established luminaire manufacturing prowess. The Racine facility subsequently became the global launchpad for the first mass-market commercial LED street lights, troffers, and smart wireless lighting systems. Recently, the Racine facility underwent an eight million dollar expansion to increase vertical integration, expanding both its component manufacturing and its sophisticated intelligent lighting test laboratories.

The complex engineering of Light Emitting Diode luminaires, intelligent wireless control systems, and complex optical reflectors constitutes eligible federal research and development. The industrial transition from traditional high-pressure sodium lighting to smart LED networks involves overcoming severe uncertainties related to the thermal degradation of semiconductors, power supply miniaturization, and the algorithmic complexity of wireless mesh networking. Engineering teams at the Racine facility evaluate alternative heat sink geometries using thermodynamic modeling, test optical diffusion materials to eliminate glare, and write proprietary firmware for occupancy sensors, satisfying the permitted purpose and experimentation tests.

From a state tax perspective, Cree Lighting’s operations in Racine are perfectly aligned with Wisconsin’s strategic legislative incentives for sustainable technology. Under Wisconsin Statute Section 71.28(4)(ad)6, the Wisconsin Department of Revenue provides a highly advantageous 11.5 percent enhanced research credit specifically targeted at activities related to the design and manufacturing of certain energy-efficient products. The statute explicitly defines these eligible products to include energy efficient lighting systems and building automation and control systems. Consequently, the vast majority of the research and development expenditures incurred at the Racine facility—including the wages of optical engineers, software developers programming automation logic, and the physical materials consumed in building luminaire prototypes—are eligible for the top-tier Wisconsin credit rate. Furthermore, because the Racine facility itself achieved the Department of Energy’s 50001 Ready status for internal energy management, the company demonstrates a comprehensive structural commitment to the technological advancements prioritized by the state legislature.

Case Study: Appliance Manufacturing and Fluid Dynamics – InSinkErator

The invention and subsequent global domination of the food waste disposer industry is uniquely tied to Racine through the founding of InSinkErator. In 1927, John W. Hammes, an independent architect operating in Racine, sought a more convenient method for disposing of household food scraps. In his basement workshop, he engineered a motorized device designed to utilize centrifugal force to grind and shred solid food waste into fine microscopic particles capable of safely traversing local wastewater treatment infrastructure. After refining the mechanical design over eight years, he secured a patent and co-founded the InSinkErator Manufacturing Company in 1938. The company expanded rapidly within Racine’s established mechanical ecosystem. Acquired by Emerson Electric in 1968 and later by the Whirlpool Corporation in 2022, the company remains headquartered in Racine, producing the vast majority of all food waste disposers utilized globally.

The continuous improvement of consumer appliances requires ongoing, intensive research and development. When InSinkErator engineers attempt to design a new disposal unit that operates with lower decibel acoustic emissions while maintaining grinding efficacy, they must navigate the complex interplay of electrical motor efficiency, fluid dynamics, and material science. Because the exact geometry of the grinding chamber required to achieve optimal acoustic dampening without causing plumbing blockages is unknown at the outset of the project, the engineers face technological uncertainty. Resolving this requires a process of experimentation involving the construction of numerous stainless steel prototypes, the testing of various polymer sound-baffling materials, and rigorous stress testing utilizing diverse organic waste compounds.

The expenditures associated with this iterative prototyping, including the specialized tooling and fixtures required to cast the custom internal grinding mechanisms, qualify for the federal research and development tax credit under the parameters of Internal Revenue Code Section 41. On the state level, these activities qualify for the general 5.75 percent Wisconsin research tax credit. Similar to the chemical manufacturing sector, the heavy machinery and specialized assembly line robotics utilized to manufacture these test components in Racine are exempt from Wisconsin sales and use tax, providing a compounded financial benefit for maintaining sophisticated manufacturing operations within the state’s borders.

The Industrial Evolution of Racine, Wisconsin

To fully understand the application of research and development tax credits to these specific entities, it is imperative to examine the historical macroeconomics of Racine, Wisconsin, which created an environment where such intense technological innovation was not merely discretionary, but an absolute necessity for economic survival. The geographic placement of Racine, founded in 1834 at the mouth of the Root River, was an intentional effort to capitalize on maritime trade routes along Lake Michigan. Initially characterized by the hunting and trapping activities of French fur traders and the indigenous Potawatomi, the local economy rapidly transformed with the arrival of Yankee settlers who recognized the immense agricultural potential of the surrounding soil.

By the 1850s, the region was experiencing a massive wheat boom. The Port of Racine, originally named Port Gilbert, became a primary engine for exporting these agricultural commodities to eastern markets. This immense accumulation of agricultural capital naturally facilitated a transition to light industry, as local artisans began manufacturing the necessary wagons, fanning mills, and pumps required to sustain the agrarian expansion. However, it was the construction of the largest threshing machine plant west of Buffalo by Jerome I. Case in 1847 that permanently shifted the trajectory of Racine toward heavy industrial manufacturing.

The presence of massive agricultural machinery plants created a gravitational pull that attracted highly skilled European immigrant labor, particularly German and Scandinavian machinists, molders, and engineers. This demographic influx fostered a uniquely synergistic industrial ecosystem. When a primary manufacturer produced a tractor, a secondary ring of specialized manufacturers inevitably emerged to engineer the distinct components required for operation—such as Arthur B. Modine developing advanced radiators, or Thomas Fawick engineering heavy-duty clutches. This localized supply chain required intense, collaborative research and development, as components had to be perfectly integrated to ensure reliability in hostile agricultural environments.

Over the twentieth century, this industrial agglomeration solidified Racine’s position within the vital Chicago-Milwaukee economic corridor. The geographic proximity to major Midwestern markets, combined with robust railway networks and eventually the construction of the Interstate 94 corridor, provided the logistical infrastructure required for national and global distribution. The region gained international recognition for specific manufacturing niches, earning titles such as the small electric motor capital of the world. To maintain global competitiveness, Racine’s industries were forced to continuously adapt to technological shifts, transitioning from steam power to diesel, and from basic mechanics to solid-state electronics and fluid dynamics. From the post-Civil War era through the modern technological age, Racine has consistently maintained its status as one of the most heavily industrialized municipalities in Wisconsin, fostering a dense corporate ecosystem where continuous capital investment in research and development is an existential prerequisite.

United States Federal R&D Tax Credit Architecture

The federal Research and Development tax credit was originally introduced by the Economic Recovery Tax Act of 1981 as a temporary legislative measure designed to stimulate domestic corporate innovation and prevent the rapid offshoring of critical technological capabilities to emerging foreign markets. After enduring decades of temporary extensions and legislative uncertainty, the credit was finally codified into permanent tax law by the Protecting Americans from Tax Hikes Act of 2015. The PATH Act also dramatically expanded the utility of the credit by allowing qualified small businesses to utilize the credit to offset employer-paid FICA and Medicare payroll taxes by up to 500,000 dollars annually, providing immediate liquidity to startups that have not yet generated taxable income.

The Federal Four-Part Statutory Test

To qualify for the federal tax credit under Internal Revenue Code Section 41, all baseline activities and corresponding expenditures must satisfy a rigorous, multi-pronged legal standard commonly referred to as the Four-Part Test. Failure to satisfy any single element of this test renders the activity entirely ineligible for the credit, requiring taxpayers to maintain meticulous documentation for each specific project.

- The Section 174 Test (Permitted Purpose): The expenditure must be eligible for treatment as a research and experimental expense under Internal Revenue Code Section 174. The activity must be undertaken for the fundamental purpose of discovering information that eliminates uncertainty concerning the development or improvement of a business component. A business component is statutorily defined as any product, process, computer software, technique, formula, or invention held for sale, lease, or used in the taxpayer’s trade or business. The underlying uncertainty must explicitly relate to the component’s capability, methodology, or appropriate functional design.

- Technological in Nature: The process of experimentation utilized to discover the required information must fundamentally rely on the principles of the hard sciences, specifically engineering, physics, chemistry, biology, or computer science. Activities based on the soft sciences, such as economic analysis, market research, behavioral studies, and aesthetic styling, are explicitly excluded from eligibility.

- Elimination of Uncertainty: At the absolute outset of the project, the taxpayer must encounter definitive technological uncertainty regarding whether they can achieve the desired outcome, the exact methodology required to achieve it, or the specific design architecture required to achieve it. If the solution is already known or available within the public domain, no uncertainty exists.

- Process of Experimentation: Substantially all of the activities (legally defined as eighty percent or more) must constitute elements of a process of experimentation. This requires a systematic, scientific approach involving the formulation of hypotheses, the design of experiments, the formal evaluation of alternatives, and the critical analysis of results. As firmly established in federal jurisprudence, simply applying known engineering principles using basic calculations on available data does not constitute a valid process of experimentation; the engineer must be actively investigating an actual technological unknown.

In instances involving the development of software intended primarily for the taxpayer’s internal use, the Internal Revenue Service imposes an additional, highly stringent High Threshold of Innovation test. This requires the software to be highly innovative, entail significant economic risk during development, and not be commercially available without extensive structural modification.

Legislative Upheaval: Section 174, the TCJA, and the 2025 “One Big Beautiful Bill Act”

The mechanical tax treatment of research and experimental expenditures has undergone unprecedented legislative volatility in recent years, requiring highly sophisticated tax modeling for corporate compliance.

Historically, taxpayers were legally permitted to immediately deduct research and experimental expenses in the exact year they were incurred under Internal Revenue Code Section 174. However, the Tax Cuts and Jobs Act of 2017 fundamentally altered this favorable treatment. For tax years beginning after December 31, 2021, the TCJA mandated that all taxpayers capitalize their research and experimental expenditures and amortize them ratably over five years for domestic research, and a punitive fifteen years for foreign research. This mandatory capitalization requirement severely restricted corporate cash flows, artificially inflating taxable income by preventing immediate deductions for innovation costs.

This restrictive environment was reversed by the enactment of Public Law 119-21, officially titled the One Big Beautiful Bill Act, which was signed into federal law on July 4, 2025. The legislation introduced a new statutory provision, Internal Revenue Code Section 174A, which effectively restores the immediate deductibility of domestic research and experimental expenditures.

| Legislative Era | Statutory Authority | Treatment of Domestic R&E | Treatment of Foreign R&E |

|---|---|---|---|

| Pre-2022 | IRC Section 174 (Pre-TCJA) | Immediate Deduction Permitted | Immediate Deduction Permitted |

| 2022 – 2024 | IRC Section 174 (TCJA) | Mandatory 5-Year Amortization | Mandatory 15-Year Amortization |

| 2025 & Beyond | IRC Section 174A (OBBBA) | Immediate Deduction Restored | Mandatory 15-Year Amortization |

Crucially, Section 174A(a) allows taxpayers to deduct amounts paid or incurred for domestic research in tax years beginning after December 31, 2024. For taxpayers who were forced to capitalize costs between 2022 and 2024, the legislation provides a retroactive transition mechanism under Section 70302(f), allowing businesses to either accelerate the recovery of unamortized domestic costs entirely in 2025, or to spread the deductions evenly over the 2025 and 2026 tax periods to optimize cash flow and prevent the inadvertent triggering of tax shelter classifications under Section 448(c).

Federal Jurisprudence and the Burden of Substantiation

The federal tax courts maintain a notoriously high standard for substantiating research and development tax credit claims. The legal burden of proof rests entirely on the taxpayer to maintain meticulous, contemporaneous documentation generated during the actual performance of the research.

In the highly consequential decision Phoenix Design Group, Inc. v. Commissioner, the United States Tax Court completely disallowed the research credits claimed by an engineering firm focused on mechanical, electrical, plumbing, and fire protection systems. The court determined that the firm failed the process of experimentation test because the engineers primarily relied on basic mathematical calculations on available building data, meaning they already possessed all the information necessary to resolve the architectural design issues. The taxpayer critically failed to specifically identify what technological information was unavailable at the project’s inception. Furthermore, the court noted that while internal emails and meeting minutes can serve as evidence of acquiring information, they are wholly insufficient if they do not demonstrate the systematic evaluation of alternatives to eliminate technological uncertainty. The Phoenix case also highlighted the legal doctrine of the shrinking back rule, which dictates that if an entire business component fails the four-part test, the Internal Revenue Service will shrink back the legal analysis to evaluate a smaller sub-component to determine if that specific piece qualifies.

Conversely, the George v. Commissioner case represented a monumental victory for the manufacturing and agricultural sectors. The court explicitly established that the physical entities utilized during testing—including agricultural pilot models and the feed or raw materials consumed during the testing process—are fully eligible supply costs, definitively confirming that experimentation does not need to occur within a sterile laboratory environment to satisfy the strictures of Internal Revenue Code Section 41.

Additionally, engineering firms engaging in contract manufacturing must navigate the funded research parameters established in cases like Meyer, Borgman & Johnson, Inc. v. Commissioner and Geosyntec Consultants, Inc. v. Commissioner. If a contract does not tie financial payment explicitly to the success of the research, or if the firm does not retain substantial economic rights to the intellectual property developed, the federal court will deem the research funded by the client and categorically deny the tax credit.

Wisconsin State R&D Tax Credit Statutory Framework

The state of Wisconsin provides a robust, parallel framework for incentivizing innovation, modeled largely upon the federal statutes but containing critical jurisdictional restrictions and highly advantageous rate enhancements uniquely designed to support the state’s specific manufacturing heritage.

Jurisdictional Restrictions and Decoupling from the TCJA

Under Wisconsin Statute Section 71.28(4)(ad), Wisconsin defines eligible qualified research expenses by directly referencing Section 41 of the Internal Revenue Code. However, the Wisconsin Department of Revenue imposes a strict geographic mandate: the expenses must be incurred for research conducted exclusively within the physical borders of the state of Wisconsin. If a Racine-based manufacturer outsources digital drafting to an engineering subsidiary located in Illinois, those specific out-of-state expenditures must be ruthlessly excluded from the Wisconsin state credit calculation. The Wisconsin Tax Appeals Commission rigorously enforces this geographic nexus, consistently rejecting look-through sourcing arguments where taxpayers attempt to attribute out-of-state software use or remote engineering support back to a Wisconsin headquarters.

Notably, Wisconsin is a non-conforming state regarding the restrictive federal Section 174 capitalization rules introduced by the Tax Cuts and Jobs Act. While federal law forced five-year amortization between 2022 and 2024, Wisconsin explicitly decoupled from this provision. The Wisconsin Department of Revenue confirms that the pre-2022 federal rules remain in absolute effect for state purposes, allowing Wisconsin corporations to continue fully expensing their research and experimentation costs immediately on their state franchise tax returns, providing a massive regional cash flow advantage that insulates Racine manufacturers from federal legislative volatility.

Tiered Credit Rates and Statutory Enhancements

The Wisconsin research credit utilizes an incremental methodology, calculated by determining the exact monetary amount by which current-year Qualified Research Expenses exceed a statutorily defined base amount. The base amount is calculated strictly as fifty percent of the taxpayer’s average Wisconsin expenses incurred over the three prior taxable years.

Unlike the federal framework, Wisconsin leverages its tax code to directly subsidize specific target industries, resulting in a tiered credit rate structure:

| Wisconsin Credit Category | Statutory Rate | Taxpayer Profile / Industry Focus |

|---|---|---|

| General Research Credit | 5.75% of excess expenses | Standard manufacturing, software, biological, and chemical research. |

| General Start-Up Rate | 2.875% of current expenses | Taxpayers with zero expenses in the prior 3-year base period. |

| Internal Combustion Engines | 11.5% of excess expenses | Research relating to internal combustion engines, vehicles powered by them, and alternate drives (fuel cells, hybrids). |

| Energy Efficient Products | 11.5% of excess expenses | Research relating to energy-efficient lighting, building automation systems, and hybrid vehicle batteries. |

For legacy Racine industries such as Modine and Twin Disc, the 11.5 percent rate for internal combustion engines offers profound financial leverage. Wisconsin Statute Section 71.28(4)(ab) explicitly expands the definition of internal combustion engines to include substitute products such as fuel cell, electric, and hybrid drives, as well as any vehicle frame or component technology in which the engine is mounted. Similarly, the 11.5 percent rate for energy-efficient products directly subsidizes the intelligent lighting development conducted by firms like Cree Lighting, establishing a deliberate state-sponsored pipeline for advanced green technology manufacturing.

Refundability and Audit Defense at the Tax Appeals Commission

In a major legislative push to increase the immediate liquidity of the tax credit, the Wisconsin state legislature radically enhanced the refundability mechanics. While the credit was historically nonrefundable, the state permitted a ten percent refundability tier post-2017, which subsequently increased to fifteen percent for tax years 2021 through 2023. Following recent legislative amendments, for tax years beginning on or after January 1, 2024, an unprecedented twenty-five percent of the total Wisconsin research credit is fully refundable.

This means that if a startup technology firm in Racine generates massive research expenses but currently operates at a net financial loss, the firm can file Schedule R and receive a direct cash refund from the Wisconsin Department of Revenue equal to twenty-five percent of the generated credit amount. Any unused, nonrefundable portion of the credit may be carried forward for up to fifteen years to offset future tax liabilities. Pass-through entities, such as S-Corporations and limited liability companies, compute the credit at the entity level via Schedule R and pass the credit pro-rata to their shareholders for utilization on their individual state income tax returns.

When disputes arise between taxpayers and the Department of Revenue, the designated venue for litigation is the Wisconsin Tax Appeals Commission. The Commission serves as the final administrative authority prior to circuit court intervention, and its holdings are binding precedent. In matters involving the research credit, the Commission’s jurisprudence often centers on strict procedural mechanics and the heavy burden of substantiation.

A landmark procedural ruling occurred in the Oshkosh Truck Corp. decision. In this case, the Department of Revenue assessed an additional franchise tax deficiency against the taxpayer for a specific historical tax year. The taxpayer possessed highly documented research credits for that exact year, but the statutory window to file an amended return to claim those credits had already expired, rendering the claims legally stale. However, the Wisconsin Tax Appeals Commission invoked the powerful jurisprudential doctrine of equitable recoupment. The Commission ruled that because the Department forcibly opened the specific tax year to assess a deficiency, the taxpayer was legally permitted to offset that specific deficiency using the time-barred research credits, provided the credits arose from the identical year and distinct income tax period. This establishes a critical defensive shield for Wisconsin manufacturers facing aggressive state audits.

Strategic Synthesis and Implementation Nuances

The convergence of the federal and Wisconsin state research and development tax credit frameworks creates a highly complex, yet profoundly rewarding, financial landscape for manufacturing and engineering firms operating in the Racine industrial corridor. The reinstatement of immediate expensing for domestic research under federal Internal Revenue Code Section 174A in 2025 drastically improves the upfront cash flow mechanics of innovation, resolving the severe liquidity constraints imposed by the previous amortization mandates. Simultaneously, Wisconsin’s refusal to adopt the prior federal capitalization mandates, combined with its twenty-five percent refundability provision and 11.5 percent targeted enhanced rates, positions the state as an exceptionally hospitable jurisdiction for capital-intensive development.

However, the legal barriers to entry remain uncompromising. As evidenced by the Phoenix Design Group and Meyer, Borgman & Johnson federal tax court decisions, the Internal Revenue Service and the Wisconsin Department of Revenue will aggressively disallow credits unsupported by meticulous, contemporaneous documentation. Taxpayers in Racine must ensure their internal accounting systems trace qualified employee wages directly to specific, technologically uncertain engineering projects. Furthermore, companies engaging in contract manufacturing must rigorously audit their commercial agreements to ensure they unequivocally retain the economic risk of development, shielding their activities from the statutory funded research exclusions.

For over a century, the geographic and demographic advantages of Racine, Wisconsin, have fostered a relentless cycle of industrial adaptation—from the water-powered threshing machines of Jerome Case to the sophisticated solid-state optical architectures of Cree Lighting. By mastering the intricate intersection of engineering practice and statutory tax law, the modern enterprises operating within this historic corridor can continue to leverage the federal and state tax codes to underwrite the immense financial risks inherent in pushing the boundaries of technological capability.

The information in this study is current as of the date of publication, and is provided for information purposes only. Although we do our absolute best in our attempts to avoid errors, we cannot guarantee that errors are not present in this study. Please contact a Swanson Reed member of staff, or seek independent legal advice to further understand how this information applies to your circumstances.

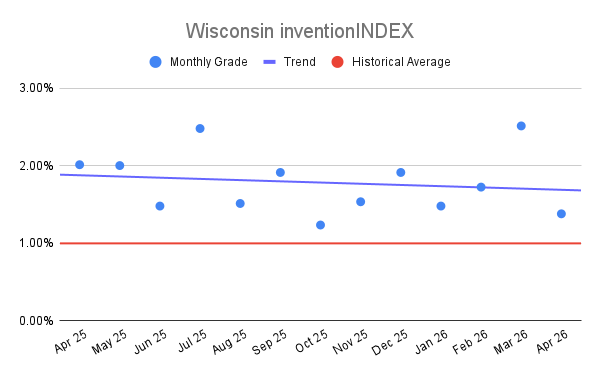

Wisconsin inventionINDEX April 2026:[...]

Wisconsin inventionINDEX April 2026:[...]